Since September, the trucking industry has seen very tight capacity and in some instances, extraordinarily high rates. FreightWaves called it at the end of August when the hurricane season exposed an underlying lack of capacity. Since then, weather events like wildfires and regulatory hurdles such as the ELD mandate have further constrained the free movement of freight, raising rates across the country.

The effects have been manifold and somewhat unpredictable—when Hurricanes Harvey, Irma, Jose, and Maria simultaneously threatened the Caribbean, Asian shippers decided to reroute Panama Canal container traffic to Seattle. The Port of Los Angeles was already operating at full capacity. Suddenly, the obscure, low-volume freight lane from Seattle to Salt Lake City was overwhelmed with Asian freight, and while the lane had maintained a normal rate of about $1.50 per mile, it shot up to $1.85 in September, $2.28 in October, and and $2.56 in November. Over the past seven days it’s still running at an average of $2.52 per mile. The Seattle-Salt Lake City lane is just a small example of how weather events in a completely different part of the country can reroute supply chains and have massive effects on trucking rates. FreightWaves and DAT have observed these trends across the country.

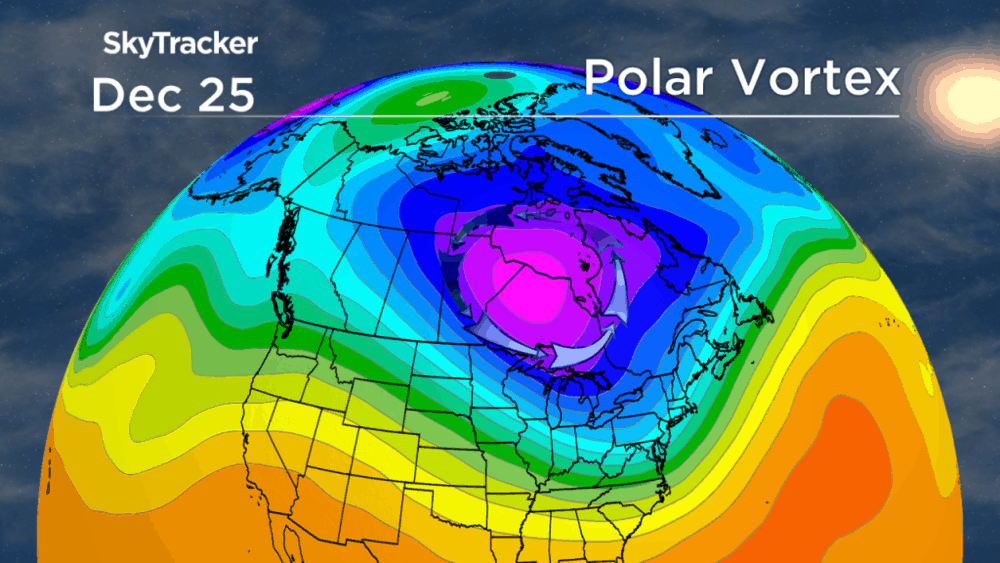

Now the Polar Vortex, the persistent low pressure zone circulating over the North Pole, has shifted back toward North America. In early December, North America saw unusually warm temperatures because the PV was on the other side of the planet, freezing much of Siberia and northern Asia. Now the vortex has drifted back over the Arctic and down into Canada. The PV’s movement tracks perfectly with Riskpulse’s 2017-8 Winter Weather Outlook, which noted an unstable Polar Vortex that would create highly variable conditions in December and January.

Jon Davis, chief meteorologist for RiskPulse, spoke to FreightWaves Friday afternoon, and underlined the effects of the pronounced cold snap the US is experiencing. “To put a little bit of historical perspective on this,” Davis said, “if you look at anywhere in the US, from the Rockies to the East Coast, if you look at the end of December to beginning of January, that will be the coldest period since 1950. It’s historically significant. The central and eastern US has never been colder during the end of December and beginning of January since 1950—for the past 67 years. Few people have lived through a colder New Year’s than the one we’re about to experience.”

All modes of freight transport have been affected. Davis said, “What’s interesting with this current situation is that the really big snows in upstate New York, Cleveland, and Erie—almost all of that is lake snow. It comes down to the intensity of the cold air from the PV, streaming from Siberia over the pole into the US. Because the fall was warm, and the Great Lakes were warm, that differential produces a massive amount of snow. It’s really turned on the Great Lakes snow machine. Barges, rails, roads, are all highly affected by the amount of snow, largely because of the intensity of the cold.”

Indeed, spot rates have shot up around the Great Lakes and Northeast. Dry van spot rate 7 day averages from Erie to Boston are at $3.78 a mile; rates from Chicago to Erie are at $3.91. Philadelphia to Boston is $4.07, Detroit to Buffalo is $4.19, Toledo to Philadelphia is $4.02, and Cleveland to Philadelphia is $3.83. In general, outbound rates out of Chicago have been high, and inbound rates into Philadelphia have been high.

Looking forward, Davis said, “The keyword for January and February is ‘more and more major variability and volatility.’ As we look at January, the first week or 10 days are going to be exceedingly cold. We see some pretty good signals that thereafter, there will be a period of moderation. From the middle of January to the second half of the month, we’ll be moderating, and after getting back to normal, we’ll start to warm up to above normal levels.”

Mark Montague, an analyst for DAT, put the regional rate spikes into a national perspective. “You see rate spikes on various van lanes, but Virginia has some soft pockets, Florida has a lot of flatbed equipment available, and California has gotten a little bit softer. Central Wisconsin got socked in with snow, and north-central Minnesota and North Dakota have seen a lot of disruption, but some of the worst weather effects have been in markets like Spokane and Missoula, places that are not strong volume freight markets,” Montague said. “Trucks are tight just about everywhere. Rates in the high $3-$4 range are not unusual–we’ve been seeing those kinds of rates since the hurricanes,” Montague added. Reefer rates are way up, too, in 61 of the top 72 lanes.

We emphasize that the volatile spot rate activity, with wider deltas than usual because the upper limit on rates has been blown off, has not been caused solely by recent weather events. Strong economic growth, the expansion of American oil production, downward pressure on per-truck productivity from the ELD mandate, and a seemingly unrelenting series of severe weather events are creating overlapping effects to keep truck rates high. Montague said, “For the near term, there are multiple places around the country where there’s a shortage of trucks and high rates, and that won’t be fixed overnight. The first quarter is definitely going to be stronger, rate-wise, than a year ago—substantially stronger. And if GDP growth holds up, the second quarter will be crazy.”

Stay up-to-date with the latest commentary and insights on FreightTech and the impact to the markets by subscribing.