They don’t call it the Windy City for nothing. The stuff that is blowing in right now is expensive—and strangely, rates going out are elevated as well. The aberration is that both are high. The question is why?

Chicago is the top U.S. freight hub. Usually, it’s a beautiful spot. Long haulers love going to Chicago because they know they can always find freight to bring out after they’ve brought a load in. There should be plenty of capacity in Chicago generally at all times, especially as it’s a hub from so many directions. It has a lot of points of consolidation, and it often also flows out of Chicago in a lot of directions. When you have a lot of turndowns in Chicago, it’s basically because you don’t have the trucks there.

SONAR’s Outbound Tender Rejection Index (OTRI) has gone up to 20.88% in the past 9 days. The fact that Chicago is outpacing the market is significant. In the wintertime this would make sense. In the summertime, however, there’s a lot of activity. The bottom line is that truckers don’t turn down freight when it’s scarce. And as you’ve probably heard the entire year of 2018, there is a lot of freight. So why, when capacity is so tight, is Chicago of all places overheated?

First, the reason we’re seeing inbound turndowns is separate from the reason that we’re seeing outbound turndowns. They’re related in the way that the market itself is experiencing general capacity constraints, but the outbound situation is more regionalized. The best explanation is that capacity is too tight. Drivers do not want to long haul it into Chicago, only to be faced with short regional lanes—that are also difficult to haul anything out of–at least when the action is as hot as it is in the southwest.

A look at the current numbers supports this. Regional lanes are going up even more than long haul in the area. For instance, Chicago to Minneapolis (408 miles—a good drive, but still no freight coming out) is at its highest ever, according to DAT, jumping from $2.20 to $2.49 in the last month. Chicago to St. Louis (296 miles) went from $2.62 to $2.83. Chicago to Milwaukee (93 miles) has gone from a flat-rate minimum of $434 to $471. Similarly, Chicago to Indianapolis has gone from a flat-rate minimum of $652 to $740. All of this in the past month.

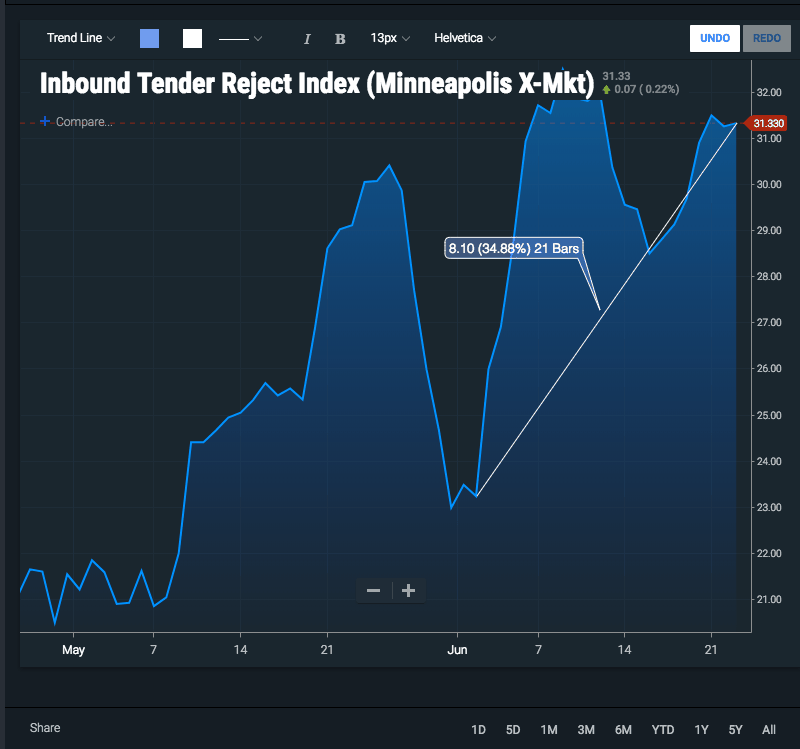

Also, Atlanta to Chicago inbound rates are blowing apart. Rates jumped $1.82 to $2.44 the past month, blowing through the ceiling of last June when it went as high as $1.61. Drivers really don’t want to go in.

Meanwhile, a long haul from Chicago to Dallas only went from $1.78 to $1.87 this past month—and certainly not as high as we saw in January at $2.26. Why is that? The data is telling us that they’re more than happy to long haul to where the action is hot.

So, from a national perspective, what we’re seeing is that the long haulers have bigger and better things to do right now, like going out west where L.A. is on fire. L.A.’s Outbound Tender Rejection Index (OTRI) is one of the only places in the country that hasn’t taken a dip. It stands at about 18%.

L.A. to Dallas was $1.60 in May to $2.23 in June, the highest it’s been in 13 months—and the tender rejections aren’t spiking there; they’re staying elevated. Long haulers are flowing in there to keep moderating the turndowns, and doing so while the rates remain high.

Overall, the market is unstable. It took the biggest increases on record in February and March, and in spite of this we’re seeing carriers break their route guides and search the spot market. Even summer in Chicago is not immune to the volatility.

Note: rate calculations do not include fuel costs

Stay up-to-date with the latest commentary and insights on FreightTech and the impact to the markets by subscribing.