Texas is on the verge of crude-by-truck

On Thursday the Brent-WTI spread, the difference between the international North Sea-based crude oil benchmark and West Texas Intermediate crude, hit $8.25. Brent was trading at $79.47 per barrel, while a barrel of WTI brought $71.22.

FreightWaves reported on the significance of the Brent-WTI spread in January: to put it simply, when American oil is discounted against international oil, global appetite for American oil exports grows and American production should respond.

In 2016, the Brent-WTI spread averaged about $1; this increased to an average of about $3.33 for 2017. By last month, the spread had already widened to $5.33. For most of Q1 2018, both indexes were rising, but Brent price hikes simply outstripped WTI. Today, it’s a little bit different: WTI is actually down slightly—18 basis points—on the day while the price of Brent increased 48 basis points. The movement of the two oil benchmarks is actually diverging.

The strong climate for oil prices is taking place in front of a familiar backdrop: OPEC production cuts, geopolitical risk in places like Iraq and Yemen and the Venezuelan economic crisis which has hampered production. But the ever-widening Brent-WTI spread has special implications for the American oil and gas industries, as well as truckload transportation and logistics.

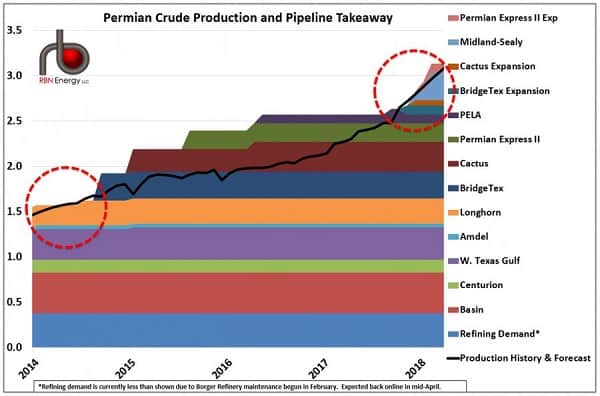

Takeaway pipeline capacity in the Permian Basin has nearly reached its limit: production has grown faster than new pipelines have been added. CNN reported this month that “America’s biggest oilfield is running out of pipeline”, and Michael Tran, a global energy strategist at RBC Capital Markets, said, “The Permian Basin has been so prolific that it’s overwhelmed pipelines. There isn’t enough capacity to move barrels to market.”

When pipeline capacity is maxed out, shale oil producers will be forced to turn to rail and truck to move their crude to ports. The problem is that hiring trucks and train cars is much more expensive than buying capacity in a pipe, and, depending on how much WTI is moved over the roads and rails, the higher transport costs will show up in the price per barrel. It’s possible that could narrow the Brent-WTI spread and help reduce the relative demand for Texas oil, cooling production off.

According to the Pipeline & Gas Journal, new pipes with the potential to carry up to 2.4M barrels per day have been proposed by a number of operators. Epic, Enterprise, Plains All American, and Magellan are all working on projects to alleviate the midstream bottleneck.

Even if those projects are completed in time to avert an expensive turn to trucks and trains, the demand for truckload miles in certain lanes is strongly correlated with oil production.

According to DAT’s Rateview tool, flatbed spot rates from Houston to Oklahoma City are averaging $3.29 per mile over the past seven days, up from $2.95 in the month of April. The flatbed lane from Birmingham, Alabama, where P&S Transportation, one of the largest flatbed carriers in the country is based, to Oklahoma City, spiked to $3.33 in the month of April, but has softened somewhat to $3.06 over the past seven days. Flatbed spot rates from Houston to Lubbock (our proxy for the Permian Basin) are sky-high, averaging $3.21 over the past seven days. Flatbed spot rates from Nashville, where Daseke-owned TSH & Co. is based, to Houston, shot up to $2.92 over the past seven days.

Stay up-to-date with the latest commentary and insights on FreightTech and the impact to the markets by subscribing.