Another equity research analyst has pulled up earnings estimates for trucking companies. Citing recent conversations with management teams from several transportation companies, Deutsche Bank (NYSE: DB) analyst Amit Mehrotra raised his earnings per share (EPS) forecasts for the rest of 2020 and all of 2021 on the carriers he follows.

“The bottom line is we expect Transportation results to be very strong across the board, with likely more to come over the course of the next several quarters,” stated Mehrotra in a weekend note to clients.

On average he increased his third-quarter earnings estimates for truckload (TL) and less-than-truckload (LTL) companies by approximately 18%. Mehrotra said his third-quarter estimates now range between 12% and 32% higher than the current consensus estimates. He believes the expected outperformance in the third quarter will result in forward-looking estimates being raised as well. As such, he raised his full-year 2020 and 2021 estimates by an average of 9% and 10%, respectively.

Mehrotra also implemented short-term, high-conviction favorable ratings on the shares of TL carriers Knight-Swift Transportation (NYSE: KNX) and Werner Enterprises (NASDAQ: WERN), and LTL carriers Old Dominion Freight Line (NASDAQ: ODFL) and SAIA (NASDAQ: SAIA). Prior to the report, Mehrotra had positive ratings on most of the carriers he follows.

He doesn’t believe the increase in third-quarter earnings estimates will result in declines in the multiples used to value the shares of these carriers, which is typically the case as earnings forecasts begin to improve.

“It’s important to note that the positive inflection we expect with 3Q results is occurring against a backdrop of still-low absolute new truck orders, which should limit potential for the de-rating of positive earnings revisions … a key risk for Transports (and cyclicals, in general) as we progress through the cycle,” he stated.

Improved outlook partly company-specific

Mehrotra believes the positive year-over-year inflection in August revenue at Old Dominion is largely attributable to higher weights per shipment. He sees the fuller shipments (weights up 3.6% year-over-year in July and 5.9% in August) as carrying less incremental expense, meaning more revenue will “drop to the bottom line.” He also views Old Dominion’s use of company-owned linehaul capacity as a margin tailwind compared to carriers that rely on third-party TL capacity and expects the favorable trends in the third quarter will change the mid- to long-term consensus outlook for operating ratios (ORs), or margins, for the carrier.

He believes Saia has seen “outsized price increases” as the carrier has sacrificed volume for yield. The company reported a slight year-over-year decline in August shipments after a 1.5% increase during July. The thought is improved pricing will allow the company to see twice the sequential OR improvement guided to for the third quarter (200 basis points instead of 100 basis points). Mehrotra believes the third-quarter margin result “helps support the path to mid-80% OR and the significant increase in earnings power that comes with that profit improvement.”

Last week, both LTL carriers reported year-over-year improvement in tonnage during August for the first time since the April swoon.

Mehrotra sees the “very strong truckload market” as a catalyst for improved earnings at carriers Knight-Swift and Werner Enterprises. He believes Swift’s expansive trailer fleet has created incremental revenue and pricing opportunities and that both Knight and Swift are potentially operating at a sub-80% OR level during the third quarter. Knight’s trucking OR was 84%, with Swift’s at 85.3% during the second quarter. He sees these trends as catalysts for the company to potentially raise 2020 earnings guidance.

The opportunity for Werner is improved utilization and revenue per total mile, according to the report. The company was stated as having the ability to reset up to 25% of its one-way contracts higher, in essence allowing it to participate in the spot market to a larger degree than some may think.

Further, the improvements don’t accompany cost inflation like broad driver pay increases as driver turnover remains low in relative terms throughout the industry. Mehrotra sees these trends “as sustainable, given the still-significant need for inventory restocking.” He noted a “significant gap” between sales and inventories at major retailers, which he sees as “disproportionately” benefiting Werner, which has significant exposure to discount and home improvement retail.

Shares of ODFL finished the day down 1% while SAIA was up 0.6%. KNX and WERN were basically flat. The S&P 500 moved nearly 3% lower on the session.

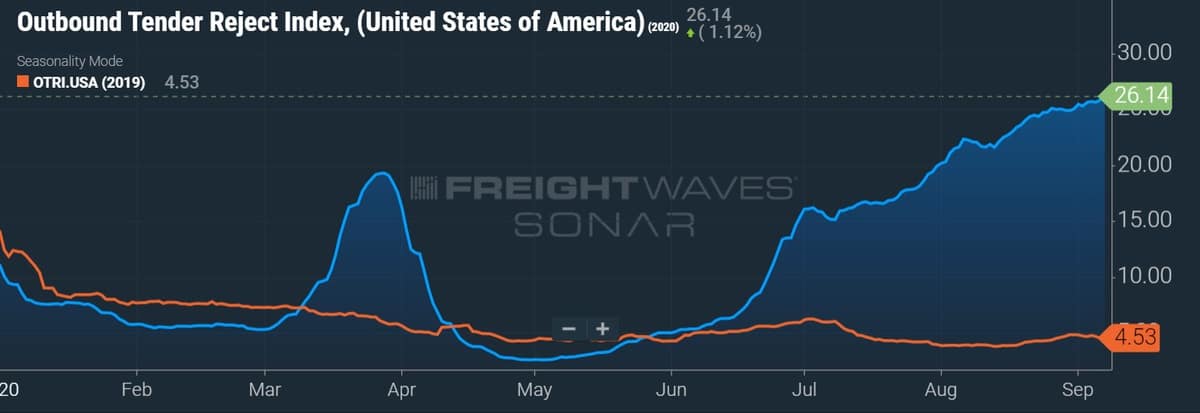

How tight is truck capacity?

The Outbound Tender Reject Index (SONAR: OTRI.USA), a measure of tendered loads rejected by carriers, stands near all-time highs at more than 26%. A sustained capacity drawdown, the result of increased costs and regulation which led to carrier failures and lower levels of equipment purchasing, has been met by shippers struggling to procure equipment to replenish inventories depleted from COVID-related buying.