Shipments saw a slight step lower in November with rates likely to inflect negatively year over year (y/y) by early 2023, according to a Tuesday report from Cass Information Systems.

Cass’ shipments subindex was down 1.9% from October and off by just 0.4% y/y in November.

“After some noise in recent months related to comparisons and other temporary factors like repositioning mistimed inventory and consumers getting ahead of rising interest rates, freight volumes settled back to a flattish level in November versus a year ago,” ACT Research’s Tim Denoyer said.

The latest shipments subindex reading was 4.1% higher than November 2020 and 6.8% above November 2019. Denoyer described the current level as “still a very stable environment overall but still one with many headwinds.”

The report noted that recent declines in imports “suggest near-term trends could soften further.” If normal seasonal patterns hold in December, volumes will likely be 5% lower y/y.

| November 2022 | y/y | 2-year | m/m | m/m (SA) |

| Shipments | -0.4% | 4.1% | -1.9% | -0.5% |

| Expenditures | 4.7% | 50.7% | 1.8% | 3.9% |

| TL Linehaul Index | 1.7% | 11.4% | -1.2% | NM |

After 30%-plus y/y increases throughout the pandemic, the freight expenditures subindex increased just 4.7% y/y in November, up 1.8% from October. The index measures the total amount spent on freight and is inclusive of fuel. The report noted that higher fuel costs, up 41% y/y during the month, and changes to modal mix were the main catalysts for the increase.

With shipments down 1.9% sequentially and expenditures up 1.8%, the inference is actual freight rates were likely up 3.7% sequentially during the month and 5.1% higher y/y.

The report said the expenditures index is likely to be flat y/y in December.

“The supply/demand balance in U.S. trucking markets has loosened significantly this year, and as a result freight rates are leveling off and set to soften further in the months to come,” Denoyer said. “Shippers are starting to see real savings and considerable cost relief is now likely for 2023, which should be increasingly positive news for the complex inflation picture.”

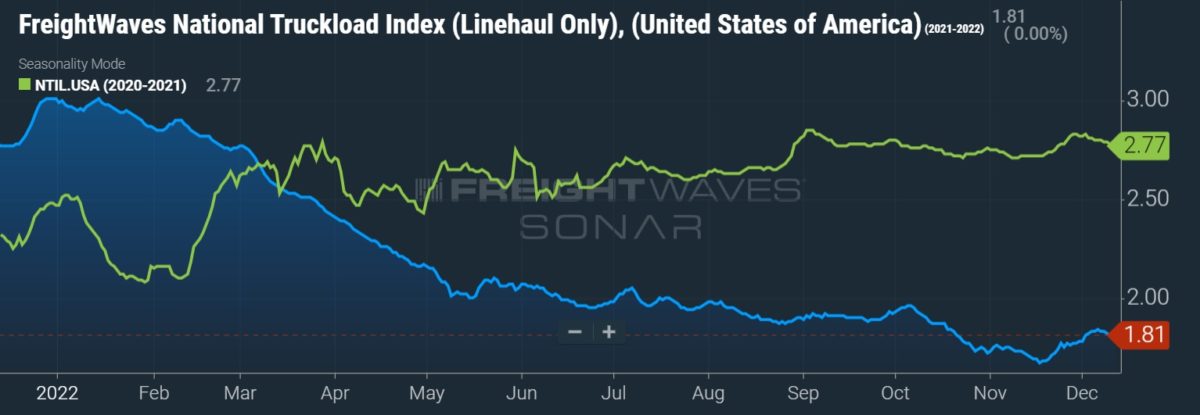

Cass’ Truckload Linehaul index, which excludes fuel and accessorials, declined 1.2% sequentially in November but was still 1.7% higher y/y. This was the sixth consecutive month the data set declined on a sequential comparison. The index includes spot and contract freight and is expected to begin to see y/y declines starting in January as the contract market has been “adjusting down more gradually.”

Data used in the Cass indexes is derived from freight bills paid by Cass (NASDAQ: CASS), a provider of payment management solutions. Cass processes $37 billion in freight payables annually on behalf of customers.

More FreightWaves articles by Todd Maiden

- ArcBest CFO to retire; company to begin search for replacement

- Yellow sees outsize volume drop as network overhaul advances

- Forward Air sees near-20% tonnage decline in November