A hockey-stick pattern starts with a low-level period — the blade — hits an inflection point, curves up, then heads sharply higher — the shaft. Newly released financial and operating reports for Q3 2021 by Matson (NYSE: MATX), Cosco and OOIL show container shipping in full-on hockey-stick mode.

Winners and losers

Pandemic restrictions and fiscal stimulus created winners and losers. On the losing end: companies that depend on people congregating in close quarters for business or pleasure. Think Midtown Manhattan office-building landlords and cruise lines. The winners: companies that facilitate the transport and sale of goods.

E-commerce has been a huge COVID-era winner, yet some retail income charts are starting to look less hockey-stick-ish. Rising challenges related to product sourcing, labor, storage and distribution, together with much higher transport costs, are beginning to bite.

After a steep rise beginning in the Q2 2020 lockdown period, both net income and operating income of Amazon (NYSE: AMZN) fell in the second quarter of this year versus the first quarter as expense growth outpaced sales growth.

Not so in container shipping, at least so far. What’s bad for importers — skyrocketing transport costs — is good for carriers. Ocean carriers are also far less labor-intensive than the land-based winners: One vessel carrying 10,000 twenty-foot equivalent units, which can gross $15 million or more per headhaul voyage, has a crew of less than 30 people aboard. And while overall liner costs are rising, revenues are rising faster.

Drewry Maritime Research projected last week that the liner industry as a whole will earn $150 billion this year, up sharply from its $100 billion forecast in early July. Drewry also now expects carriers to make the same or slightly more next year, bringing the two-year tally to around $300 billion.

To put that in context, McKinsey & Co. estimated in 2018 that shipping lines had destroyed around $110 million in shareholder value over the prior two decades. In other words, carriers could earn almost three times as much in two years as they lost in the previous 20.

Matson blows away estimates

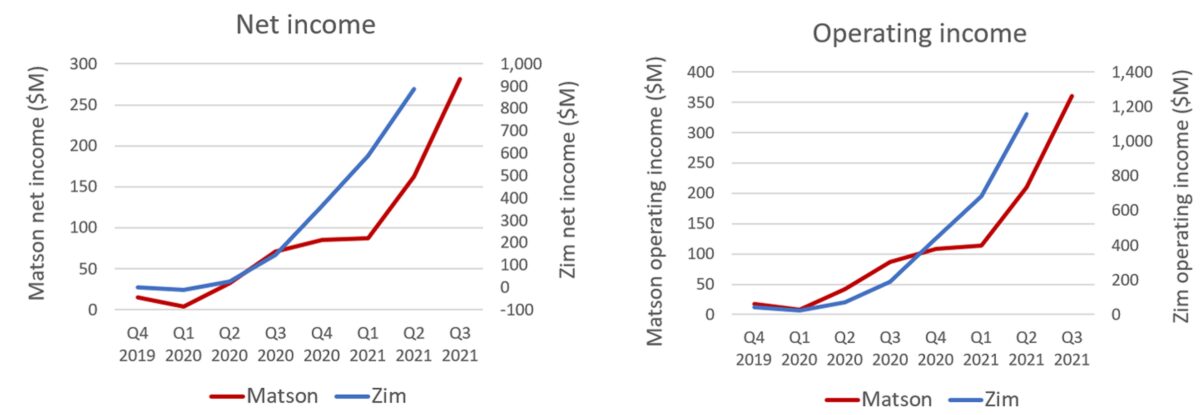

After market close on Monday, Matson disclosed that it will post 3Q 2021 net income of $277.3 million-$285.5 million when it announces final results on Nov. 1. In the second quarter, it earned considerably less: $162.5 million.

Profits in the third quarter were driven by operating income from its ocean transport division of $358 million-$363 million, compared to $201 million in Q2. Matson CEO Matt Cox said that he expects favorable conditions “to remain largely in place at least through midyear 2022.”

The consensus estimate for Matson 3Q earnings was $4.87 per share. Matson now says EPS will be around 33% higher than that: $6.39-$6.58 per share. Matson “materially exceeded our estimates yet again,” said Stifel analyst Ben Nolan.

Matson is one of two container shipping carriers with U.S.-listed common shares, along with Zim (NYSE: ZIM). Both are heavily focused on the Asia-U.S. trade, and in both cases — unlike with Amazon — their hockey-stick patterns are still intact.

On Tuesday, a day when Wall Street indexes fell, shares of Zim and Matson rose 5% and 7%, respectively.

COSCO and OOIL results keep climbing

China’s Cosco, the world’s fourth largest carrier group, preannounced Friday that it earned net income of 30.49 billion yuan ($4.73 billion) in 3Q 2021. That’s up from 21.64 billion yuan in the second quarter and 14.45 billion yuan in the first.

Cosco subsidiary OOIL reported its revenues and lifting data on Friday. Revenues for 3Q 2021 totaled $4.31 billion. In Q2, revenues were $3.47 billion, and in Q1, $3.02 billion.

As previously reported by American Shipper, OOIL highlighted “severe congestion around the network,” which depressed volumes. Overall load volume rose only 0.4% year on year, yet average revenue per TEU spiked up by 142.7%.

Too much congestion lowers carrier volumes and impairs revenues as ship capacity is tied up. But ocean carriers are still in a sweet spot where congestion inflates rates to an extent that heavily outweighs revenue fallout from voyage delays.

Click for more articles by Greg Miller

Related articles:

- How supply chain chaos and sky-high costs could last until 2023

- Record shattered: 73 container ships stuck waiting off California

- How high can container shipping profits go? Will 2022 top 2021?

- Battle of the shipping booms: Containers ‘21 vs dry bulk ‘07-‘08

- Global demand isn’t booming. So why are shipping rates this high?

- Inside container shipping’s COVID-era money-printing machine

- Supply chain ‘anarchy’ is gold mine for ocean carriers like ZIM