As part of our overall coverage of freight markets, FreightWaves publishes a summary of the changes in the economy over the past month, both in terms of the data releases and in developments in public policy. The Economic Roundup is designed to synthesize the events of the past month as they relate to freight markets, and provide a guide on trends to keep an eye on in the upcoming month. The Roundup is published on the first business day of each month with the next release scheduled for Tuesday, May 1st.

Overview:

Economic conditions as they relate to freight generally improved during the month. Data releases in the month of February (largely covering January activity) were replete with disappointments, with retail, manufacturing, housing, and international trade all surprising on the downside.

Results released in March weren’t universally positive, but were certainly stronger, and served as a reminder that freight demand is likely to remain solid in upcoming months. Many key indicators rebounded, making some of the early-year performance look more like a temporary pullback after a strong 4th quarter than a sustained slowdown in the economy.

Indeed, there is reason to believe that the economy will actually gain further momentum in the 2nd quarter. The impact of the recent Tax Cuts and Jobs Act has yet to be felt in any meaningful way in the real economy, and will likely provide a boost to activity in the remainder of the year. In addition, the recent budget agreement allows for some additional federal spending and should provide some extra lift to the economy in the second half of 2018.

Of course, the economy still faces some potential headwinds from policy, as recent announcements of tariffs from the Trump administration have threatened to derail some of the momentum that the economy currently enjoys. So far, however, the tariffs have been less obstructive than originally thought in implementation and, barring any escalation into a broader trade war, should have a fairly small impact on overall international trade in the economy.

So what does this all mean for freight markets? The accelerating economy will keep the demand high for transportation services, keeping the pressure on trucking companies who are already dealing with tight capacity. With tougher enforcement of the ELD mandate starting April 1st and truck companies already struggling to deal with driver shortages, the strength in the economy is likely to translate into further price increases and additional delays in the trucking space. This, in turn, is likely to lead to spillovers into other areas of freight and will pressure shippers to find ways to contain their transportation spending throughout the year.

Gross Domestic Product

Overall growth in the 4th quarter was revised up to 2.9% from previous reports of 2.5%. Much of the revision was driven by improvements to consumer and business spending, which speaks to the strength of the economy’s fundamentals at the end of last year. GDP growth performed well during the last three quarters of 2017 and is expected to remain generally strong throughout 2018.

Keep in mind that GDP measures all of the economic activity in the US economy for the quarter, not just movements that involve freight. The US economy is made up of approximately 70% services, which may or may not have any goods movements associated with it. As a result, many other metrics such as industrial production, retail sales, and goods exports do a better job of tracking freight performance in the economy

Trend to watch: The initial release of 1st quarter GDP is scheduled for the end of this month. Given the weakness in results from January, GDP is likely to pull back some from the growth seen in the 4th quarter, but should pick up through the rest of the year.

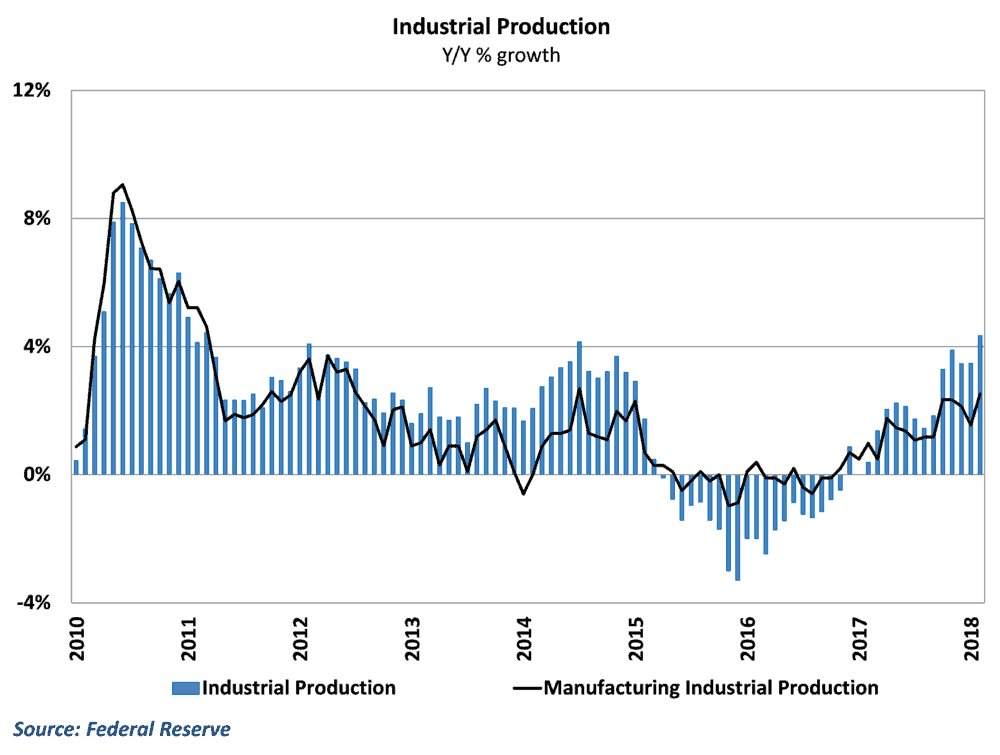

Manufacturing

Results on the manufacturing side of the economy generally improved during the month after disappointing releases throughout February. The “hard” output data in the manufacturing sector performed particularly well, as industrial production and durable goods orders saw strong rebounds after weak results in January. Year-over-year growth in industrial production jumped above 4% for the first time since 2014, and the continued solid results from durable goods orders suggests that manufacturing activity will remain robust going forward.

The survey data in the manufacturing sector was a bit more mixed. The Institute of Supply Management’s national manufacturing index rose to the highest level in over a decade. Regional Federal Reserve surveys showed improvements in New York, but Philadelphia, Richmond, and Dallas surveys slipped.

Trend to watch: Responses from the regional surveys suggests that manufacturers felt some sting last month from the initial announcements of tariffs, which pushed some of the softer results. It will be interesting to see whether or not these tariffs are having lasting effects when these surveys are updated throughout the month.

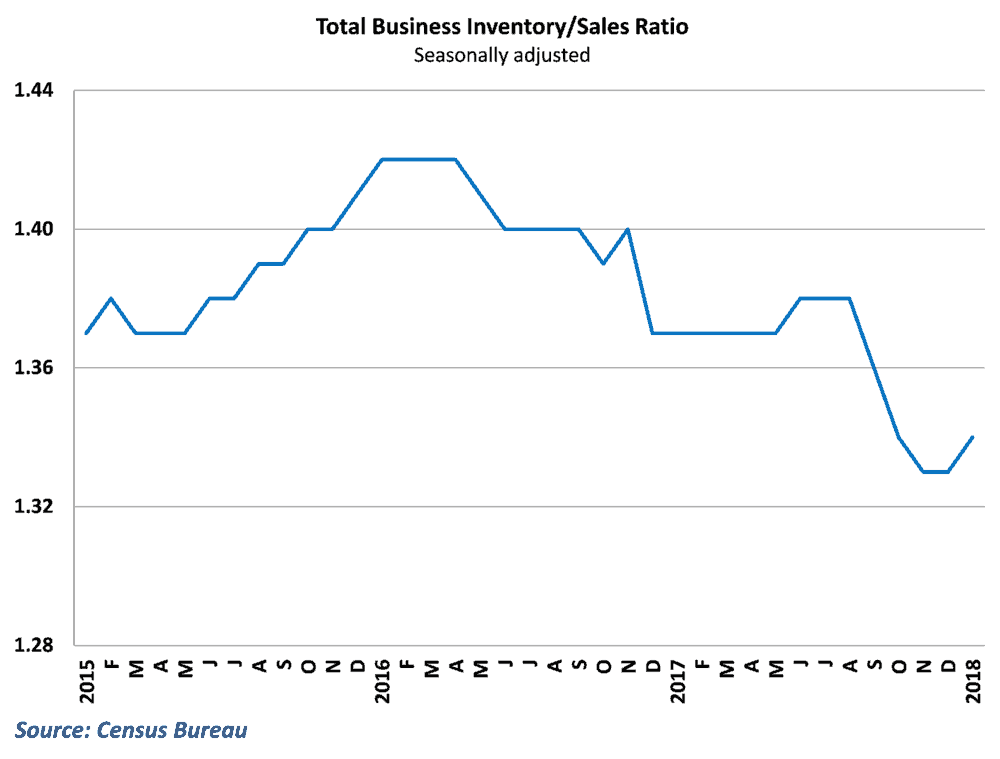

Retail and inventories

Retail performance underwhelmed last month and unexpected declined for the third consecutive month. Much of the decline was driven by a dip in auto sales however, as the rest of the retail sector managed to eke out a small gain. Electronic shopping also took a bit of a hit during the month, although year-over-year growth in e-commerce continues to outpace brick-and-mortar sales by a wide margin. This has implications for carriers, as the growth in last-mile delivery continues to be a theme in the transportation and logistics space.

The weakness in sales led to a rise in inventory levels and reduced inventory turnover during the month. This, in turn reduced some of the demand for freight, which has been pressured by lean inventories and tight shipping deadlines.

Trend to watch: Retail sales get updated again in the middle of the month. Much was made at the end of last year about the boost that tax cuts would give to US households, but very little evidence of that has been seen on the spending front. Right now, the weakness in retail looks like pullback after a strong 4th quarter, but another month of weak retail would start to raise some real concerns.

Labor markets

Job growth was very strong in February, with over 300,000 jobs added to payrolls. The labor market continues to impress with large employment gains despite already low unemployment in the economy. Wage growth remains stubborn, but the pace of hiring should continue to support consumer spending growth going forward.

Trend to watch: Hiring has begun to pick up some momentum in the trucking industry. February saw the largest monthly gain in trucking jobs in the past few years, and the number of jobs added in the industry has improved in each of the last four months. More needs to be done in order to address the current shortage, but this has become an important trend to keep an eye on when the next jobs report hit son Friday.

Housing and construction

Housing data was generally mixed during the month, as home sales and home prices saw solid gains during the month while home starts fell well short of expectations. Most importantly for freight markets, construction spending disappointed last month, which means less lumber and building materials being transported through the economy. However, oil and natural gas drilling activity picked up during the month, which should help truckers.

Much like the trucking industry, construction has been faced with a shortage of available skilled workers. There is still quite a bit of pent up housing demand in the economy, and the rapid gains in home prices suggests that households want to buy, but the housing market continues to be hampered by a tight inventory of homes for sale.

Trend to watch: Housing can be particularly volatile at the start of the year, as weather activity often shifts activity in the early months. This may also be the case when March’s data is released, as late-winter snowstorms across the northern part of the country may have restrained construction. As a result, it may be a while before the underlying strength of the housing market is known.

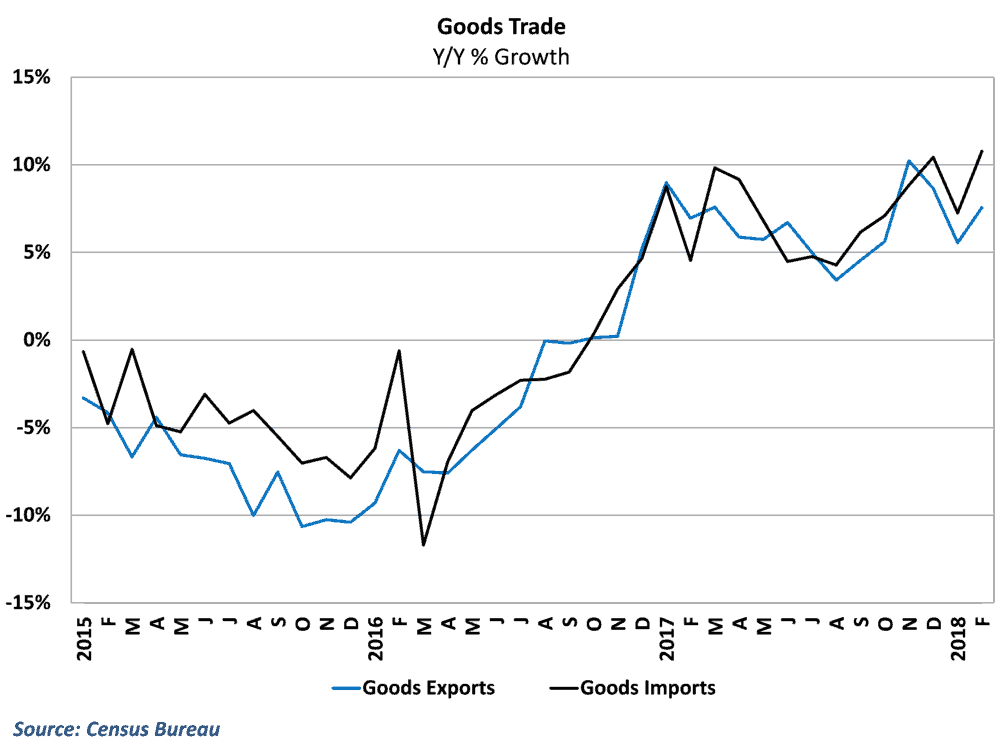

International Trade

On the trade front, the goods deficit increased for the sixth consecutive month, reaching a new post-recession low. This makes it likely that trade will continue to subtract from growth in 1st quarter GDP results are released next month.

The good news for the transportation industry is that trade volume rebounded strongly during the month. Goods imports surged in February, particularly in the major West Coast ports.

Trend to watch: It will be interesting to see how well trade volumes hold up in upcoming months. For one, some of the surge in February may have been caused by the manufacturers rushing to stock up in early February before the late Chinese New Year this year. This certainly would go a long way to explain the gaudy import numbers into the West Coast. Factory activity usually shuts down for weeks in China due to the New Year, and March import trade likely felt the pinch.

Trade numbers from February are also the last data points before the announcements of protectionist tariffs on steel and aluminum and targeted tariffs on China. How this plays out in actual trade activity will be one of the key trends to monitor going forward.

Ibrahiim Bayaan is FreightWaves’ Chief Economist. He writes regularly on all aspects of the economy and provides context with original research and analytics on freight market trends. Never miss his commentary by subscribing.