As part of FreightWaves’ overall coverage of freight markets, it publishes a summary of the changes in the economy over the past month, both in terms of the data releases and developments in public policy. The Economic Roundup is designed to synthesize the events of the past month as they relate to freight markets, and provide a guide to trends to keep an eye on in the upcoming month. The Roundup is published on the first business day of each month with the next release scheduled for Wednesday, May 1.

Overview:

Developments over the past month continue to point towards an economy that lost considerable momentum. Data releases in March (mostly covering February activity) generally fell below expectations, with poor showings from international trade, manufacturing, employment and housing construction throughout the month.

There are a few reasons for optimism going forward, however. Keep in mind that the government shutdown, polar vortex and Midwest flooding all hit the economy in the early parts of 2019 and likely hamstrung growth during the quarter. As the economy normalizes following these events, growth should improve in the second quarter and beyond. FreightWaves still expects that the pace of growth will be slower than in 2018, but the economy should regain some momentum after a poor first quarter.

GDP

Revisions to U.S. gross domestic product (GDP) showed that the economy slowed to a 2.2 percent pace of growth in the fourth quarter of 2018, down from the initial estimate of 2.6 percent. Downgrades to consumer spending and business investment drove much of the revision, suggesting that domestic demand in the economy was weaker than initially thought at the end of 2018. Still the general picture of the economy remains roughly the same following the revision.

Trend to watch: First quarter GDP results will be released at the end of this month. The combination of the effects from the government shutdown, inventory drawdowns, weakened investment demand and significant weather events are likely to drag GDP growth below 2.0 percent. FreightWaves expects GDP growth of 1.5 percent before some rebound in activity in the second quarter.

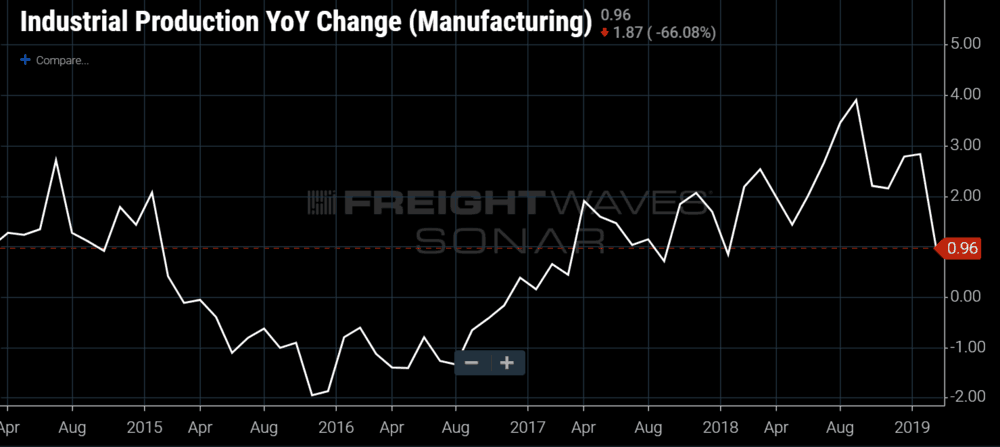

Industrial production and manufacturing

Industrial output again fell short of expectations in February, as total industrial production rose by just 0.1 percent despite a surge in utility production due to the cold weather at the beginning of the month. Manufacturing production, which excludes mining and utilities from the total, fell for the second consecutive month as year-over-year growth tumbled to just 1.0 percent. Factory orders for manufacturers also struggled during the month, as the latest readings from January showed just a 0.1 percent increase.

Survey data from the manufacturing sector has reinforced the performance in manufacturing production, as both data from the Institute of Supply Management (ISM) and regional Federal Reserve manufacturing readings have cooled from the high readings that emerged last year. The ISM manufacturing index posted its lowest value in over two years in February, coming in at 54.2. This still suggests expansion in the sector, but the pace of growth is still significantly slower than last year.

Trend to watch: ISM data from the manufacturing sector covering March activity is scheduled for later today (April 1) and will give an early view on performance at the end of the first quarter. The New Orders component will be of particular interest, giving some insight into how severe the current slowdown in manufacturing will be.

Retail and inventories

Retail sales activity rebounded in January after December’s disastrous results, rising 0.2 percent during the month. On its face, this is just a slight improvement, but the details in the January report were far more encouraging. Growth during the month was restrained by large declines in both motor vehicle and gasoline sales. Once these categories are stripped out, core sales grew at a more robust 1.2 percent led by rebounding sales at sporting goods, building materials and healthcare stores. Year-over-year growth in core retail sales continues on a moderating trend, but remains generally healthy at 3.7 percent.

On the inventory side, the total inventory/sales ratio jumped to 1.38 in December 2018 from 1.35 in the previous month. Much of this rise was driven by poor sales in December, as both retailers and merchant wholesalers experienced falling sales at the end of last year. In addition, many U.S. companies began importing more than they otherwise might during the fourth quarter in an attempt to evade the threat of future tariffs, particularly on goods from China. Companies are already beginning to draw down some of these inventory stores, and are likely to continue to do so in upcoming months.

Trend to watch: The Census Bureau is still dealing with delays from the government shutdown, and released February data this morning (April 1), showing a decline in retail spending. Poor weather contributed to the weakness during the month, but consumer spending has clearly lost some momentum in the first quarter .

Labor markets

The labor market provided the biggest surprise during the month, as just 20,000 workers were added to payrolls in February. This marks the slowest pace of hiring in the economy since hurricane season disrupted hiring in September 2017, raising questions about the fundamentals for consumer spending and the economy overall going forward.

Trucking hires continued to advance in February, adding 900 workers to payrolls during the month. This marks the tenth consecutive month with positive job growth and puts trucking employment 2.7 percent higher than at this point last year. This continues to outpace hiring in the economy overall, where total employment is 1.6 percent higher than at this point last year, and suggests that industry has managed to add significant capacity over the past several quarters. Job openings within the transportation and logistics industry have cooled some in recent months, however, which suggests that the labor market in the industry is no longer much tighter than it is for the economy overall.

Trend to watch: All eyes will be on the March employment report, which is scheduled for April 5. Most other indicators outside of job growth were decent in February. The unemployment rate dropped to 3.8 percent, which is close to the near 50-year low of 3.7 percent reached late last year, and wage growth remained strong at 3.4 percent year over year. Still, if the number hires fails to rebound in March, it would heighten concerns about the pace of growth for 2019.

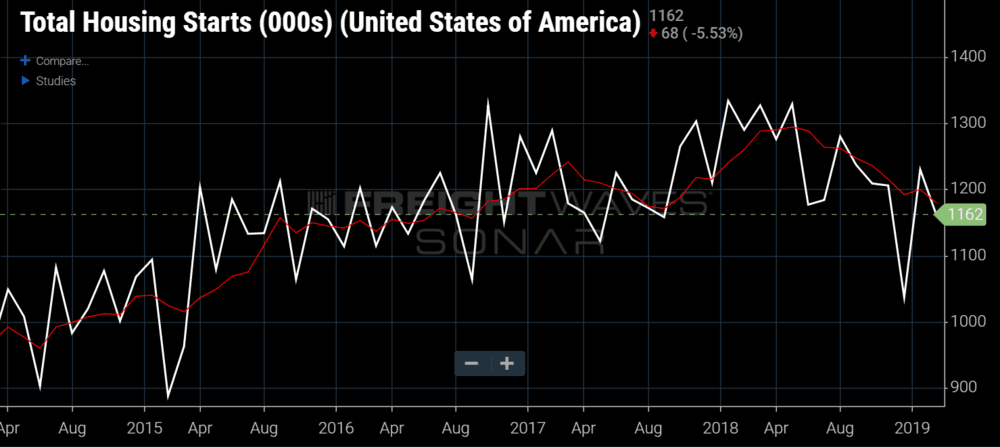

Housing and construction

Housing construction data also fell short of expectations in February, falling 8.7 percent to a 1.16 million annualized pace. Single-family home building plunged during the month, falling to the slowest pace in over one and one-half years and weighing down overall results during the month. Building permits also fell during the month, though permits now exceed starts in the economy. This suggests that homebuilding activity will remain subdued, but should expand in the spring months.

On the demand side, the results were far better as both new and existing home sales grew at a rapid pace in February. Home buying activity was plagued throughout the second half of 2018 by rising prices and higher mortgage rates. However, mortgage rates have cooled in recent months, and as long as labor market conditions stabilize, housing demand should improve.

Trend to watch: Trends in housing starts have clearly turned negative since the third quarter of 2018, but weather events have likely played a role in some of the recent softness. Flooding in the Midwest likely also had an effect in March, but there is significant building and repair work that will take place in upcoming months.

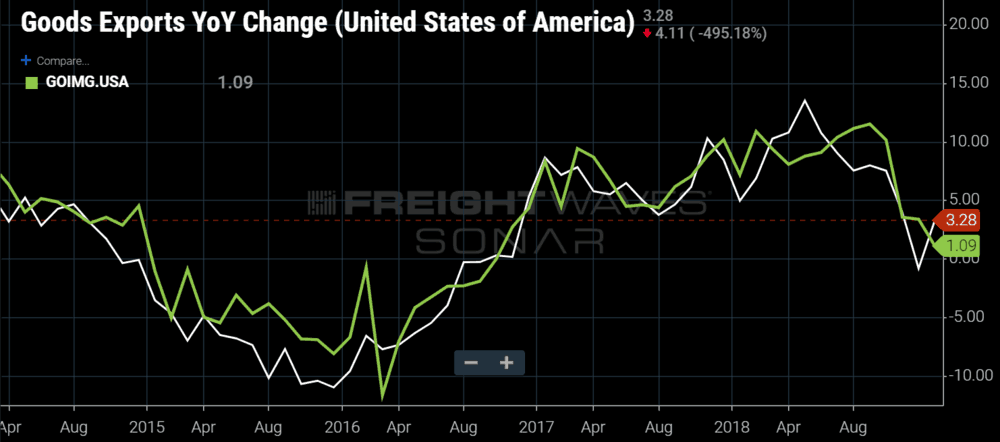

International Trade

The Census Bureau reported that the U.S. economy’s goods deficit narrowed sharply in January to -$73.3 billion on a seasonally adjusted basis, from a revised -$81.5 billion in the previous month. This has positive implications for international trade’s contribution to first quarter GDP growth when numbers are released this month, but details on imports and exports were far less sanguine for freight demand.

Goods exports managed to rebound in January, rising 1.3 percent for the first increase in four months. This was enough to push year-over-year growth in goods exports back into positive territory at 3.3 percent after dipping into negative territory in the previous month. Goods imports fell by 3.0 percent in January, erasing all of the previous month’s gain and pulling year-over-year growth in goods imports down to 1.1 percent. As a result, the total value of traded goods fell during the month, which has negative implications for freight demand in early-2019.

Trend to watch: Tariffs-related moves have introduced additional noise into the international trade numbers in recent months, but underneath it all is a clearly decelerating trade sector. Reports suggest that the U.S. and China are nearing a deal to resolve the ongoing trade conflict, but weakening global growth and a decelerating U.S. economy are likely to keep trade growth relatively slow this year.

Ibrahiim Bayaan is FreightWaves’ Chief Economist. He writes regularly on all aspects of the economy and provides context with original research and analytics on freight market trends. Never miss his commentary by subscribing.