As part of our overall coverage of freight markets, FreightWaves publishes a summary of the changes in the economy over the past month, both in terms of the data releases and in developments in public policy. The Economic Roundup is designed to synthesize the events of the past month as they relate to freight markets, and provide a guide on trends to keep an eye on in the upcoming month. The Roundup is published on the first business day of each month with the next release scheduled for Tuesday, September 4th.

Overview:

Economic conditions as they relate to freight remained generally solid throughout the month, as health in consumer spending and business investment continue to drive demand for freight in the 2nd quarter. Most of the data released in July (predominantly coving June activity) suggest that the economy finished the 2nd quarter at a rapid pace.

US GDP grew at a rapid 4.1% pace during the second quarter as a rebound in consumer spending and continued strength in business investment helped drive activity. The economy was helped by a temporary boost from international trade, which helped offset a significant slowdown in inventory building.

The end result was one of the strongest quarters of growth in the post-recession era, made even more impressive when you consider that inventories subtracted a full percentage point from growth. Going forward, growth will likely continue at a solid pace, but most indications point to some softening in growth throughout the 3rd quarter. This is not a real weakening in the fundamentals of the economy, but the reversal or absence of some temporary factors that helped growth in the 2nd quarter should weigh down growth in the current quarter.

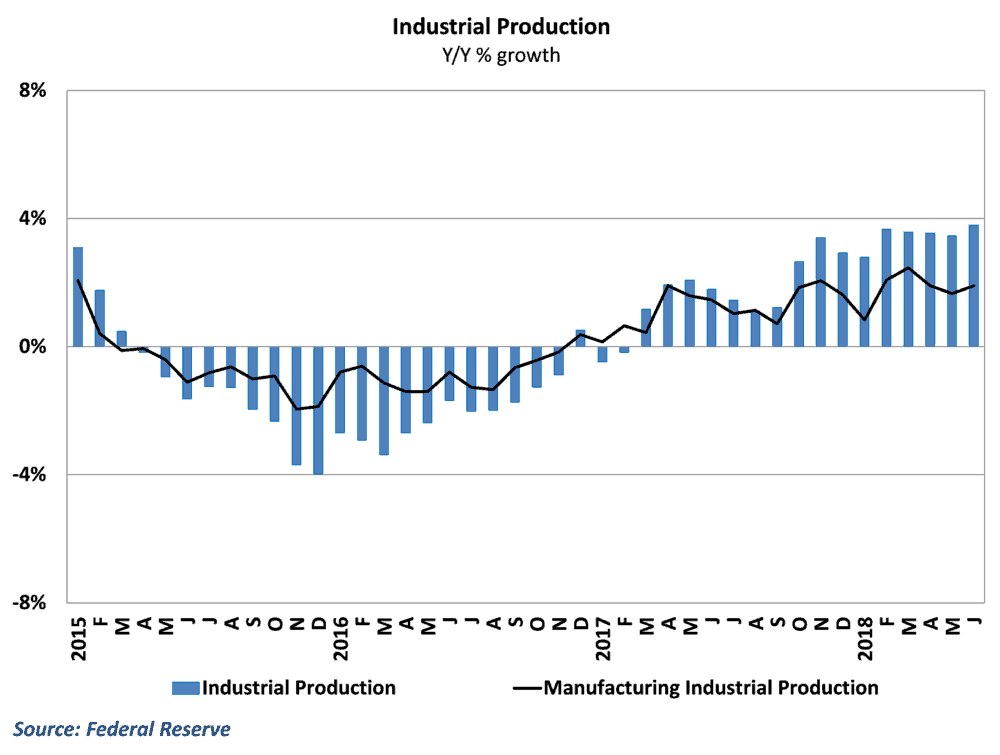

Manufacturing and industrial production

Industrial output continues to grow at a rapid clip in the economy, as gains in the energy sector have helped to drive activity during the first part of the year. Growth in total industrial production rose to 3.8% in June after a healthy monthly gain helped to erase last month’s disappointing results.

Outside of the energy sector, manufacturing activity has been a bit of a disappointment. Manufacturing industrial production also had a solid month in June, but much of the gain during the month was driven by a rebound in auto production after the Ford auto plant supplier fire in May. Growth in the manufacturing sector remained below 2% in each month in the 2nd quarter, falling well short of expectations coming into the quarter

Survey data continues to point towards strength in manufacturing, however, as most of the drivers of manufacturing demand remain healthy. Responses from Federal Reserve surveys and purchasing manager data suggest that the combination of tariffs and lack of trucking capacity have contributed to disrupting supply chains in the manufacturing sector, which could explain some of the softness in manufacturing

Trend to watch: Survey data on order backlogs gives some valuable insight into the ability of manufacturers to meet demand in the economy. Readings from the ISM index and regional Fed surveys will give an indication of whether companies are able to navigate around trucking capacity issues.

Retail and inventories

Retail performance kept humming in June, as year-over-year climbed to 6.6% during the month. This put a cap on an impressive quarter for the retail sector, which bounced back nicely after a disappointing start to the year. E-commerce remains a highlight within the retail space, but the gains in June (and the rest of the quarter) were generally broad-based.

Inventories were essentially flat during the month among wholesalers and retailers, although much of the gain was driven by a buildup of inventories in the auto industry. Nonauto inventories remain fairly lean in the economy, particularly in the retail sector, which will continue to put pressure on carriers to meet tight inventory replenishment schedules.

Trend to watch: Retail appears to be on solid footing going forward after the early-year hiccup. Looks for continued healthy gains going forward as US households still have a solid foundation for spending.

Labor markets

Labor market news was positive during the month as job growth surprised on the upside with 213,000 jobs added in June. The unemployment rose slightly during the month, but this was driven by people rejoining the labor force rather than any weakness in hiring. Wage growth fell short of expectations overall in June, but did fairly well for the quarter, and tight labor market conditions should push wage growth higher gradually going forward.

Trucking hires continued to push forward in June with 2,500 jobs added during the month, though results were dampened by a downward revision to the previous month’s data. Trucking employment is now 1.7% than it was at this point last year, which is slightly faster than the economy overall, but lagging behind growth in other industries such as manufacturing and construction.

Trend to watch: The labor market has continuously defied expectations throughout the year with generally strong job numbers all throughout. Labor is getting scare however in the economy, and it will be difficult for this torrid pace of hiring to be sustained for much longer. At some point there will be a slowdown in job growth to match the general pace of expansion in the labor force.

Housing and construction

Housing data fell well short of expectation from both the supply and demand side, as tight inventory and rising mortgage rates have led to a softening in activity. Home starts suffered a massive decline in June, which pushed the entire negative relative to the first quarter. Home builders have struggled in recent months from labor shortages and rising materials costs, which has affected the profitability of new construction.

Sales of both new and existing houses also saw significant declines in activity in June. Existing home sales have declined thus far in 2018 and are on track to be negative for the entire year. Inventory is particularly tight for existing homes, which has pushed up prices and restrained sales considerably.

Trend to watch: Tariffs on Canadian lumber are partially to blame for the massive spike in materials costs for home builders. Trade policy has been in constant flux once early in the year, and housing is one of the downstream industries that could be affected by the outcome of policy changes.

International Trade

In international trade, the goods deficit widened after three consecutive months of a narrowing trade balance. A decline in exports was the primary culprit here, as the amount of goods sent to other countries fell by 1.5% during the month. Imports rose by just 0.6% in June, leaving the total value of goods traded slightly lower than it was last month.

Tariff-induced volatility is likely to affect international trade patterns going forward, as companies in the US and abroad continue to try to navigate through a rapidly changing policy landscape.

Trend to watch: May’s numbers were boosted by an unseasonably strong surge in soybean exports, which reflect some of the trade tensions in China. June’s numbers suggest that this behavior continued through the end of the 2nd quarter, but this trend likely began reversing in July.

Ibrahiim Bayaan is FreightWaves’ Chief Economist. He writes regularly on all aspects of the economy and provides context with original research and analytics on freight market trends. Never miss his commentary by subscribing.