A pair of releases this morning show that retail spending and industrial output expanded in August, signaling that some key components of freight demand continue to grow at a healthy pace in the 3rd quarter.

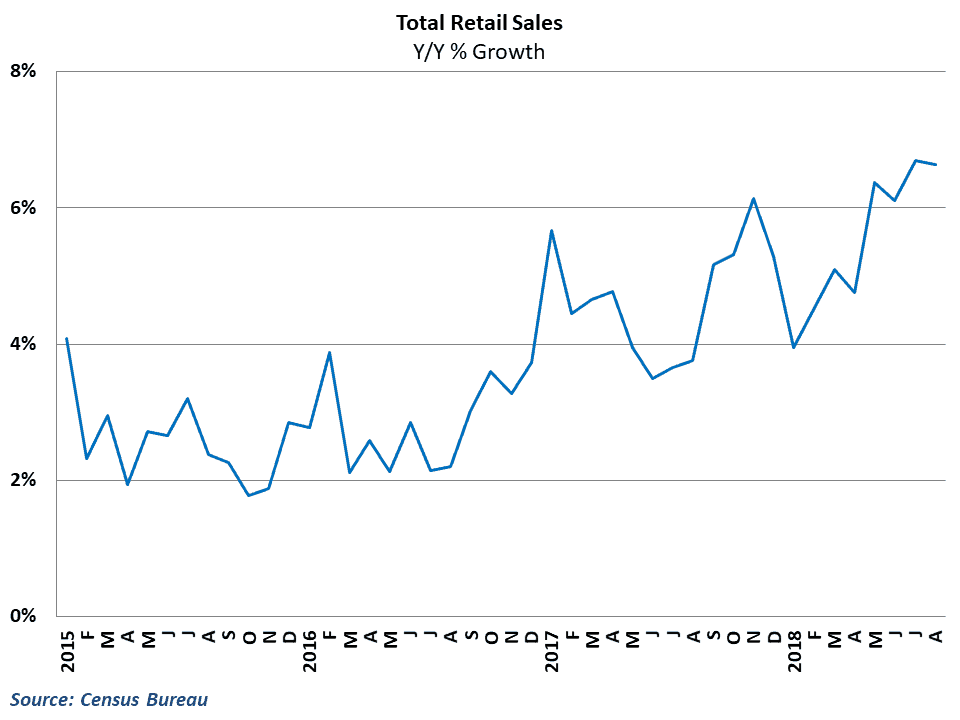

The Census Bureau reported this morning that total retail sales rose 0.1% in August on a seasonally-adjusted basis from July’s levels. While this fell short of consensus estimates of a 0.4% gain, numbers from July were revised upward leaving the combined results from the two months roughly in line with expectations. Retails sale have now grown for seven consecutive months and are 6.6% higher than at this point last year

Growth in the sector came despite a sizeable decline in auto sales, which fell 0.8% during the month. In addition, weakness in the housing sector has affected retail spending in some downstream retail industries, as furniture sales and sales of building materials both saw declines during the month.

Outside of these areas however, retail growth was generally broad-based and 9 of the 13 major industries in the retail report saw higher sales in August than in July. Big gains in gasoline, health care, and electronics sales helped to lead the way during the month. Nonstore (mostly online) retailers also experienced another month of strong growth and sales in this industry are now 10.4% higher than at this point last year. Overall, another solid month in the books for the retail sector, and consumer spending looks to be in a good space during the 3rd quarter.

Manufacturing activity looking to accelerate

On the industrial side of the economy, total industrial production rose 0.4% in August on a seasonally-adjusted basis from July’s levels. This was in line with consensus expectations and marks the third straight monthly increase after the Ford fire-influenced decline back in May. Total production has now increased in 9 out of the past 11 months as year-over-year growth rose to 4.9%. This is the fastest pace of growth in the industrial sector since the end of 2010 and underscores just how strong this part of the economy is during the 2nd half of the year.

Some of the strength in total production stemmed from rebounds in mining activity in August. In fact, the resurgence of the mining and drilling sector has been one of the key driving forces in the impressive performance of industrial output. Mining production makes up over 15% of total industrial production and is now 14.1% higher than at this point last year. Manufacturing industrial production, which excludes mining and utilities from the total, rose 0.2% in August and year-over-year growth climbed up to 3.1%. Like the total, this marks the fastest pace of manufacturing production growth in years, and given the data from manufacturing surveys, activity should remain strong in upcoming months

There are some concerns within manufacturing going forward, however. Much of the gain during the month was driven by a surge in auto production, which rose a whopping 4.0% during the month. Outside of the auto sector, many of the major industry groups showed big declines in August, with some particularly large drops on the nondurable side of the economy. Survey data suggests that demand remains fairly strong for these goods, but businesses are not able to keep up with the amount of orders they are receiving. Going forward, this is likely to remain an issue as manufacturers continue to struggle to find workers to produce goods.

Behind the Numbers:

Taken in tandem, this morning’s reports serve as a sign that some of the key drivers of freight demand remain healthy in the 3rd quarter. On the retail side, the softness in August numbers was offset by the revisions in July. Some of this is probably the result of changing seasonality, as consumers have pushed more spending into July in recent years to take advantage of Prime Day and all of the related deals that occur during that time. The year-over-year growth still looks impressive, even once you consider that rising gas prices and higher inflation in general is driving some of the high headline numbers. Things are shaping up nicely for the peak holiday shopping season, and sales are likely to be very strong this year.

The industrial production results were also good, but the number of areas of weakness is a bit troubling. Mining and oil exploration is expanding rapidly in the economy, and is dominating some much of the industrial activity. Even outside of the strong mining production numbers, much of the production in machinery and primary metals is for things supporting the mining sector. Demand seems strong for most sectors, but the inability to meet demand is becoming an issue for more and more industries within the sector.

Still, from a freight demand perspective thing look healthy in the 3rd quarter. The August numbers may be the last clean look we get at economic results for a while, as the hurricane could derail September results and subsequent months may be boosted by rebuilding efforts.

Ibrahiim Bayaan is FreightWaves’ Chief Economist. He writes regularly on all aspects of the economy and provides context with original research and analytics on freight market trends. Never miss his commentary by subscribing.