As part of our overall coverage of freight markets, FreightWaves publishes a summary of the changes in the economy over the past month, both in terms of the data releases and in developments in public policy. The Economic Roundup is designed to synthesize the events of the past month as they relate to freight markets, and provide a guide on trends to keep an eye on in the upcoming month. The Roundup is published on the first business day of each month with the next release scheduled for Monday, July 2nd.

Overview:

Economic conditions as they relate to freight continued to make positive strides thus far in the 2nd quarter. Much of the data released in May (predominantly covering April activity) from the goods side of the economy posted solid gains.

The economy slowed slightly overall in the 1st quarter of the year, as poor weather and a spending hangover from a robust 4th quarter restrained growth at the start of the year. However, the fundamentals remain solid in the economy, with a renewed appetite for business investment and solid consumer conditions forming a sound foundation for growth going forward.

Readings to this point in the 2nd quarter suggest that the economy is regaining some momentum. Job growth remains fairly solid despite softening slightly in recent months. Consumer spending, particularly on retail goods, has shown some signs of life after struggling early in the year. In addition, industrial production has continued its gradual acceleration, helped by rising oil prices, a weakened US dollar, and healthy demand from businesses and consumers.

All is not rosy in the economy, however. Housing activity continued to disappoint during the springtime months, with sales and starts falling below expectations during the month. In addition, the trade deficit fell for the 2nd straight month, but the decline was driven by a decline in both imports and exports. This means that there was less trade activity overall.

Still, the economy is likely to experience stronger growth overall this quarter. This means that trucking carriers will likely continue to find themselves operating at or near capacity in order to meet the demands of the economy. Shippers, already facing rising transportation costs and shipping delays, are likely to continue to investigate alternative means of freight such as rail and intermodal. This will likely put upward pressure on rates across different modes of freight

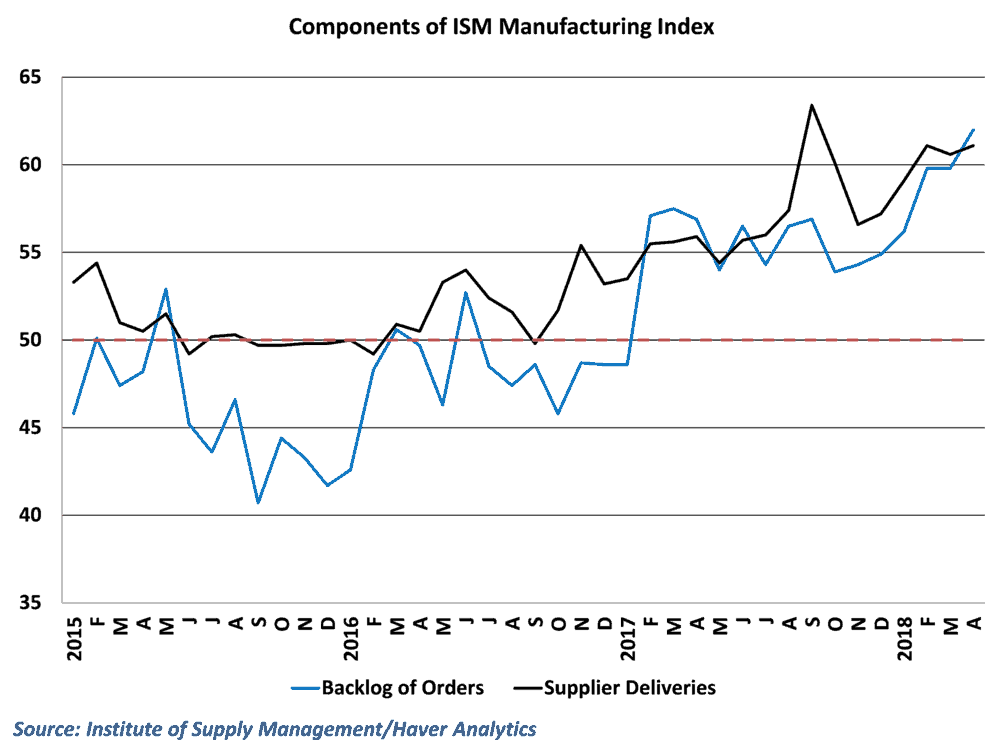

Manufacturing and industrial production

Results on the manufacturing side of the economy showed robust activity despite some challenges for the sector. Industrial production rose a healthy 0.7% in April, with sizeable gains across most major industries. The broad-based gains helped offset a sizeable decline in auto production and helped manufacturing post one of the largest gains of the year. Factory orders also posted strong gains excluding aircraft, which suggest that manufacturing will likely remain strong going forward

The survey data in the manufacturing sector also suggests that manufacturing activity is robust. Data from the Institute of Supply Management tapered slightly but remains well into expansionary territory. Survey responses suggest that demand is so strong that businesses are having a hard time finding workers and carriers to fulfill existing orders.

Trend to watch: Fed survey responses suggest that labor shortages have stretched beyond the transportation industry, as manufacturers often find themselves struggling to find available workers to fill positions. Hiring has picked up in the manufacturing sector this year, but like trucking, much more needs to be done.

Retail and inventories

Retail performance continued its spring rebound with another solid month of sales in April. Like the results in the manufacturing sector, gains in retail were fairly broad-based during the month, with only a handful of industries in the sector registering declines. Retail was one of the weak points of the economy throughout most of the 1st quarter, but consumer confidence remains high and sales growth should continue going forward. E-commerce remains a standout in the retail space, as growth continues at a double-digit pace.

Inventories grew during the month, but low inventory/sales rations suggest that inventory turnover remains high. This is particularly true in the retail sector, where the inventory-sales ratios tumbled in the 3rd quarter of last year and has yet to recover fully. Lean inventories help companies manage their warehousing costs, but put significant pressure on carriers to replenish inventory stocks more frequently

Trend to watch: Beige book responses suggested that there was some softening in consumer spending in the early part of May. Stronger consumer spending is expected to drive most of the improvement in overall GDP growth in the 2nd quarter, but high gas prices and rising interest rates may take some of the steam out of the US consumer.

Labor markets

Job growth picked up in April, but the pace of hiring fell a bit short of expectations with 164,000 jobs added. Despite the disappointing jobs number, unemployment fell below 4% in the economy for the first time since 2000 as the size of the labor force shrunk during the month. Labor conditions remain very tight in the economy, with other indicators such as job openings and jobless claims hinting at a labor market that is running out of room for improvement. However, wage growth has been particularly stubborn, hovering around 2.5% since the end of 2015.

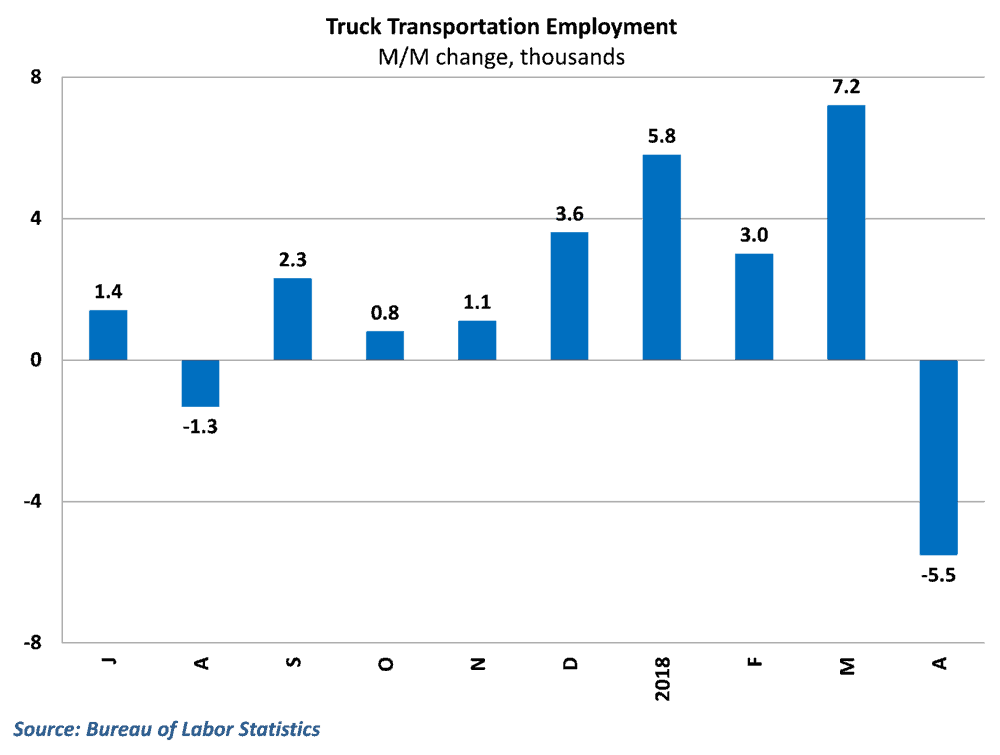

Trucking hires took a significant step back during the month, posting a sizeable decline in employment despite the better overall numbers for the economy. Carriers are still trying to find ways to recruit new drivers and retain existing ones, but there still is a lot of work to be done on that front.

Trend to watch: Results from May came in significantly stronger than in April on all fronts. Trucking hires reversed the decline in April and have now been positive in eight out of the past nine months. A reacceleration in hiring would go a long way in alleviating the current capacity crunch.

Housing and construction

Housing data was disappointing throughout the course of the month, as home sales, home start, and value of construction data all fell well short of expectations in April. Existing home sales are now more than a full percentage point lower that at this point last year, while new homes sales saw a decline in April and downward revision to data from earlier in the year as well. Starts have also sputtered, pulling back in April as multifamily starts experienced sharp declines

Home sales typically drive demand for large appliances, furniture, and building materials for renovation, while starts boost freight demand for lumber, sheet rock, and other construction materials. The hope was that once weather warmed up after the cold winter, housing would kick into gear. However, the data from this month and the number of building permits for future construction suggest that housing will likely continue to disappoint in the 2nd quarter.

Trend to watch: The housing market continues to face significant supply concerns, which has driven up prices considerably in recent quarters. If the pace of housing starts does not pick up in upcoming months, this could become a real problem for the housing market. Rising interest rates may send households scrambling to buy now, and if the supply is not there, affordability will become an issue.

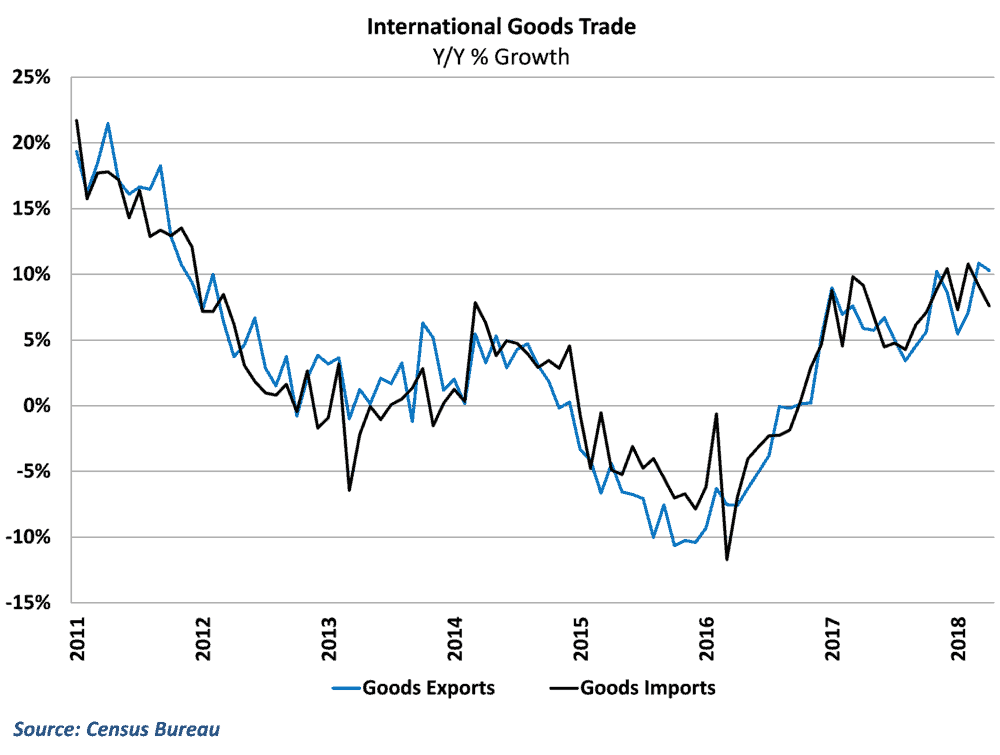

International Trade

In international trade, the goods deficit fell for the second straight month. However, the narrowing deficit was the byproduct of a decline in the total value of goods traded. Both exports and imports declined in April, with the fall in imports being larger than the fall in exports.

The still seems to relatively little evidence that some of the targeted tariffs announced by President Trump’s administration are having significant effect. Still, increasingly protectionist nature of US trade policy is not going to be good for trade volumes going forward. Right now, exports and imports are both experiencing healthy year-over-year growth, but this could easily change as trade tensions escalate.

Trend to watch: The total value of traded goods has now fallen in two out of the last four months. While there wasn’t much evidence of a big impact coming from tariffs, it will be interesting to see if these policy changes do begin to affect the data in upcoming months.

Ibrahiim Bayaan is FreightWaves’ Chief Economist. He writes regularly on all aspects of the economy and provides context with original research and analytics on freight market trends. Never miss his commentary by subscribing.