As part of our overall coverage of freight markets, FreightWaves publishes a summary of the changes in the economy over the past month, both in terms of the data releases and in developments in public policy. The Economic Roundup is designed to synthesize the events of the past month as they relate to freight markets, and provide a guide on trends to keep an eye on in the upcoming month. The Roundup is published on the first business day of each month with the next release scheduled for Monday, December 3rd.

Overview:

Economic conditions remained generally solid throughout the month for portions of the economy that drive freight demand. As has been the case for the past several months, strength in consumer spending and business investment continue to drive overall demand for goods transportation in the economy. All is not perfect, however, as construction and housing activity continue to lag behind the rest of the economy. In addition, trade remains a general source of weakness in the economy, as import growth continues to outpace gains in exports

On the supply side, trucking capacity continues to expand gradually. The number of employees on payrolls in the economy continues to make positive strides, and the pace of hiring within trucking is exceeding the pace of hiring in the rest of the economy. The combination of moderating demand and continued additions to capacity has caused some easing in prices through September, and tougher comparisons should lead to continued moderation in rate inflation going forward.

GDP

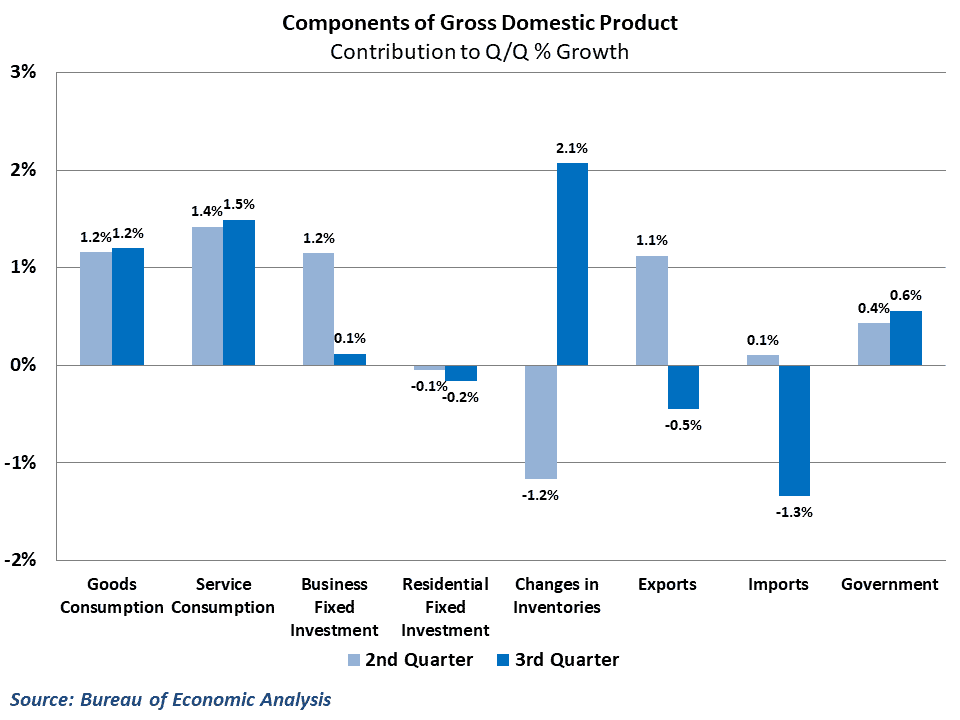

Initial estimates of US GDP for the 3rd quarter showed that the economy grew at a 3.5% pace, down from the 4.2% pace seen in the previous quarter. Consumer spending posted another strong quarter, growing at a slightly faster pace than in the 2nd quarter and contributing 2.7% towards overall GDP growth. Inventory building activity added an additional 2.1% towards growth during the quarter, more than making up for the drawdown in the previous quarter.

These gains were offset by a sizable decline in net exports during the quarter. Much of the inventory build was composed of goods brought into the country earlier than expected by US companies looking to avoid tariffs. This led to a surge in imports during the quarter, while payback from the jump in 2nd quarter exports cause a decline in exports. Business fixed investment also slowed down during the quarter, driven largely by temporary declines in aircraft purchases.

Trend to watch: Behind all of the trade and inventory fluctuations, the economy has performed well over the past couple of quarters, and should continue to do so going forward. The declines in net exports and gains from inventory building likely won’t continue at the same pace in the 4th quarter, so look for growth to settle in the 2.5-3.0% range.

Manufacturing and industrial production

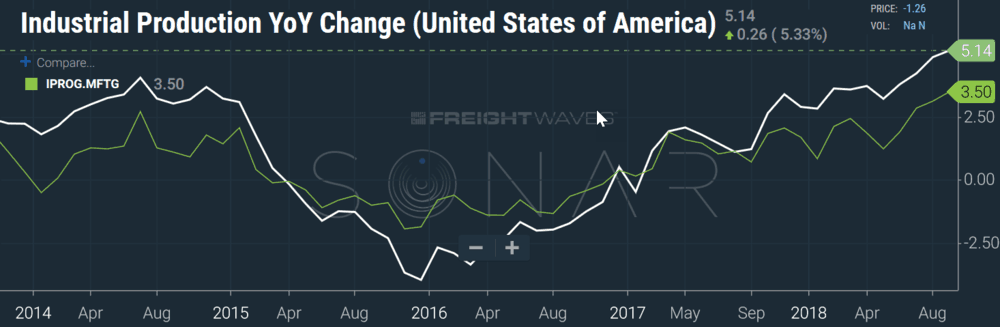

Industrial output continued to climb at a healthy pace in September, as total industrial production rose 0.3% from August’s levels. Year-over-year growth rose above 5% in total production for the first time since late-2010, as manufacturing and mining activity continue to be one of the highlights for freight demand and the economy overall.

Notably, there were only slight disruptions in the industrial sector from Hurricane Florence. The Federal Reserve estimated that total output was restrained by just 0.1% due to the hurricane. For comparison, Hurricane Harvey in 2017 subtracted approximately 0.75% from industrial production in August of last year. As a result, there is likely to be a slight rebound from lost activity, but not to the extent seen during last hurricane season. Of course, this would be offset in October by any impact from Hurricane Michael

Trend to watch: Weather aside, conditions for manufacturing and industrial output look generally solid. Yearly growth is likely to come down from the recent highs however, as comparisons to last year begin to get difficult in October.

Retail and inventories

Retail sales saw modest growth again in September, rising just 0.1% from August’s levels. Year-over-year growth plummeted below 5% despite the monthly gain, however, as comparisons to last year got more difficult. Much of the softness during the month was driven by a (possibly hurricane-related) decline in sales at restaurants and bars. Outside of this, retail performance was generally healthy and conditions remain favorable going forward Retail spending has now grown in each of the last eight months in the economy, and we expect holiday sales growth near 5% this year.

Inventories also advanced at a solid pace during the month, as businesses in the economy appear to be bringing in some imported goods earlier than usual in an attempt to circumvent any potential future tariffs. This has caused a slight uptick in inventory/sales ratios over the past couple of months.

Trend to watch: The recent decline in the stock market gives some pause to the optimism for the holiday season. Confidence has held up to this point, but the loss in equity values could affect consumers’ willing ness to spend in November and December

Labor markets

Labor market conditions were generally favorable during the month. The economy added just 134,000 jobs in September, though the timing of Hurricane Florence likely restrained job numbers. Other indicators were more positive, as jobless claims continued to trend near historical lows and wage growth hit the highest point in a decade

Trucking hires continued to make strides in September, adding another 4,900 workers to payrolls during the month. This marks the 12th increase in the last 13 months, pushing employment within the industry 2.2% higher than at this point last year. Capacity appears to be expanding in the industry, which should ease some pressure on rates going forward.

Trend to watch: The headline job numbers are going to have some weather-related noise for October. A broader perspective on the jobs numbers, including jobless claims, wages, and other measure of employment will give a clearer picture of the underlying strength.

Housing and construction

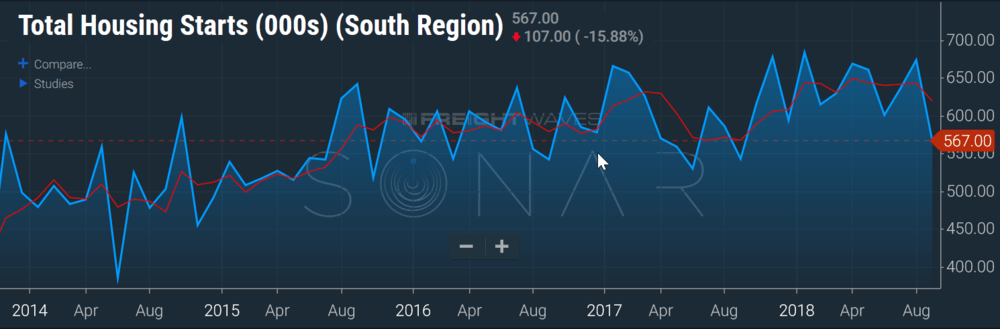

Housing data continued to surprise on the downside during the month, as both sales and building data fell well short of expectations.

Housing starts fell sharply to a 1.201 million annualized pace in September. Hurricane Florence again likely played a role in the poor results, however, as much of the weakness was concentrated in the South. Typically, more than half of all single-family housing starts take place in the South, so weather disruptions can significantly affect national numbers.

On the supply side, both new and existing home sales fell well short of expectations. Disruptions from the hurricane also likely played a role here, but home-buying activity has been plagued by affordability concerns. Rising mortgage rates and limited inventory have affected buying performance, and will remain issues for the housing sector even after weather returns to normal.

Trend to watch: Housing and construction a historically very sensitive to weather fluctuations. With Florence in September and Michael in October, housing data is likely going to be plagued with weather-affected dips and rebounds. It may be difficult to get a clear picture of the housing market until next year.

International trade

In international trade, the goods deficit widened again in September, reaching -$76 billion. The value of exported goods made some modest gains during the month after declining in the previous two months, rising by $2.5 million. However, this was outweighed by a gain in the value of imported goods, which rose by $3.1 million.

As mentioned earlier, part of the reason behind the rise in imports has been the fear of additional tariffs. The Trump administration has already implemented a 10% tariff on $200 billion in Chinese made goods, and is prepared to increase these tariffs to 25% in January of next year. In addition, the administration has threated to broaden the scope of the tariffs, targeting all imports from China.

By a similar token, many US importers likely brought in additional goods in July in advance of US tariffs on Chinese imports which were implemented in July and August. This has boosted import numbers recently, and contributed to the surging trade deficit.

Trend to watch: Tariff noise aside, there are some dynamics in trade fundamentals that are worth paying attention to. The recent strengthening of the dollar and the apparent weakening in China and Europe are likely going to shape the trade picture more than tariffs will over the next year.

Ibrahiim Bayaan is FreightWaves’ Chief Economist. He writes regularly on all aspects of the economy and provides context with original research and analytics on freight market trends. Never miss his commentary by subscribing.