There are ultimately no winners in a trade war, as FreightWaves has been reporting for the past several months, ever since mid-February when Trump first began considering raising tariffs. Open markets are good for everyone. If the current tactics are meant to negotiate fair trade deals, it can make sense. Raising tariffs in a vacuum, however, hurts everyone when it ends up suppressing supply.

As chief market strategist, Donald Broughton wrote for FreightWaves on March 2, “Open markets and deregulated transportation have been a powerful force in the creation of a thriving economy and some of the most productive transportation companies in the world.”

The United States is the world’s largest importer, and the economy is humming along in virtually all sectors. The top five importers in the U.S. are Walmart, Target, Home Depot, Lowe’s, and Dole, respectively. Combined, in 2017 those five alone accounted for 2,360,800 TEUs imported, according to JOC, SFG research. TEU stands for Twenty-Foot Equivalent Unit, which can be used to measure a ship’s cargo carrying capacity. The dimensions of one TEU are equal to that of a standard 20′ shipping container. 20 feet long, 8 feet tall. Usually 9-11 pallets are able to fit in one TEU. That is a lot of cargo, and 24 weeks into 2018, capacity remains tight.

The song of 2018 remains the same—and tariffs or no tariffs, it projects to remain so even as infrastructure on the rails and ports expand. Part of the explanation comes from the type of goods so far under siege: the current proposed tariffs are centered on goods of relatively low value and high density. The manufacturing process of goods as raw materials moves “downstream.” When they are processed into finished products, cost increases of the original materials are often filtered out of the final product price.

Also, intense competition in some markets will actually keep consumers from feeling the pinch—at least at first. With increased competition between companies, it may turn out that companies in these markets would rather absorb the costs themselves rather than passing on increased costs to customers.

Another factor is timing. There’s a lag between the increased price of metals and when manufacturers and producers of goods will actually pay for new steel and aluminum. Meanwhile, some companies have responded to higher prices of aluminum and steel by ramping up U.S. domestic production, such as a near-doubling of planned solar panel capacity.

So long as the tariffs on aluminum will only add an additional one to two cents to the cost of canned beer the issue is “measurable, but still relatively minor,” as John Mothersole, director of research in IHS Markit’s pricing and purchasing service, said to the L.A. Times.

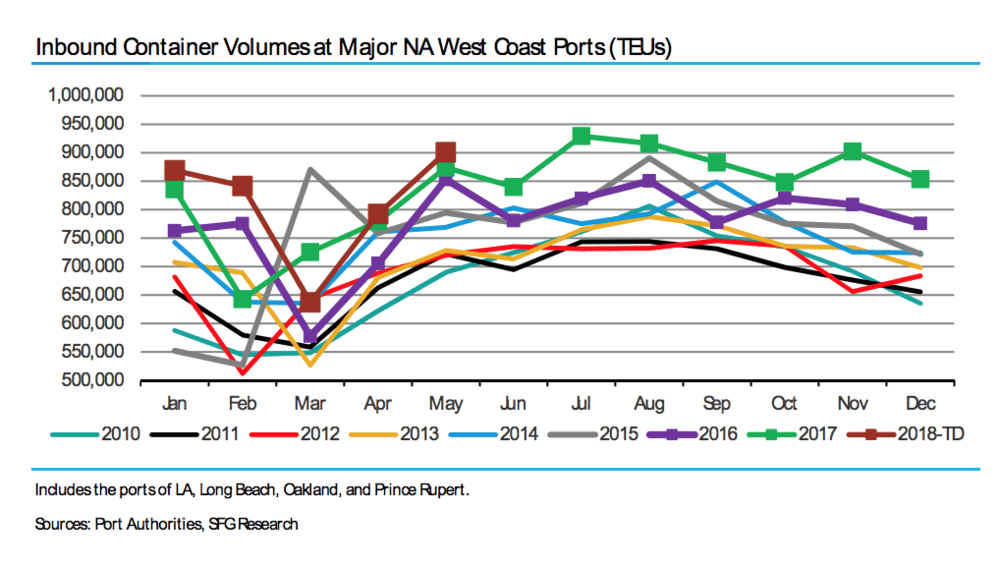

Encouragingly, recent international ocean and airfreight volumes aren’t showing signs of a trade-fear related slowdown, as we move bravely toward July.

According to SIG Susquehanna analyst Bascome Majors, the sample of May container volumes of top global ports were up in the low-to-mid single digits Year over Year, and also ahead of historic Month over Month seasonality. Majors’ team views May’s seasonal outperformance as notable given: May to July is typically the “set-up” for the August to October peak season, with trade velocity over the former period a good directional indicator for peak strength/weakness, and 2) the trade dispute between the U.S. and China remains fluid (e.g., last Friday’s 25% levy on $50B worth of Chinese imports met with a similar measure on U.S. exports). They look to “hard” port (and airport) data for evidence of a trade related slowdown, and they aren’t seeing it. Not yet at least.

For Asian Ports, total container volumes rose 3.4% Year over Year in May (vs. a +10.9% comp), slightly below April’s +4.3% (which was off an easier +6.5% comp), though above March’s +2.4%. Sequentially, volumes were up 4.9% Month over Month, ~200bps above the average Month over Month trend of +2.9% for the last 5 years (range of +1.2% to +5.8%).

For West Coast Ports, total container volumes were up 4.0% Year over Year in May (vs. a flat comp), slightly below April’s +4.5%, though above March’s CNY-impacted -7.8%. On the import side, volumes were up 3.1% Year over Year (vs. a +2.4% comp), up from April’s +1.7% and above March’s -12.1% (also CNY-impacted). Sequentially, volumes rose 13.7% Month over Month, fully ~450bps better than the average Month over Month trend of +9.2% for the last 5 years (range of +1.1% to +20.9%).

Meanwhile, Maersk, the world’s largest container shipper, announced on June 5 they are raising their rates on Freight of All Kinds (FAK), focused especially on the corridors between the Mediterranean and Far East Asia. They specifically said, “These rates are unaffected by, and do not affect, any tariff notified, published or filed in accordance with local regulatory requirements.” Supply is high across the globe, and for now the trade war talk remains rhetoric.

Stay up-to-date with the latest commentary and insights on FreightTech and the impact to the markets by subscribing.