A weekly look at what occurred in the oil markets of the U.S. and the world this past week.

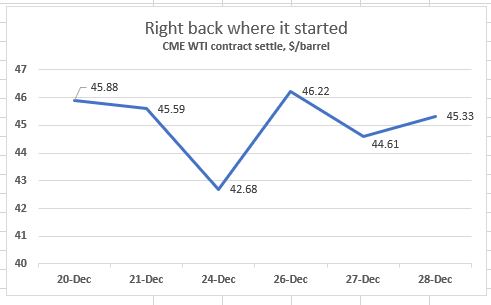

–After being yanked up and down during a week that is supposed to be fairly quiet, oil prices closed the week Friday at about the same level where they settled one day before last weekend.

But that doesn’t tell anything about what really happened. After a settlement in the WTI market last Thursday at $45.88/barrel, the settlement this past Friday was $45.59, just 29 cts different after that roller coaster ride. In the interim, there was a Christmas Eve collapse of almost $3, a surge the day after Christmas of more than $3.50, another drop of more than $1.50 a day later and then a strong move upward at the end of the week to bring us right back where we started.

That wasn’t the case with the ultra low sulfur diesel market, which finished up the week down almost 7 cts from where it was a week earlier. The CME ultra low sulfur diesel contract settled Friday at $1.6647, down from $1.7327 a week earlier.

Focus during the week shifted away from discussions about likely market imbalances next year, but not because anybody believes they are going away. Note that OPEC’s planned reduction in output of 1.2 million b/d—two-thirds of it by OPEC, the other by Russia and its friends–doesn’t even go into effect until January.

Instead, several analysts led mostly by Goldman Sachs and long-time energy economist Philip Verleger stressed the importance of trader selling as a result of hedging activities. With U.S. production surging but doing so on the back of a lot of borrowed money, those banks and other financing sources have been demanding that producers hedge. That hedging is generally done with put options, where a producer buys a put option that allows them—but not requires them—to sell oil at a designated price, known as the strike price. If the market price dips toward that strike price, the seller of the put option, likely some sort of financial firm, needs to sell outright futures contracts. Human input will go into the decision of when to sell, but it’s then built into an algorithm, so it’s on automatic pilot as the price starts to decline toward that strike price where they’re going to stuck having oil “put” on to them. Both Verleger and Goldman—and others—have stressed in recent weeks that the selling of futures tied to that hedging has been a major downward push on prices and is mostly divorced from market fundamentals. But there is also a view that given where a lot of hedges were placed, much of that hedge-related selling is probably done…for now. The key takeaway from the events of the past few weeks is that while you can look at all the supply and demand figures you want, but with so much oil hedged out of the expanding U.S. oil patch, what goes on with that hedging can have—and just did have—a significant impact on price.

–The theory that hedge-related selling might be driving the market lower is not universally shared. A report from the well-respected firm of Tudor, Pickering & Holt did not describe the downward movement as being about fundamentals, instead describing it was “less fundamentally driven and more a function of the overall market meltdown as increased equity volatility and growing macro concerns have weighed on a number of asset classes.”

–Has this last price drop started to impact drilling activity? The latest rig count from S&P Global Platts indicates it has. The rig count reported by Platts dropped last week to 1,137, a drop of 28 and the lowest level since April. All that decline came from rigs that were drilling for oil, as opposed to natural gas or a combination of oil and natural gas. The numbers are still more than last year at this time, however.

–During the recent market decline, commodity diesel prices trailed the market. For example, based on CME data, on December 19 the spread between ultra low sulfur diesel prices to crude oil stood at 28.6, meaning the value of one barrel of ULSD was $28.60 more than the value of a barrel of crude. By December 27, it had fallen to 25.9/barrel. On Friday the gap stood at $24.58/b. The lag in the diesel market evidenced over the past few days might be a function of end-of-year tax selling. Petroleum Argus reported: “Part of the weakness on the US Gulf Coast comes from an effort to clear taxable inventory before the end of the year. Texas’ ad valorem tax tends to prompt a sell-off from Gulf coast refiners, and this year’s impact was particularly severe.”

–South of the border, Mexico’s slow deterioration of its oil position continues. Its oil output in November declined 2.7% from just a month earlier to approximately 1.71 million b/d. In 2013, it averaged 2.52 million b/d. The grand experiment with outside investment is starting to look like a flop and with current President Obrador essentially hostile to that initiative, it’s not clear what can turn around this long slide. State oil company Pemex itself has predicted output to fall to less than 1.6 million b/d by the end of 2019 barring a dramatic turnaround.

–Any sort of commodity trading is ultimately a zero-sum game. The winners aren’t always traders; they can be individual motorists or truckers or railroads who are now seeing their fuel prices slide. But it’s not always easy for the losers. Last month, the head of a natural gas-focused trading firm released this remarkable video in which he emotionally tried to apologize to his clients for what he had lost in the natural gas market, mostly over the course of a mere week. And with the decline in oil over the last few weeks came the report that two leading officials at Chinese trading company Unipec had been fired as a result of a bet on rising oil prices, according to multiple news reports. The two were identified as Chen Bo, Unipec president and Zhan Qi, the Communist Party secretary. The irony is that China has net import dependence of about 65%, while the U.S. is down near 12%. As the world’s biggest importer, it benefits more than any other country by a decline in the price of oil. Yet its biggest trading company apparently was long and looking to benefit from higher prices.