Southwest Airlines (NYSE: LUV), incorporated in 1967, has been one of the most profitable and best-performing airlines in the United States for decades. Southwest has maintained a consistent Investment Grade credit rating from all three ratings agencies, which is rare among airlines. It has been the only airline to consistently return capital to its investors year after year, and in 2018 recorded its 46th consecutive year of profitability.

Besides an innovative point-to-point network and a focus on customer satisfaction, one of Southwest’s key differentiators has been its fuel hedging program, which it started in 1994. The idea was that by locking in prices for its largest variable cost, Southwest could protect itself against upward volatility in fuel. When other airlines were using their cash to pay for runaway jet fuel prices, Southwest would be in a position to invest in new aircraft, improve its operations and take market share.

Southwest’s fuel hedging started slowly – it was outsourced and relatively simple, trading contracts representing just 20 percent to 30 percent of the airline’s fuel needs up to six months in advance. That changed in 1998, as Asian economies melted down and OPEC crashed crude oil prices to $12/barrel. It was at that point that Southwest executives got serious about locking in these extremely low prices and hedging a greater percentage of its overall fuel spend. Over the next five years, Southwest was paying anywhere from 25 percent to 40 percent less for its jet fuel than its competitors, and by 2008, the airline was hedging 70 percent of its fuel needs.

“Being unhedged is the ultimate short position. You’re betting every day that the price of fuel won’t go up,” Barry Siler, a Houston-based commodities trader who consulted with Southwest on fuel hedging, told USA Today.

Siler’s point is true for truckload transportation as well; if you’re a buyer or seller of trucking capacity, you already have a position in the market. Shippers are naturally short, because they want trucking rates to go down. Carriers are naturally long, because they want trucking rates to go up. To date, neither shippers nor carriers could do anything to hedge their natural positions, but that changes on Friday, March 29, with the launch of the first Trucking Freight Futures contract on the Nodal Exchange.

The Southwest Airlines example especially applies to how shippers would use Trucking Freight Futures, because in both cases the party would likely be covering a naturally short position. Southwest would buy crude oil contracts and take a long position in the futures market to hedge its naturally short position.

Imagine that Southwest bought West Texas Intermediate (WTI) at today’s price, $58.32/barrel, 12 months in advance. If the price of oil – and therefore jet fuel – went up over the course of that year, against airlines’ natural position, Southwest would be protected, paying a lower price than its competitors. If the price of oil and jet fuel went down, then Southwest might end up paying more than its competitors, but at least the airline would know what its costs were going to be ahead of time.

Beginning March 29, shippers, carriers, third-party logistics providers and speculators will be able to trade 11 different trucking freight futures contracts. Four of those contracts represent “baskets,” or averages of different lanes, while seven contracts are based on specific lanes. Starting with the lane-specific contracts first, market participants will be able to buy contracts for Los Angeles to Seattle, Seattle to Los Angeles, Los Angeles to Dallas, Dallas to Los Angeles, Chicago to Atlanta, Atlanta to Philadelphia, and Philadelphia to Chicago. Those lanes can be combined into three regional baskets: the bi-directional L.A.-Seattle lanes form a ‘West Coast’ basket; the bi-directional L.A.-Dallas lanes form a ‘South’ basket; and the Chicago-Atlanta- Philadelphia unidirectional triangle forms an ‘East Coast’ basket. Finally, a contract based on the national average dry van spot rate will be available for trading. All of these contracts will be cash-settled monthly based on DAT’s price assessments.

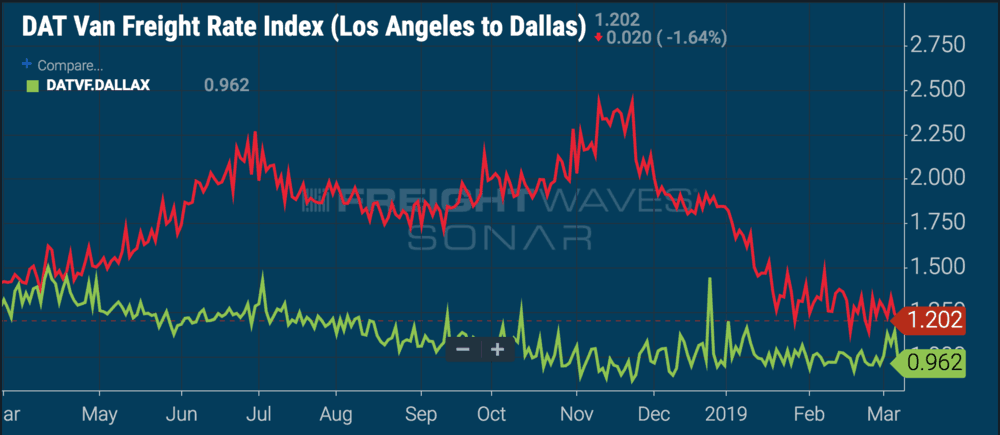

The chart below displays a year’s worth of dry van spot rates from Los Angeles to Dallas (DATVF.LAXDAL) and compares them to dry van spot rates from Dallas to Los Angeles (DATVF.DALLAX).

( Chart: FreightWaves SONAR )

( Chart: FreightWaves SONAR )

Last year the lane from Los Angeles to Dallas saw a seasonal run-up beginning about in March and extending through the end of June, during which spot rates rose from less than $1.50/mile to $2.25/mile. A shipper moving goods from Los Angeles into Dallas – or secondary markets like Phoenix, which is highly correlated – might want to take advantage of current low rates to keep its costs down in the future.

It is unlikely that a carrier would take the other side of a Los Angeles to Dallas June contract priced at just $1.20/mile, because the carrier knows June prices are going to be higher than March prices. The question is by how much? The carrier might look at economic data, recent earnings updates from publicly traded carriers, and its own volumes and decide that this summer peak is going to be softer than 2018. Imagine, in this hypothetical scenario, that the bid-ask spread comes together at $1.85/mile. In other words, what the shipper asks and what the carrier is offering meets in the middle at $1.85/mile. If prices go above that, the shipper makes money; if the economy does poorly and prices never get that high at all, then the carrier still gets paid.

In both cases, the shipper and carrier can use their expectations for what the market will do to protect against worst-case scenarios and manage their respective costs and revenues better. Ultimately, hedging against its natural position allows a company to deploy capital more efficiently, since instead of maintaining a cash reserve to deal with unfavorable market volatility, it can protect itself with a financial instrument and use its cash to invest in its business.