Remember when people thought container shipping spot rates would peak around Chinese Golden Week last October? They weren’t even close. Then they thought year-end. Wrong again. Then they pointed to Chinese New Year, which starts next week.

That’s not going to happen either. Spot rates remain stratospheric. California port congestion keeps breaking records (there were 40 container ships at anchor in San Pedro Bay on Monday — a fresh all-time high). Liners are canceling voyages this month due to the port crunch, pushing even more volume to the months after Chinese New Year.

It now appears spot rates will remain strong all the way through the second quarter. They may ebb from current highs, but they almost certainly won’t crash.

This is exactly the scenario U.S. importers feared. They will have to negotiate their annual contracts — which generally expire by May 1 — in the midst of a spot-rate boom.

“The spot market has been insane … [and] timing is in carriers’ favor to negotiate contract rates, because spot rates are so high,” said Nerijus Poskus, Flexport’s global head of ocean freight, during a webinar presented by Flexport last week.

“The industry experts and veterans we talk with think that the first half might be a squeeze for the entire period,” said Patrik Berglund, CEO of Xeneta, a company that collects and analyzes contract-rate data, during his company’s latest market presentation.

“This is a historically strong seller’s market at the moment. We see that for the first half in total,” said Berglund, who added: “The high spot rates … have cascaded down into contract agreements, putting the squeeze on shippers worldwide.”

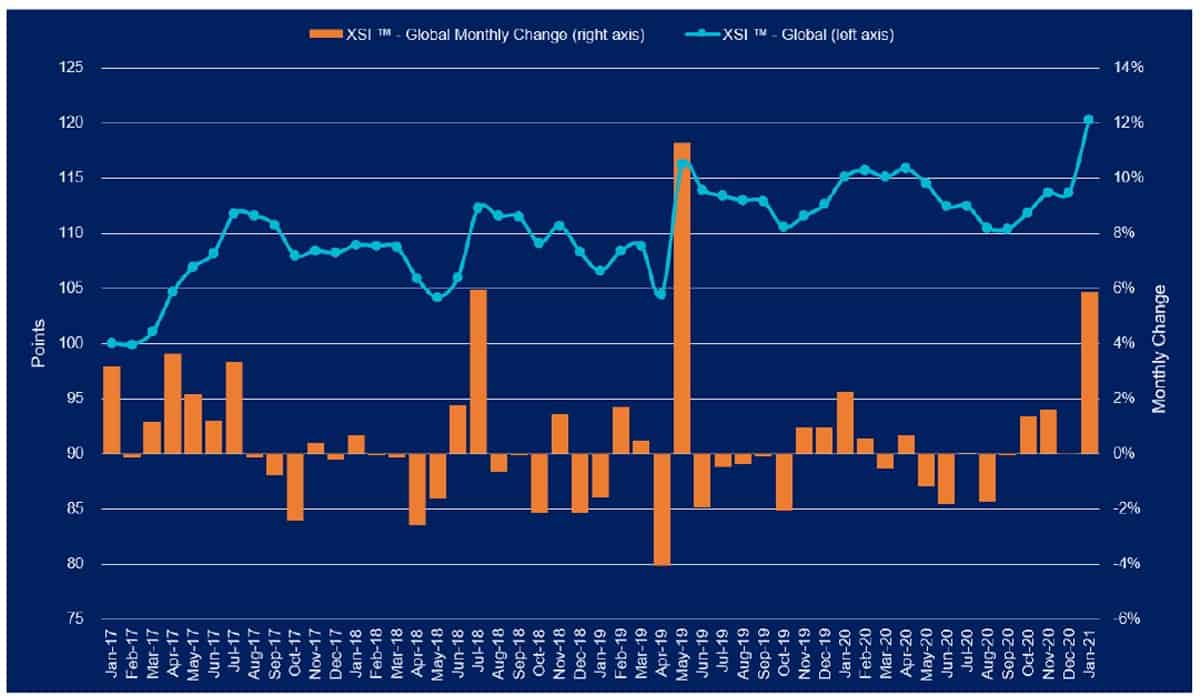

Contract rates could jump by high double digits

Xeneta’s XSI index tracks ocean contract rates. It rose 5.9% in January versus December, one of its largest ever month-to-month gains.

According to Thorsten Diephaus, Xeneta’s strategic accounts director, “If your contract is expiring May 1 and you’re asking whether you should go to tender or not, I can only recommend you go to tender.

“Because what we have seen with companies not going to tender when their old prices expired in December [when European contracts renewed] is that they are more or less close to the spot market with all of the volumes they’re moving.”

Those that pushed ahead with long-term contract tenders are seeing “an increase of 30-50% or sometimes probably even more on certain trades,” said Diephaus.

That sounds like a lot, but it pales in comparison to spot rates, which in many cases are quadruple contract rates. According to the Freightos Baltic Daily Index, China-West Coast rates (SONAR: FBXD.CNAW) spot rates — excluding thousands in extra charges — were $4,262 per forty-foot equivalent unit (FEU) on Friday. China-East Coast spot rates (SONAR: FBXD.CNAE) were $5,651 per FEU.

SeaIntelligence Consulting CEO Lars Jensen said during the Flexport webinar, “We haven’t seen contract rates explode to the same degree as spot rates, but they have been coming up rapidly over the last few weeks.

“Most contract rates took a nosedive back in 2016 when the market crashed,” Jensen recalled. “The carriers have tried but failed to increase contract rates ever since. It seems highly likely that 2021 will be the year when they actually succeed in doing that.

“And if they do bring contract rates to normal pre-2016-market-crash levels, in very round numbers, what you’re looking at is a 70% increase on the trans-Pacific and a 50% increase in Asia-Europe,” said Jensen.

How shippers could minimize spot exposure

Today’s spread between long-term contract rates and spot rates “is unprecedented,” said Berglund. “If you are pushed onto the spot market, you’re not talking about a 30-40% cost increase. You’re talking about a transportation budget that goes through the roof.”

One way shippers can limit the damage is to more accurately predict volumes — an even taller order than usual in 2021 due to COVID-driven demand uncertainties.

“Predicting the volumes you are going to ship has never been as important as it is this year,” stressed Poskus. “MQC [minimum quantity commitment] divided by 50 or 52 [weeks] is just not going to cut it anymore. If you cannot predict [quantity] well, you will end up paying more.”

Diephaus warned, “In this kind of market, if you award a carrier or supplier five boxes a week and you only bring three boxes a week, I bet the carrier will cut your allocation to three boxes only. For the remaining boxes, they will charge you on top. This is something we already see.”

How carriers could hike spot exposure

“With these rate levels, I would also be very surprised if carriers did not reduce their long-term [contract] market share on some major trades and add more on the spot market,” Diephaus continued.

What that means, in practice, is that shippers must further diversify their ocean freight suppliers this year.

“If you’ve used one carrier for a lane in the past, you may need to split it between three. The carrier from the past may not accept the rate levels you ask for and reduce your [contract] capacity. We already see this happening. Customers need to nominate more suppliers for the same volumes they had in the past.”

According to Jensen, “There is going to be quite a bit of tension between carriers and shippers in contract negotiations in 2021. Carriers want to maximize their own profitability, which is perfectly fair in any market. But that comes at a price: more tension in their relationships with their customers.” Click for more FreightWaves/American Shipper articles by Greg Miller

MORE ON CONTAINERS: Trans-Pacific trade crashes into max-capacity ceiling: see story here. COVID outbreak could cripple California container ports: see story here. Inside California’s colossal container-ship traffic jam: see story here. ‘Blue wave’ could spur stimulus on top of stimulus: see story here. Container shipping 2021: hangover or party on? See story here.