Shares of J.B. Hunt Transport Services (NASDAQ: JBHT) gapped down as the third-quarter conference call progressed Friday. The commentary on near-term expectations didn’t appear to satisfy investors who were braced by management for a continuation of intermodal service headwinds, which have resulted in an elevated cost structure, at least through the fourth quarter.

Stock under pressure after missing recently raised forecasts

Shares of JBHT entered the call down more than 4% on the day, but as the realization that a turnaround in rail service may take time and cost headwinds were likely to persist for the rest of the year, the stock moved lower, finishing the call down 8%.

This was not surprising, as some may say the shares were priced for perfection, up 21% year-to date and approaching a doubling in value since the depths of the pandemic. Further, analysts were bullish on the trucking industry, taking up their forecasts for the third quarter. The expectation was that changes in buying patterns from services to hard goods, continuous inventory replenishment and a big peak season amid a backdrop of continuous tightening in truck capacity would allow the carriers to capture incremental profits in the period.

In the race to raise trucking forecasts, several analysts raised their earnings estimates for the Lowell, Arkansas-based company even though it isn’t a pure trucking play and still sees roughly 60% of its operating income come from its intermodal segment, which has been plagued by slow rail service.

Management noted that service constraints in intermodal were aplenty in the quarter as the railroads slowly brought back furloughed employees and equipment to meet rising demand. Further, many of J.B. Hunt’s customers struggled to find the headcount needed to unload the influx of containers arriving at their facilities. The result was lost business and a higher cost structure. Additionally, operating losses in the company’s brokerage segment widened as gross margins fell on rising capacity costs in a tight truck market.

The combination produced a 9 cents per share earnings miss on a $1.27 consensus estimate, a forecast that was raised 20 cents per share over the three-month period heading into the print, according to Yahoo Finance. The $1.18 third-quarter 2020 result was ahead of the prior year’s $1.10, but that period included $0.30 per share in arbitration charges related to the final award to BNSF Railway (Berkshire Hathaway, NYSE: BRK.B).

Taking the long approach

On the earnings call, management said they would remain steadfast on their long-term approach to the business, which includes a focus on customer retention, balancing capacity additions with the sustainability of longer-term returns on those assets and continuous investments in technology and improved service throughout the network.

When pressed on why they didn’t abandon lower price customer contracts in favor of higher spot prices available in the market currently, management said they didn’t believe it would be a prudent long-term strategy. They said not meeting minimum capacity requirements when many of their customers are approaching them for more equipment hurts customer retention and overall returns in the long run. They noted that many of their clients use multiple modes and services on the J.B. Hunt platform and that gains in one service offering could present an issue in another.

Intermodal struggles continue into 4Q

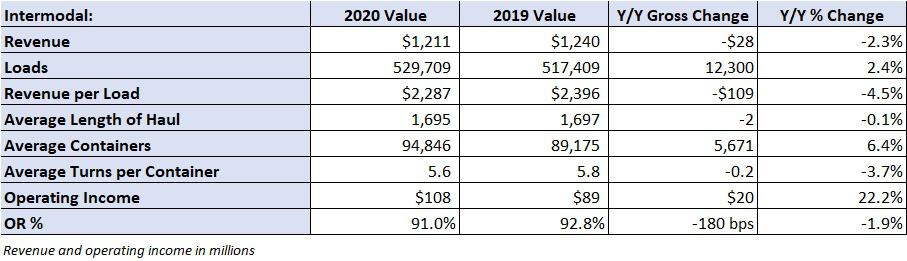

Intermodal loads increased 2% year-over-year during the third quarter, in line with domestic container movements on the U.S. railroads but lower than broader domestic intermodal volume trends. Load increases of 3% in the East and 2% on transcontinental shipments outpaced very modest declines reported by J.B. Hunt’s rail partners Norfolk Southern (NYSE: NSC) and BNSF Railway. Loads were classified as “heavily constrained” due to increased rail congestion and labor issues that resulted from the rapid surge in demand during the quarter.

Total intermodal revenue fell 2% year-over-year as revenue per load declined 5% (flat excluding changes in fuel revenue). Management said they were turning down thousands of loads per week to honor contractual capacity commitments.

Headline operating income was up 22% year-over-year at $108 million, but the 2019 third quarter included $44 million in charges related to the revenue-sharing dispute with BNSF Railway. Excluding the impact of the arbitration award, intermodal operating income was down 18% year-over-year. Surging import containers to the U.S. West Coast drove an equipment imbalance throughout the intermodal network. Management indicated on the second-quarter call that moving empty containers back to the West Coast would be a cost headwind in the third quarter, which it was. Cost increases in purchased transportation, drayage and labor as well as declines in revenue per load drove the weaker operating result.

Looking forward, the velocity of container movements on the railroads is expected to be a challenge into the fourth quarter. Fluidity in the network deteriorated throughout the third quarter, continuing into October. The new intermodal rate bid cycle has begun but any price increases gained may take a while to impact operating results. J.B. Hunt expects to reprice 10% of its contracts during the fourth quarter and 30% in the first three quarters of 2021, meaning it will likely be the second or third quarter before improved pricing bleeds through to results.

The long-term guidance for intermodal operating margins in the 11% to 13% range hasn’t been changed. Management expects to move closer to the goal over the next year, suggesting improvement from the current level of 9%.

Brokerage still on track to turn a profit in back half of 2021

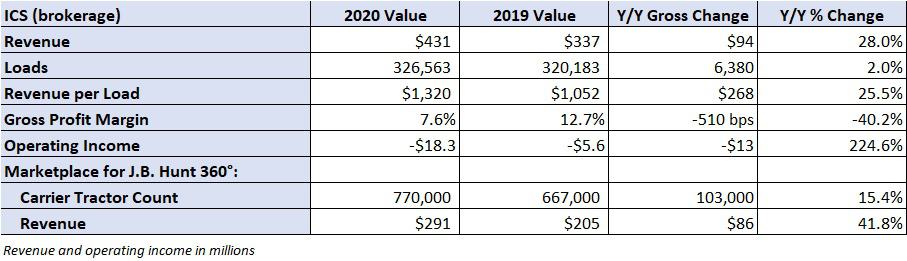

Brokerage revenue increased 28% year-over-year to $431 million as loads increased 2% and revenue per load climbed 26%. An improved freight mix and higher contractual and spot rates drove the improvement. Revenue generated through the Marketplace for J.B Hunt 360° platform jumped 42% to $291 million. The division saw losses widen to more than $18 million as gross margins collapsed, down 510 basis points to 7.6%. A tight capacity environment and contractual price competition were to blame.

Management said they expect the division to be profitable in the back half of 2021 as expenses as a percentage of revenue will ease.

Dedicated sees steady improvement, final mile turns a profit

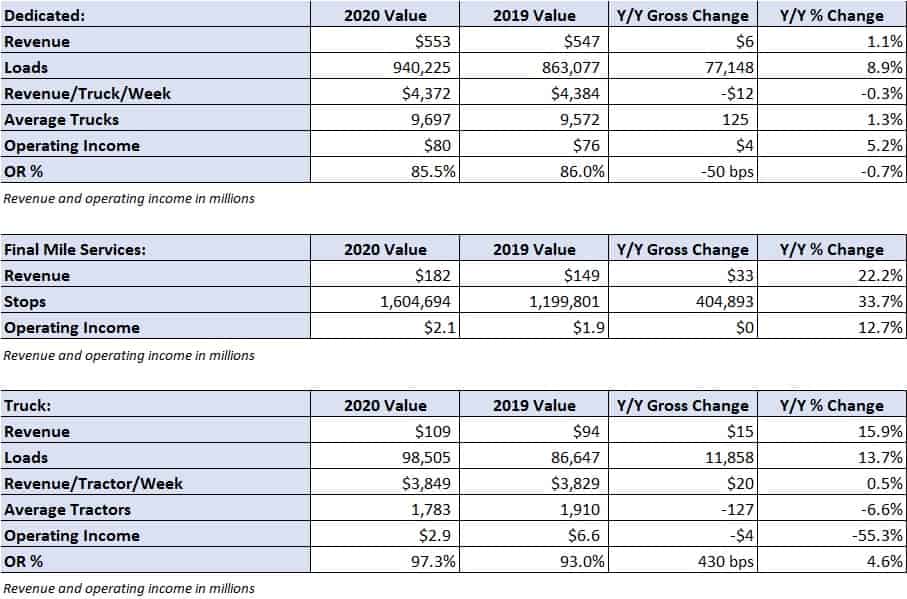

Dedicated revenue per truck per week was flat year-over-year but up 2% excluding fuel surcharges. The division has added 890 producing trucks to the fleet, surpassing the 2020 goal for additions in the 600 to 800 range. The fleet is expected to remain stable the remainder of the year.

Operating ratio (OR), expenses as a percentage of revenue and the inverse of operating margin, improved 50 basis points to 85.5%, When asked if they would raise the long-term operating margin forecast for dedicated from 11% to 13% given the recent success the unit is having, management cited increases in driver wages and recruiting costs and the return of travel and entertainment expenses as more of the economy reopens as reasons for the muted guidance.

Future prospects for the final-mile segment were described as the best seen in memory. Revenue increased 22% year-over-year with stops climbing 34%. Final mile was profitable in the quarter after a $5.2 million loss in the second quarter.

J.B. Hunt ended the period with $319 million in cash and net debt under $1 billion. The 1x debt-to-earnings before interest, taxes, depreciation and amortization (EBITDA) ratio remains the leverage target.

Shares of JBHT are off 9% on the day compared to a 0.5% increase in the S&P 500.