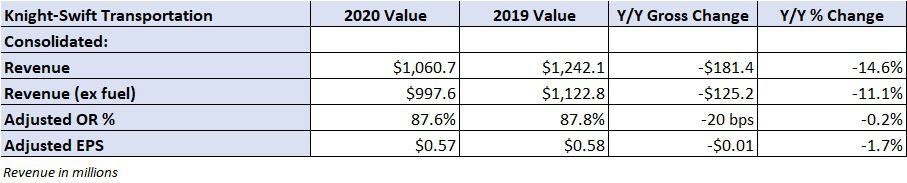

Knight-Swift Transportation Holdings Inc. (NYSE: KNX) keeps the better-than-expected earnings theme rolling forward. The Phoenix-based truckload (TL) carrier reported second quarter adjusted earnings per share of $0.57, easily beating analysts’ forecasts of $0.35.

Similar to other carriers, Knight-Swift saw freight demand rebound off of April’s bottom, “gradually” improving throughout the quarter and into July. “We are encouraged by the continued strength in freight demand in July; however, demand may be difficult to predict for the back half of the year,” stated the company’s earnings release.

Even with limited visibility into freight demand in the months to come, the carrier reinstated its outlook for earnings. Knight-Swift now expects full-year 2020 earnings per share of $2.15 to $2.30, which is better than its original guidance of $2.00 to $2.15 that was pulled in the first quarter over COVID-19 concerns. The new forecast is well ahead of current expectations calling for earnings of $1.75 per share.

Shares of KNX are only up 1% on the day, ahead of the S&P 500 which is flat, but continuing the strong run the stock has had in recent weeks. Shares are up 10% in the last week and almost 20% since the middle of June when analysts began to acknowledge June’s improvement in freight demand may result in estimates being too conservative.

The report was well-received by some equity analysts, including Deutsche Bank’s (NYSE: DB) Amit Mehrotra. “While we have been very bullish on KNX for a long time, and just yesterday in our “Early Morning Haul” daily, we said we see potential for a “relatively large beat”…today’s print and guidance reinstatement surpassed our most ambitious expectations.”

The second quarter’s adjusted number came with some noise. The company excluded $10 million, $0.06 per share, in COVID-19-related costs. It also reported $8.5 million in other income associated with gains from the company’s portfolio of equity investments. The figure was $3.1 million last year. Those tailwinds were offset by gains on equipment sales that were off $5.8 million in the period as used truck prices remain under pressure.

All in, Knight-Swift reported earnings per share of $0.47 on an unadjusted basis, a penny higher year-over-year.

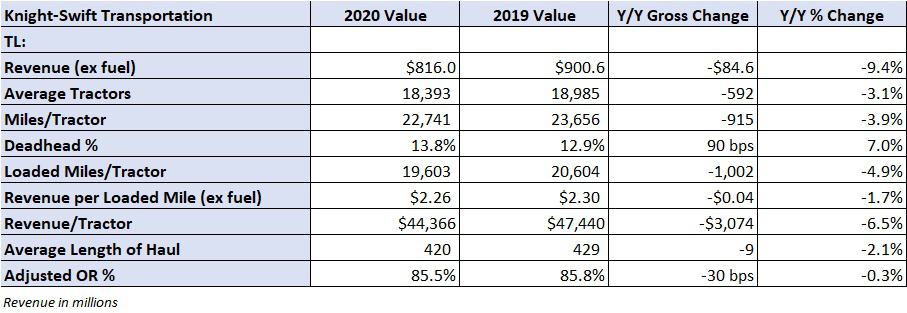

Trucking segment

Trucking revenue excluding fuel surcharge revenue declined 9.4% year-over-year to $816 million. Revenue per tractor declined 6.5% as loaded miles fell 4.9% and revenue per loaded mile excluding fuel declined 1.7%. Revenue per loaded mile was flat compared to the first quarter.

The division posted an 85.5% adjusted operating ratio (OR), 30 basis points better year-over-year. Knight’s trucking OR was 84%, with Swift’s at 85.3%. The combined total of salaries, wages and benefits expense and purchased transportation expense as a percentage of revenue declined 40 basis points year-over-year. Depreciation and amortization expense as a percentage of revenue increased 230 basis points. Again, declines in gains on equipment sales provided a headwind.

Gains on the sale or trade-in of tractors and trailers are booked as an offset to operating expenses on the income statement. As the industry has begun to work off excess tractor capacity created from record purchasing (from the third quarter of 2018 through the bulk of 2019) prices for used trucks have gapped lower. Operating cost inflation (notably on the insurance and claims line), tighter credit markets and sagging freight rates (until recently) have resulted in weaker equipment demand.

Knight-Swift expects its rate per mile to be positive in the third quarter. “We believe supply has and will continue to exit the market as evidenced by significantly lower Class 8 truck orders, a weak used equipment market, and lower transportation employment levels,” stated the release.

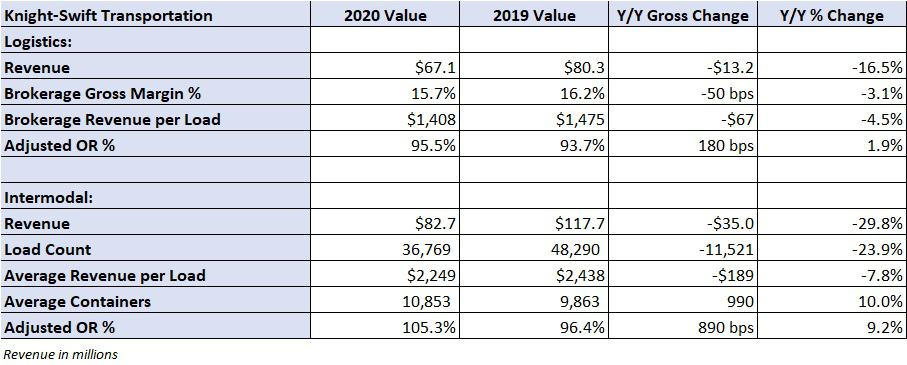

Logistics and intermodal

Revenue in the logistics segment, mostly brokerage, fell 16.5% year-over-year to $67 million. Brokerage revenue declined 14.2% as loads declined 10.1% and revenue per load was off 4.5%. Brokerage gross margins declined 50 basis points to 15.7%. “Margins were strong to begin the quarter and subsequently compressed, as the truckload market improved throughout the second quarter of 2020,” continued the release.

The intermodal division posted a $4.4 million adjusted operating loss, $8.6 million worse than the 2019 comparable period result. Loads were off 23.9% with revenue per load down 7.8%. “Continued market pressures, including the impact of the COVID-19 pandemic on port volumes” were named as the culprits.

Knight-Swift ended the quarter with $692 million in available liquidity and net debt of $734.2 million. The company generated $188.2 million in free cash flow, which includes a $93.4 million cash settlement related to the classification of independent contractors, in the first half of 2020.

Knight-Swift lowered its full-year 2020 net capital expenditures (capex) guidance to $500 million to $525 million (it was formerly $515 million to $540 million), deferring some facility projects and equipment purchasing until 2021. The average age of the company’s tractor fleet remained level with the year-ago period at 2.1 years.

Click for more FreightWaves articles by Todd Maiden.