On its first quarter 2020 earnings call, Landstar System Inc. (NASDAQ: LSTR) President and CEO Jim Gattoni said that dispatched volumes in April are running 20% to 30% lower year-over-year for the truck broker.

During the first 12 weeks of the quarter, volumes were about 5% below 2019 levels on average, even moving into positive territory briefly. However, the final week saw a 14% decline as shelter-in-place mandates spread and the automotive original equipment manufacturers (OEMs) closed. Management said that the current volume level, down 20% to 30%, could hold into and possibly through May.

On the call, Gattoni said that the current environment was “nothing like the company has ever seen before” when explaining how quickly volumes fell off.

Management said that the company could see earnings per share (EPS) of $0.70 to $0.85 during the second quarter if revenue remained 20% to 30% lower year-over-year. They highlighted the resiliency of the company’s variable cost structure wherein most expenses like its two largest (purchased transportation and agent commissions) move in lockstep with volume and revenue.

Landstar didn’t provide earnings guidance for the second quarter and management said that the earnings scenario provided isn’t intended to be construed as guidance. In 2019, Landstar generated $1.53 in EPS during the second quarter.

In comparison to dry van demand, the company is seeing slightly worse demand in the flatbed markets, which are heavily tied to industrial demand for auto, building products and metals. Typically, automotive-related freight accounts for 8% to 10% of Landstar’s revenue. This sector is only accounting for 2% of the company’s revenue currently.

Landstar only has approximately 2% to 3% of its revenue directly tied to the oil and gas markets, but a precarious supply imbalance driving oil prices into negative territory will weigh on the flatbed capacity demand-supply dynamic.

Gattoni said that they are already seeing idled equipment in the market and that he expects to see more trucks parked in both the flatbed and dry van markets until supply equilibrium is reached.

Pricing has held firm for Landstar so far with rates per load actually a little better when compared to normal seasonality. However, management said that the company’s Business Capacity Owners (BCOs) network sees a 30- to 45-day lag in rates compared to those providers more directly exposed to the spot market. This indicates that a dip in rates is likely in store for Landstar and management conceded that they have seen a small downtick in recent days on the call.

When discussing the prospects of a recovery, Gattoni said that it will really depend on how quickly the OEMs and building suppliers start producing again. However, for now Gattoni felt comfortable with the company’s ability to endure a prolonged downturn largely due to Landstar’s variable cost structure and strong balance sheet.

The company generated $99 million in operating cash flow during the quarter and closed the period with $211 million in cash and short-term investments and undrawn revolving credit capacity of $216 million. The company funded capital expenditures (capex) of $5.8 million and $86 million in dividend payments in the quarter. It also repurchased $116 million of stock, but plans to exercise “prudence” repurchasing future shares.

Excluding the share repurchases, the company was modestly cash flow-positive in the quarter after paying dividends and capex. While a pronounced downturn could challenge the company’s ability to fund all payments with cash flow from operations, management believes that the company has ample liquidity to fund those needs – employee salaries, payments to agents and capacity providers and fund its capex and dividend.

First Quarter 2020

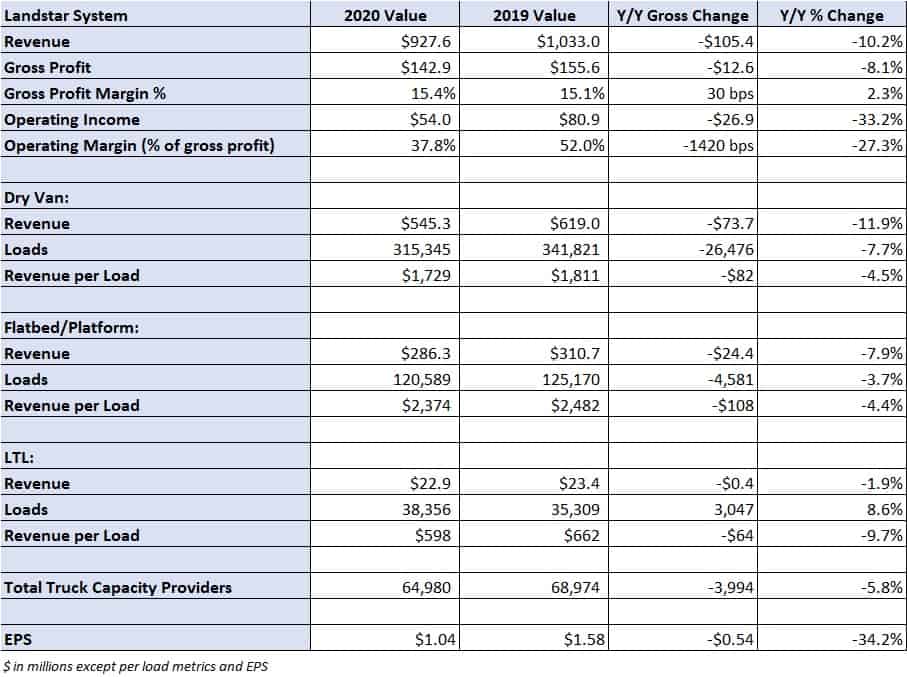

Landstar reported a 10.2% year-over-year revenue decline to $928 million in the quarter. Dry van revenue was 11.9% lower at $545 million, as loads declined 7.7% with revenue per load falling 4.5%. Flatbed revenue was 7.9% lower at $286 million, as loads declined 3.7% and revenue per load was down 4.4%. The company’s gross profit margin improved 30 basis points in the period to 15.4%.

First-quarter 2020 EPS of $1.04 was lower than the consensus estimate of $1.10 and well off the year-ago report of $1.58. The quarter included $25 million in insurance and claims expenses, up roughly $10 million year-over-year. Management stated that the fatal accident during January was included in this quarter’s results. Landstar has $8.5 million of loss exposure or $0.16 per share per event.

Excluding the accident, management said that first-quarter EPS would have been at the high-end of its prior guidance range of $1.10 to $1.20.

Landstar is paying bonuses as incentive for those working during the pandemic. The company will pay $50 to each agent dispatching a load and each BCO delivering a load during the month of April. The company expects to incur $6 million to $7 million in incremental expenses in April as it believes its BCOs will deliver 60,000 to 70,000 loads during the month.

Management said that these payments could extend into or through May depending on how long it takes for volumes to improve.

Shares of LSTR are up 3% in midday trading.

Jo

Not certain what is going on in the trucking industry this week. Three times my husband was signed onto a load, and twice they cancelled the loads the day before it shipped and once he was already fueled and miles down the freeway to pickup before they cancelled KNOWING he was on the way to pickup. This has prevented him from signing onto a load that pays. To top it off even though they are holding him to contact they do not have to pay him any money for the time he is under contract waiting to pickup or expenses incurred as a result of the cancellations. These people should know not to contract the truck if they do not need it, and if they do it anyway should have to pay the driver for the time he was under contract!

Champ

Landstar is becoming or should I say one of the worst truck brokers in the U.S the rates they are giving in these time should be illegal and against the law I run for Landstar or should I say I used to run loads for them the Country is being lied to saying truckers are being paid and being treated like they or first responders all the brokers are getting rich on the on the backs of the small trucking company they have run the little trucking business out of business and the banks have not gave one red penny to the people that make this country what it is (FACTS)