While a host of unfavorable freight data points appeared by the end of the first quarter, with trend lines declining further to start the second quarter, many executives at the nation’s largest trucking companies are presenting a much rosier outlook than the data suggests. During the first-quarter earnings season, management teams from publicly traded carriers acknowledged softness in the spot truckload market but said the loosening in capacity won’t likely hurt them.

The growing consensus in the industry is that the little guy is likely in store for pain if spot TL fundamentals have reset lower for the near term. On the other side, well-capitalized, large operators with the majority of their business tied to annual contracts will see a much more manageable environment if the market moderates further.

Just delayed seasonality?

Some industry participants have subscribed to the theory that the recent downturn is just “delayed seasonality” following a prolonged stretch of outperformance, and freight will flow heavily again once China’s lockdowns are lifted.

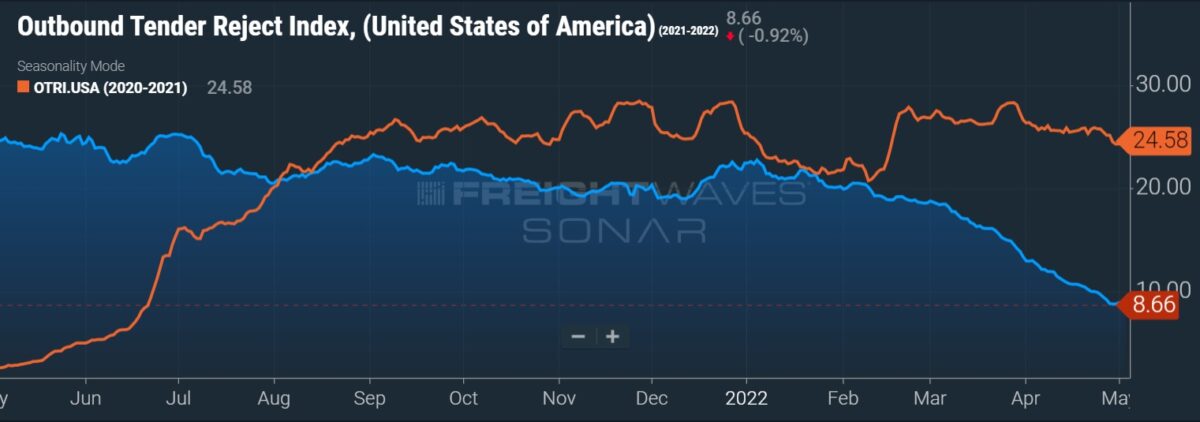

The new year picked up where 2021 left off with capacity remaining tight and rates continuing to soar. The trend bucked normal seasonality, wherein January and February traditionally see a slowdown in freight demand following the holidays.

March is normally when shipments step materially higher sequentially as consumers exit hibernation, spring merchandise begins to fly off the shelves and produce season nears. March too, didn’t follow normal seasonal trends this year, as demand cooled with each passing day. As industry data points turned sharply lower, investors became spooked and trucking stocks were down by as much as 20% to 40% year-to-date by mid-April.

“I think what is undeniable is that the data is pretty weak and continues to weaken,” Morgan Stanley (NYSE: MS) analyst Ravi Shanker told FreightWaves. He said that it isn’t just trucking data that is soft, some of the firm’s other equity research teams are seeing signs of a downturn as well.

“We know that demand has driven the bulk of the downturn so far and it feels like that is going to get tougher.”

In December, Shanker downgraded his outlook for the freight transportation industry to “cautious” from “in line,” citing the stocks were trading on inflated earnings estimates and valuation multiples after a pronounced bull run. He also flagged a potential “over-inventory” situation as demand was cooling and shippers had ordered merchandise at record levels throughout 2021. His call at the time was that the current trucking cycle would likely end in mid-2022.

While Shanker sees three plausible theories in play now — delayed seasonality, an “air pocket” caused by China lockdowns and the Russian invasion, or the cycle just tapped out one quarter ahead of schedule — it is clear that the industry has hit an inflection point.

“We are still fairly confident that there is going to be a downcycle in the back half of the year. I don’t think it is going to be a massive downcycle,” Shanker said. He expects rates to trough above where they peaked in the last cycle with spot rates seeing the bulk of the reset, not contract rates. Also, the firm’s proprietary TL freight index, which prompted his December downgrade earlier than similar actions from other analysts, has already started to level. Early indications are that the next reading from the dataset is likely to be up slightly.

“In the next four weeks we will know which theory is correct,” Shanker said.

Management commentary positive in Q1, guidance steps higher for some

Commentary from trucking heads thus far in earnings season suggests business as usual at least in the near term. The bifurcation between what’s happening in the spot market versus comments from large carriers about the contract market give the appearance the two aren’t even engaged in the same business.

What has not been surprising is the number of record quarterly performances reported by carriers in the first quarter. The public TLs saw robust freight demand and rates from 2021 spill over into the first three months of the year. For some, revenue and earnings per share were not just first-quarter records but all-time records, a big deal for what is traditionally the seasonally weakest quarter of the year.

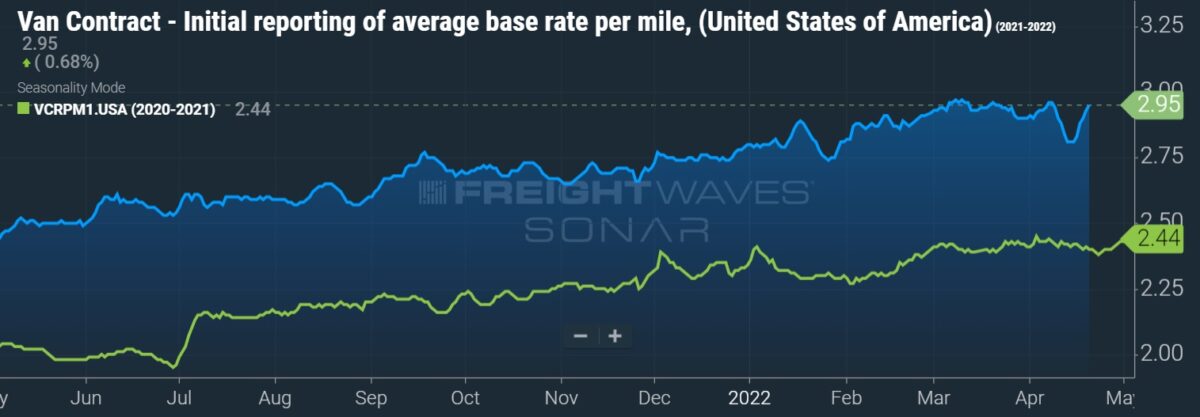

Contract rates were well into the double digits last year and early in the 2022 bid season, there has been no letup.

Knight-Swift Transportation’s (NYSE: KNX) formal 2022 guidance calls for TL contract rates to increase by double digits with spot rates continuing to moderate. The company raised full-year EPS guidance to reflect its outperformance in the first quarter. The financial implication is that the outlook for the remainder of the year was unchanged from the initial guide in January.

“As we sit here today, demand for our services, and in particular the asset side of our business, is the strongest I’ve seen in my 27-year career at the company,” J.B. Hunt (NASDAQ: JBHT) Chief Commercial Officer Shelley Simpson stated on a conference call with analysts. The company is hallway through bid season, which Simpson referred to as “the best bid season that I have seen.”

Schneider (NYSE: SNDR) too raised guidance, by 7% at the midpoint of the range, pointing to strength in the contractual market. The company worked through nearly 40% of 2022’s contract renewals in the first quarter and the outcomes were good.

“We are seeing share gain and very healthy improvement in price with recognition towards the inflationary cost around the driver [and] around equipment,” Mark Rourke, CEO and president, stated on a call. “We think the market is still very responsive to that.”

However, to balance the argument, some of the language from management teams has to be taken with the understanding that many companies still have to reprice 60% to 75% of their contractual revenue books and don’t want to show any weakness heading into negotiations.

“Most companies still think that they’re going to have a decent back half,” Shanker said. “I think that’s because they have to.”

The step lower in spot market fundamentals has resulted in many analysts reeling in estimates.

Earnings floor has been raised, higher rates part of the reason

“We do think that the [earnings] floor has been raised,” Shanker said. “I think that’s largely because the cycle floor has been raised.” His assessment comes from the expectation that inflationary pressures will keep spot rates from falling below prior cycle peaks.

It simply costs much more to run a truck now than it did in prior cycles. Lower utilization due to the ELD mandate, along with a notable step up in cost inflation on every expense line, has structurally altered the cost profile. It was the hardening of insurance markets that pushed fleets to fail during the last downturn. Since then, the industry has seen additional capacity move to the sidelines as Drug and Alcohol Clearinghouse compliance has increased.

“All of these supply constraints they’re structural, they’re never going away,” Shanker said. “In fact, Clearinghouse and insurance repeat and reset on Jan. 1 of every year. They’re going to end up taking capacity out of the industry every single year in perpetuity.”

While inflationary headwinds are expected to prop up rates, small carriers will still have a tough time adjusting to their higher cost structures, which include elevated expenses like labor, fuel, insurance, parts, equipment, etc. Also, many of the recently minted entrepreneurs obtained their authority at the peak of the market and also bought their trucks at the peak of the market. The reality of a downturn will be tough to overcome for a group that may have modeled its new venture off of all-time high spot rates.

More diversity in the model but the cycle is largely the same

Some carriers have diversified their offering, branching out into intermodal, brokerage and other asset-light offerings. The changes have smoothed out some of the booms and busts historically seen in asset-based TL. These efforts accelerated further during the pandemic as record free cash flow generation allowed for a bigger push in M&A and other organic initiatives.

Spreading out the business has some management teams suggesting their models are now better built to weather a downturn, meaning earnings are unlikely to revert back to prior trough levels.

“I think the diversification helps reduce the cyclicality of earnings,” Shanker said. “[TL earnings] have a lot more upside in the upcycle and more downside in the downcycle. That range of cyclicality kind of narrows with every level removed you are from TL.

“At the end of the day, if you’re in this industry and you have a TL, LTL, intermodal, logistics business, it’s all the same cycle. It might be one is early cycle, one is mid cycle, one is late cycle, and the difference is a matter of quarters, not years.”

No material relief for shippers in 2022

Shanker noted in a report last week that lower rates in the spot market wouldn’t provide any material rate relief to retail shippers this year as the bulk of their freight is tied to contracts. Contractual rates lag changes in spot rates by several months in most cycles, meaning it’s likely 2023 before most shippers see relief.

However, shippers could see some relief on all-in freight costs. Freight costs surged in the second half of 2021 as record consumer demand had many supply chain managers scrambling to pace inventories with sales. That pushed shippers to use more expensive airfreight options versus ocean. Once the merchandise landed in the U.S., they were forced to use a higher-cost spot market for capacity more than they would have liked.

The thought is total freight costs could net out lower as shippers move away from the premium options used last year. Also, any pick up in supply chain fluidity would likely lower costs as well. However, the report said if shippers were to see material cost relief in 2022, it’s likely due to consumer demand rolling over or it turns out they over ordered merchandise trying to navigate supply chain bottlenecks.

Click for more FreightWaves articles by Todd Maiden.

- Werner beats in Q1, expects spot-market carriers to fail

- Daseke’s outlook calls for flatbed rates to remain strong

- US supply chain pressures ease as transportation capacity grows