Byers: “The Transpacific is its own monster”

A tidal wave of containers is headed toward the West Coast

This year, President Donald Trump broke with thirty years of unquestioned orthodoxy on trade policy, attacking trading partners and allies, calling them to account, and erecting new barriers to cheap imports flooding American marketplaces. If Trump broke Washington’s conventional wisdom on international trade, his administration’s actions also broke long-standing trade flow patterns that shippers, carriers, and intermediaries have used to model supply and demand for years.

This year’s customary fall freight surge never really materialized. In every year since 2010, West Coast container volumes accelerated from June to August; in six of the past ten years, volumes contracted from August to September. Neither of those things happened this year. Instead, freight demand was pushed forward to avoid tariff deadlines on July 6 and September 24 of this year and January 1, 2019. This year, June’s volumes were larger than May’s as Chinese shippers moved their freight ahead of the July deadline; volumes also unexpectedly grew in September in advance of that deadline.

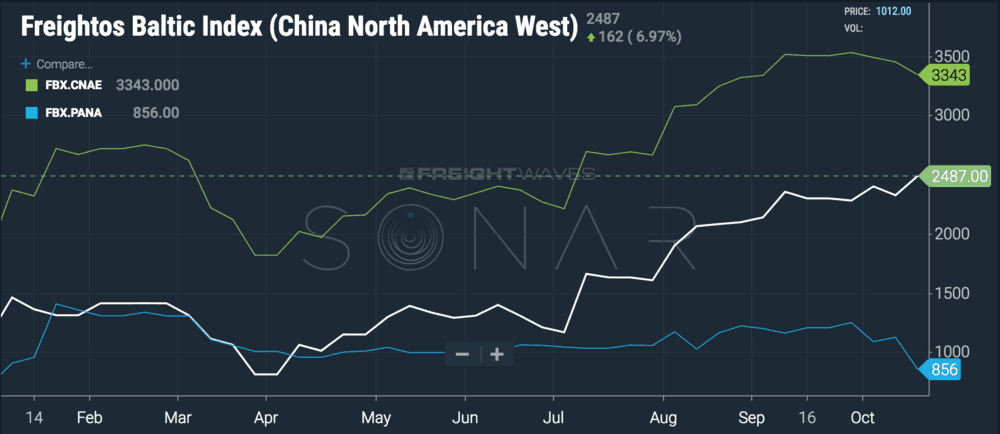

Three interlocking factors have conspired to raise spot rates for 40’ containers moving eastbound on Transpacific lanes to $2,487 this week. First, the demise of South Korean steamship line Hanjin in 2015/6 did a lot to mitigate the lane’s chronic overcapacity problems; secondly, very strong economic growth in the United States provided robust demand; finally, the chaos introduced by the tariffs allowed carriers to keep stripping capacity from their services and sell space at a premium.

FreightWaves spoke to Henry Byers, Director of Pricing and Partnerships at Steam Logistics, a Chattanooga-based international freight forwarder, about the Transpacific freight market and the outlook for Q4 and beyond. Byers started as a freight broker at Access America in 2013, continued with Coyote Logistics and UPS (NYSE: UPS) through the acquisitions, and joined Steam in 2015. At top of mind was how these market forces have affected shippers’ transportation costs.

“If a shipper has a fixed rate contract at $1,100-1,200 per FEU to the West Coast, and $2,000 per FEU to the East Coast, then right now they would be paying more than double their fixed rate to find fixed space,” Byers said.

“We were expecting, going into peak season, that it’s the usual two to two and a half month deal where you’re battling for space with companies trying to get their products in,” Byers said. “It flipped on its head from what we would have expected historically. But getting toward the tail end of normal peak season, there was another announcement of the January 1 increase from 10% to 25% which people didn’t expect it. There was a lag where people tried to explore their options, hoping it would go away, that they could lobby to change it, but now everyone’s biting the bullet and trying to get as much as they possibly can in. So right at the end of October when rates should have stayed the same or decreased, that extra volume has made rates go up on the 1st and 15th.”

Byers said he expects rates to continue to climb through November before settling in December and then falling off in January. Under normal conditions—although e-commerce has somewhat altered this assumption—retailers need inventory in their distribution centers by October 1 in order to bring it to market for the holiday shopping season. But the current wave of freight headed toward West Coast ports—Byers said that all of the ships were full of containers sent by shippers desperate to avoid 25% tariffs—is not being driven by consumer demand. Instead, Byers said, this freight would have been the cargo forming the pre-Chinese New Year surge in January (CNY falls on February 5 next year). Now shippers are moving it in advance of January 1 tariff deadlines.

The freight coming in now and into November will not be time-sensitive freight and will fill up warehouses as inventory. Because it’s already been pushed so far forward, the freight may represent an opportunity for railroads’ intermodal services to compete for carloads (the spread between trucking and railroad transit times and service will be less determinative).

The effect of the tariffs has been to break up a normal peak season surge centered on the late July to early September period and instead we’ve had two surges, one on the front end (June and July) and one on the back end (September and October). The traditional center of the peak season, in August, this year was a hole with the same number of West Coast TEUs as August 2015.

“I expect rates to increase another 6-8% on November 1 to around $2800/40’ to the West Coast and around $3400/40’ to the East Coast,” Byers said. “Then, on November 15, I would expect another increase between 4-6%. By that time, I believe demand will begin to taper off and rates will remain at that those levels through December 1. Then, in December you will likely begin to see the beginning of a rate decline that is likely to continue through Chinese New Year and beyond.”

We finished the conversation by talking about winners and losers in the trade war and speculating about what this would have looked like had the United States remained in the Trans-Pacific Partnership (TPP). Byers said that executives from Steam normally visit Asia twice a year, and he expects to go back next March to China, Hong Kong, Vietnam, and possibly India this year. Vietnam, Byers said, reminds him of China in the 1990s: a relatively unsophisticated workforce with a government that has not yet done all it can do to improve the ease of doing business. Still, “Vietnam is blowing up”, and could be a big winner if the US-China trade war lasts long enough to move manufacturing and redesign supply chains.