PHOTO COURTESY OF NYC & CO/WILL STEACY

Two key indicators of vessel finance – securities sales by U.S.-listed ship owners and global marine syndicated loan activity – are both flashing red. Ocean freight markets should see both short- and long-term consequences.

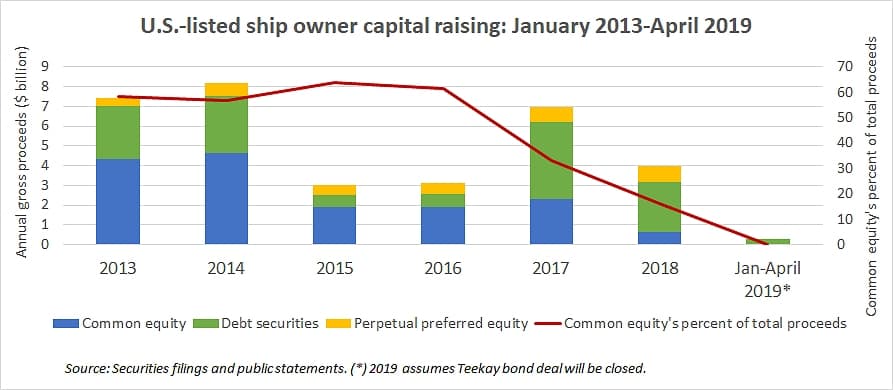

Ship owners began going public in New York in significant numbers in the early 2000s. Since the industry’s Wall Street debut, there has never been a full quarter when these companies did not raise at least some cash via offerings of equity or debt securities – until now.

On April 24, Teekay Corporation (NYSE: TK) announced plans for a private placement of $300 million in debt securities. Assuming the Teekay deal goes through, it will mark the first securities offering by a U.S.-listed ship owner (excluding time-to-time sales of shares under pre-existing equity distribution programs) since the mid-November 2018 sale of $100 million in perpetual preferred equity by GasLog Partners (NYSE: GLOP).

Wall Street drought

The absence of follow-on offerings during the first quarter of 2019 comes after a historically lean year for common-equity sales in 2018. According to data compiled by FreightWaves from securities filings and public announcements, U.S.-listed ship owners grossed only $650 million from sales of common shares in 2018, just one-seventh of the $4.6 billion in proceeds raised from common-equity offerings in 2014.

Shipping stocks have generally traded below the ‘net asset value’ (NAV) of the company, defined as the price the ships could obtain if sold in the second-hand market, plus cash and charter-contract values, minus debt and other liabilities. There’s little incentive for private founders of public shipping companies to sell shares below NAV – which is the same as selling ships at a discount – unless their hand is being forced by lenders as part of debt restructurings.

Offerings of common equity accounted for around 60 percent of all capital raises (excluding bank debt) by U.S.-listed companies during the 2013-16 period. In 2017, common equity’s share of the pie sank to one-third. Last year, it was only one-sixth. So far this year, it’s close to zero.

Given common equity’s discount to NAV, public ship owners have instead opted to raise cash through the sale of perpetual preferred equity and debt securities (secured and unsecured bonds, in both the U.S. and Norwegian markets). Perpetual preferred equity is listed separately from common shares and, like bonds, offers investors fixed income, not the highly variable – and increasingly unattractive – upside and downside afforded to common-equity holders.

The aversion to selling common shares at a discount to NAV explains another major trend – the collapse in the initial public offering (IPO) market for shipping. No ship owner has successfully priced an IPO in New York since Gener8 Maritime in June 2015, almost four years ago. Gener8 Maritime’s stock performed poorly, and the company was sold to Euronav (NYSE: EURN) in 2018.

Nonetheless, more ship owners keep coming to Wall Street. Owners such as Diamond S Shipping (NYSE: DSSI) have side-stepped the sale of discounted shares and gone public through a so-called ‘direct listing,’ whereby shares become tradeable but no money is raised, a process popularized by music-streaming giant Spotify (NYSE: SPOT).

Bank debt pullback

Shipping’s current lack of popularity on Wall Street coincides with a major pullback by its traditional source of finance – European banks. In the wake of the 2008-09 global financial crisis and subsequent European sovereign-debt crisis, multiple European lenders that had been highly active in shipping debt disappeared from the scene, including the Royal Bank of Scotland in the United Kingdom and HSH in Germany.

Today, shipping bank-debt availability is being further squeezed by the implementation of regulations under the Basel III protocol and impending implementation of Basel IV. The Basel regulations mandate risk-adjusted capital requirements for banks that make long-term lending to a volatile industry like shipping less attractive (from the perspective of the bank’s bottom line) than providing loans to other industries.

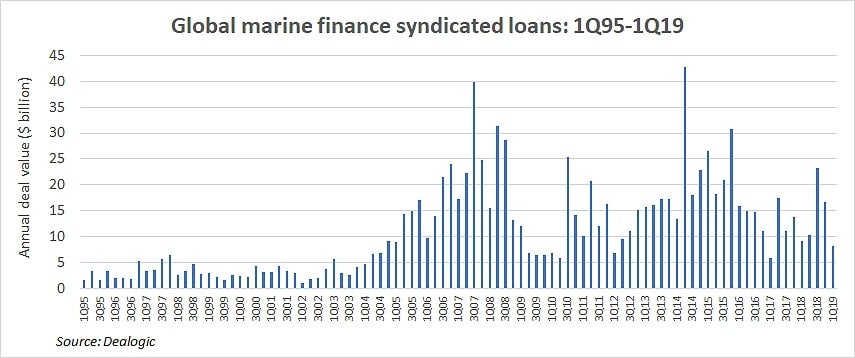

Data compiled by Dealogic, a U.K.-headquartered analytics company, confirms the extent of the decline in shipping bank debt. The latest Dealogic statistics show that only $8.25 billion was raised through marine-finance syndicated loans in the first quarter of 2019, the third-lowest quarterly tally in the past decade.

The debt pullback is not across the board, however, which is changing the competitive landscape for ocean shipping. Larger ship owners, and those with a U.S. listing, have continued to enjoy relatively open access to European commercial bank debt at low rates, in the range of LIBOR (London Interbank Offered Rate) plus 2-3 percent. Banks are competing for their business, keeping loans cheap.

In contrast, many smaller and medium-sized ship owners have reportedly been locked out of the mainstream banking market altogether, and forced to seek debt from so-called alternative-finance providers that charge steep interest rates in the high single and low double digits.

Freight implications

Ship finance is important to ocean freight markets for at least three reasons – transparency, reliability and rates.

In terms of transparency, the more listed owners there are, the more information is provided to the cargo market on prevailing rates.

There are numerous freight-rate indices available, but these are focused on specific trade lanes. The actual rates obtained by ship owners are often not reflected by the benchmark rates, as many ships do not travel those routes. Global trade patterns are becoming increasingly complex and more ‘bespoke,’ rendering quarterly rate reporting by public companies more valuable.

The shipping IPO drought has been a negative for transparency, although direct listings by companies such as Diamond S have partially countered this effect.

Ship finance is important from a cargo-transport reliability perspective because an inability to raise cash in the capital markets and/or a difficulty in refinancing maturing debt can precipitate lower maintenance spending and more ship breakdowns. In the worst-case scenario, a financing squeeze can lead to insolvency, which severely impacts cargo partners.

Finally, ship-finance availability has major consequences for ocean freight pricing. The more access to finance vessel interests have, the more new ships will be built, the more shipping capacity will be available, and the lower future rates will be for cargo shippers.

The effect on freight rates is primarily seen in the wet and dry bulk shipping sectors. Container shipping is different, as a large proportion of ordering is effectively government-sponsored. In a recent market report, brokerage Compass Maritime pointed to 34 newbuilding orders for container ships of 10,000 TEU (twenty-foot equivalent units) or larger from “government-linked owners in Asia” since the middle of last year.

Although Asian governments also support orders in the bulk sectors, capacity levels in these categories – and thus freight rates – have historically been driven more by the ordering behavior of private owners.

Limits on European bank financing and a lack of investor interest in U.S. public markets has coincided with a sharp decline in newbuilding ordering in several bulk segments. For example, contracts in the ‘workhorse’ medium-range (25,000-54,999 deadweight tons, or DWT) category of refined-product tankers is “at a historically low orderbook-to-fleet ratio of 7 percent, the lowest level since 2000,” noted Jefferies analyst Randy Giveans.

In general, as capital becomes more expensive and difficult to find, returns must inevitably improve to cover those expenses. For vessel categories exposed to escalating capital costs, capacity would eventually have to decline in relation to cargo demand and freight rates would have to rise.