‘Tis the season in ocean shipping when deal-making grinds to a halt – when ship owners pine for the Greek islands and their investment bankers plot sojourns in the French Riviera and Amalfi Coast.

Not every year pans out the same way, however. On the transaction front, ship owners and bankers might as well have been on vacation since January. The entire year has been August-esque.

On the other hand, when it comes to rates, 2019 has felt like something is happening. You certainly wouldn’t know it from investor sentiment, but there has been positive progress in the first half. Two examples are dry bulk, which is admittedly up off a low base, and liquefied petroleum gas (LPG) shipping, which is doing extremely well by any measure.

Mine reopening and trade truce bolster bulk

There have recently been two positive developments for the dry bulk sector.

First, a truce in the U.S.-China trade war was signaled at the G20 summit on June 29. This included a vague promise of Chinese purchases of U.S. soybeans, a commodity that is generally carried aboard Panamaxes, bulkers which have carrying capacities of 65,000-90,000 deadweight tons (DWT), and Supramaxes (45,000-60,000 DWT).

There was also an announcement on June 28 of an actual Chinese purchase order for 544,000 tons of U.S. soybeans, the largest order since early April.

Clarksons Platou Securities analyst Frode Mørkedal commented, “The U.S.-China ceasefire… should help support Panamax and Supramax earnings in particular, although clearly this is also good news for the whole dry bulk sector.”

The other positive news hook in dry bulk centers on Capesizes (bulkers of 100,000 DWT or more). As Evercore ISI analyst Jon Chappell put it, “Brucutu is back.” The 30 million tons per year (mtpa) Brucutu iron-ore mine in Brazil had been closed since the tragic tailings dam accident in January. Mine owner Vale (NYSE: VALE) announced on June 19 that it would reopen the mine after winning an appeals court decision.

Iron ore is shipped from Brazil to China aboard either Capesizes or larger 400,000 DWT Valemaxes. The voyage to China from Brazil is three times as long as the trip from Australia to China, meaning that losses of Brazilian exports have three times the negative effect on shipping demand as losses from Australia.

Chappell noted, “It is important to highlight that increased Brazilian exports in the second half of 2019 should boost Capesize ton-miles, which is especially important as Rio Tinto cut its full-year iron-ore production guidance mid-point by 29 million mtpa owing to operational issues in Australia.”

According to data from Clarksons Platou Securities, Capesize rates as of July 3 were $21,100 per day, up 14 percent week-on-week and up 62 percent month-on-month. Panamax rates were $12,400 per day, up 16 percent week-on-week.

All of which has done surprisingly little to sway sentiment on dry bulk, which remains weak. Allied Shipbroking research analyst Thomas Chasapis asked, “Given that realized earnings are relatively good, why is there such a poor feeling being expressed towards the market?” He added it was rare to see “this level of disconnect.”

The answer is likely to be the opposite of ‘The Boy Who Cried Wolf.’ Market participants and investors have heard this turnaround called (wrongly) too many times before.

Public companies with spot Capesize, Panamax or Supramax exposure: Eagle Bulk (NASDAQ: EGLE), Genco Shipping & Trading (NYSE: GNK), Golden Ocean (NASDAQ: GOGL), Scorpio Bulkers (NYSE: SALT), Star Bulk (NASDAQ: SBLK), Safe Bulkers (NYSE: SB), Seanergy (NASDAQ: SHIP)

LPG shipping rates maintain high levels

Rates in the LPG shipping sector feels more ‘solid’ than in dry bulk, and are hovering in the vicinity of multi-year highs.

According to data from Clarksons Platou Securities, rates as of July 3 for very large gas carriers (VLGCs, which have a carrying capacity of 84,000 cubic meters) were $63,200 per day, essentially flat week-on-week and up 28 percent month-on-month.

The LPG shipping rate outlook was a focus of a Capital Link webinar held on July 2, featuring speakers from Dorian LPG and Avance Gas.

“The market is strong and rates are staying on the high side as a result of a shortage of ships,” commented John Lycouris, chief executive officer (CEO) of Dorian LPG (USA) LLC.

He pointed to the propane arbitrage between the U.S. and Asia, which allows traders to buy U.S. propane and sell it in Asia for a profit after subtracting transport costs.

“We have a great arbitrage opportunity between the U.S. and the Far East,” said Lycouris. “Domestic U.S. demand has been slack – it has fallen, actually – and as a result, U.S. inventories have increased and the product has become cheaper and cheaper, and therefore it needs to move. Also, Middle East pricing [for LPG exports to Asia] has been higher due to events in the region and the OPEC cutbacks.”

Peder Carl Gram Simonsen, chief financial officer and interim CEO of Avance Gas, emphasized that “the share of U.S. production going to exports [versus domestic consumption] has increased significantly” and that “Japan and Korea are taking a very large share of U.S. volumes.”

When asked whether VLGC spot rates could top $100,000 per day as they did in 2014-15, Simonsen replied, “They could, but it’s a bit more balanced now [between supply and demand], so I don’t think we will see the massive rates we had back then.”

Public companies with spot VLGC exposure: Dorian LPG (NYSE: LPG), BW Gas (Oslo: GAS), Avance Gas (Oslo: AVANCE)

Container freight rates perking up

After a dip and a quick recovery in May, global container rates were fairly flat throughout June, but now they seem to perking up, at least somewhat. Is this the start of the seasonal upswing that peaks in the third quarter?

The Frieghtos Baltic Daily Index (Global), which tracks the change in pricing for 40-foot containers on a worldwide basis, has shown an uptick over the past few days. Its indices on individual trade lanes show a particular strength in recent days for China-Mediterranean freight rates.

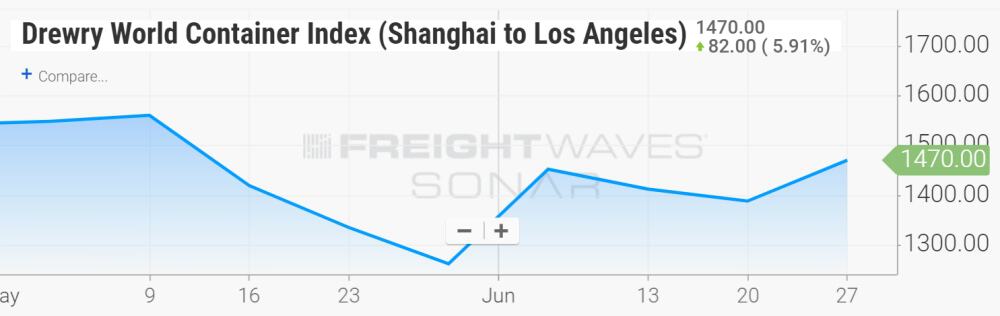

On a positive note for the moribund trans-Pacific market, the Drewry World Container Index (Shanghai to Los Angeles), which measures weekly average pricing from China to California, showed an increase in the last week of June.

According to Mørkedal at Clarksons Platou Securities, “The U.S.-China trade war truce likely means that the possible 25 percent tariff on all the remaining imports is delayed and will not affect the third quarter peak season, which should be good news for liners.”

Public shipping companies with exposure to spot box shipping rates: Maersk, Hapag-Lloyd, Matson (NYSE: MATX)

Editor’s note: Freightos has a business agreement with FreightWaves that includes editorial coverage.