Container shipping rises first and highest, then dry bulk, then product tankers, then crude tankers. That’s the emerging consensus on how a post-COVID global recovery will play out in ocean shipping. Phase one — containers — is now in epic full swing. Phase two — dry bulk — is ramping up fast.

Dry bulk is “off to the races,” maintained Cleaves Securities analyst Joakim Hannisdahl in his new quarterly outlook. Stifel analyst Ben Nolan foresees a possible “dry bulk Shangri-La.” As Braemar ACM Shipbroking lead dry cargo analyst Nick Ristic put it: “The bulls are back in town.”

Dry bulk investors have heard this story before — and been repeatedly disappointed. But so far this year, rate and stock momentum has kept building while vessel-supply growth has remained firmly in check.

Rates at multi-year highs

Dry bulk freight rates are not just an indicator for dry bulk shipping. High spot rates imply growing demand for commodities, industrial production, steel and construction — they’re a positive signal on global economic health.

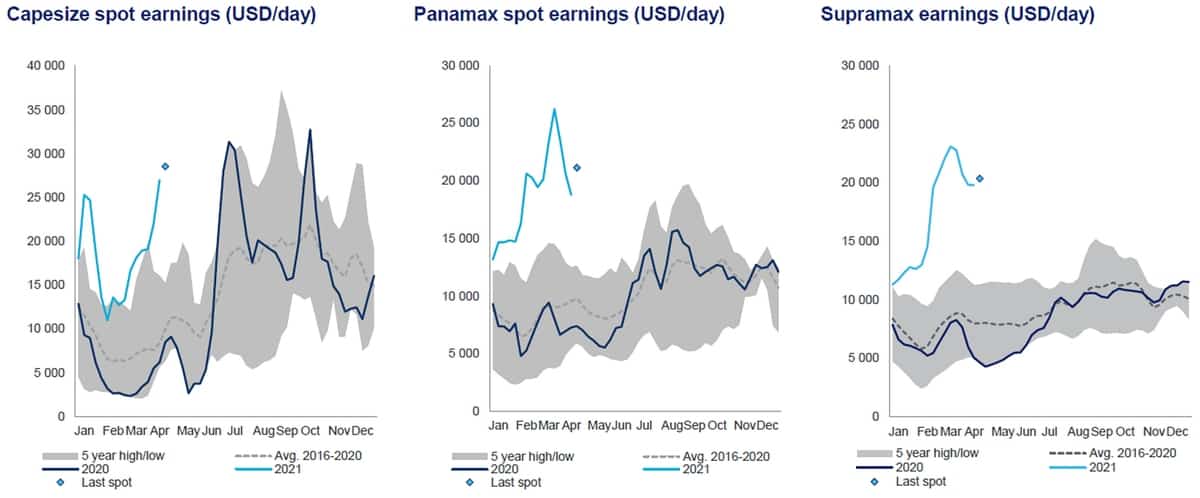

Clarksons Platou Securities reported Monday that spot rates for Capesizes (larger bulkers with capacity of around 180,000 deadweight tons or DWT) averaged $28,800 per day, up 11% week on week and 48% month on month. Today’s rates are nearly triple the 2016-20 average for this time of year.

Rates for Panamaxes (65,000-90,000 DWT) and Supramaxes (45,000-60,000 DWT) are off their February highs, but still very strong. Clarksons puts Panamax rates at $21,100 per day and Supramax rates at $20,300 per day.

In both cases, these are more than double the five-year average.

Trading levels of forward freight agreement (FFA) derivatives imply continued strength. Capesize contracts for May closed Monday at $32,007 per day, with Q3 contracts at $26,843 per day and Q4 contracts at $23,504 per day. Panamax and Supramax FFAs closed up across the board on Monday.

Dry bulk stocks rally

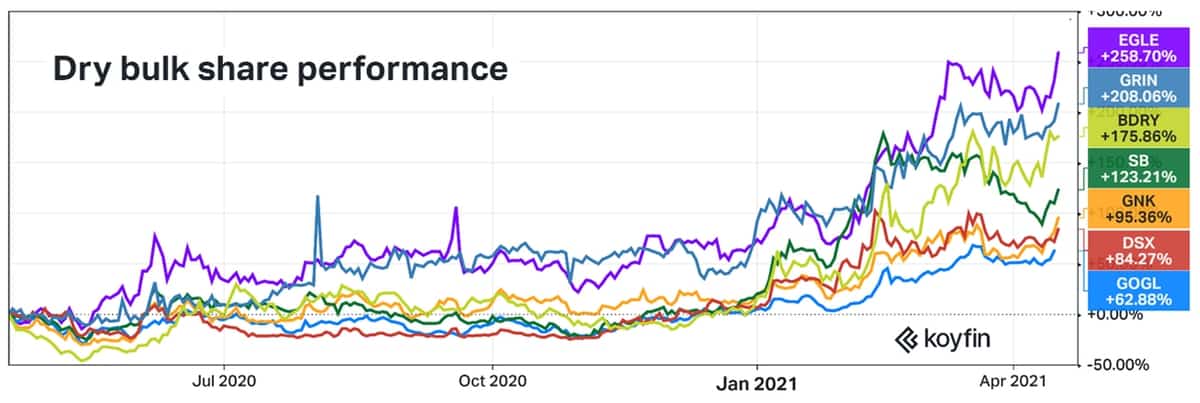

Not surprisingly, interest in dry bulk stocks is intensifying. According to Hannisdahl, “An unusually high earnings environment and a sudden influx of capital into dry bulk shipping equities have propelled our dry bulk share index to multi-year highs.”

On Monday, a down day for the overall stock market, shares of Eagle Bulk (NASDAQ: EGLE) jumped 9.7%. Diana Shipping (NYSE: DSX) rose 7.5%, Genco Shipping & Trading (NYSE: GNK) 7.4%, Star Bulk (NASDAQ: SBLK) and Safe Bulkers (NYSE: SB) 6.4%, and Golden Ocean (NASDAQ: GOGL) 6.1%.

Over the past year, Eagle Bulk has been the best performer, up 259%, followed by Grindrod Holdings (NASDAQ: GRIN), up 208%, and the Breakwave Dry Bulk Shipping ETF (NYSE: BDRY), up 176%.

Most of these gains have occurred in 2021. But even though recent price increases have been steep, dry bulk equities, in general, are still trading far below where they were in 2014 and before.

Supply side looks even better

Will new ship orders kill the rebound yet again, as it has in past cycles? According to Hannisdahl, “‘Super-cycle’ is a strong impression, but the probability is increasing each day at the current ordering trend.”

He estimated that dry bulk tonnage on order represented just 5.6% of on-the-water tonnage. “This is the lowest on our records going back to 1996 and compares with the 24.2% historical average [the mean; the median average is 15.7%].”

To put that in perspective, the container-ship orderbook-to-fleet ratio is triple the dry bulk ratio. As of April 1, the container-ship orderbook totaled 16.7% of the operating fleet, according to Alphaliner.

Cleaves estimates that the ratio for oil tankers is 8.6%, liquefied petroleum gas (LPG) carriers 17.2% and liquefied natural gas (LNG) carriers 23.2%.

Rates-to-orders correlation breaks down

According to Nolan, the relationship between dry bulk rates and newbuilding orders has broken down. The monthly correlation over the past 25 years is 0.76. Over the past six months, it’s -0.3. He said that rates are up 88% over the past six months, but monthly spending on newbuildings “is down 31% relative to the 2020 average of $515 million per month, which was already half the average for the previous 10 years.”

He sees several reasons for the disconnect. The first came up during a virtual meeting between Stifel and the management of Star Bulk on Friday. The Star Bulk management team maintained that uncertainty over which propulsion system will meet future decarbonization regulations is a much bigger hurdle for dry bulk than for other sectors.

Star Bulk management said that the “propulsion system is a far larger component of the absolute cost of the [dry bulk] ship versus containers, tankers and gas ships,” recounted Nolan.

Furthermore, “as opposed to container and tanker owners, long-term contracts are not as readily available on dry bulk ships to support the technology risk [of new propulsion systems].”

Another reason for dry bulk’s rates-ordering disconnect: Bulker owners now face an “expensive entry point” for orders due to both recent steel price inflation and orders from other shipping segments. “The sharp increase in ordering of container ships and, to a lesser extent, tankers have led to tighter shipyard capacity and pricing power for the shipyards,” said Nolan.

Capesize demand drivers

Of course, a low orderbook-to-fleet ratio doesn’t equate to sustainable strong rates without sustainably strong demand.

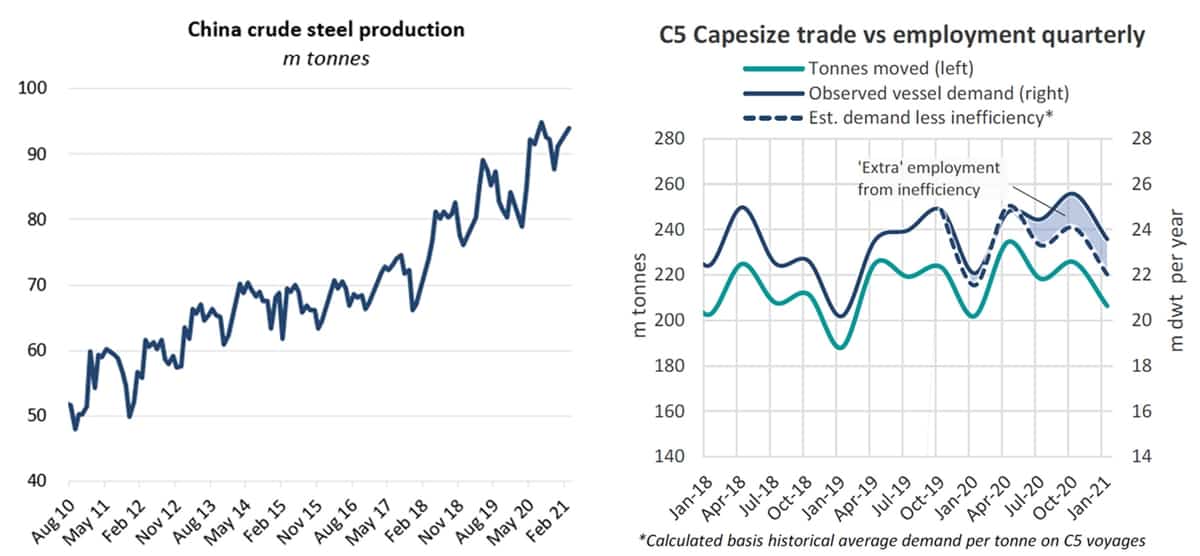

The main cargoes of Capesize bulkers are iron ore and coal, the components for steel production — and the main driver of steel production is China. According to Braemar ACM, Chinese steel production was up 19% year on year in March and up 15% year on year in the first quarter overall.

Another Capesize rate driver is fleet inefficiency: time spent waiting to unload and extra time spent ballasting due to COVID rules in Australia. That country requires a ship to be at sea for 14 days before calling at an its ports, which has had a major effect on the all-important C5 Australia-China Capesize route, according to Ristic at Braemar ACM.

Marine Strategies International (MSI) reported demand improvements for Capesizes carrying Brazilian iron ore, as well. It said that ship-movement data shows Brazilian export loads up 20% in March versus February, with “high iron-ore loading delays in Brazil.”

Sub-Capesize demand drivers

MSI also highlighted Brazil as a top driver in the Panamax sector, in this case, with its soybean exports. “Not only have exports volumes been very strong recently but port congestion in Brazil has risen to four times higher than the five-year average,” it reported.

Meanwhile, rates in smaller bulker size segments are being driven by so-called “minor bulks” such as steel products and cement.

“Indicating emerging pockets of a post-COVID demand recovery, demand for steel products has been improving in many countries across the world, notably in the U.S. and Europe,” said MSI. “This has shifted the pattern of trade in a relatively short period of time.” Chinese steel exports jumped to 7.5 million tons in March, a four-year high and 40% above January and February.

Click for more articles by Greg Miller