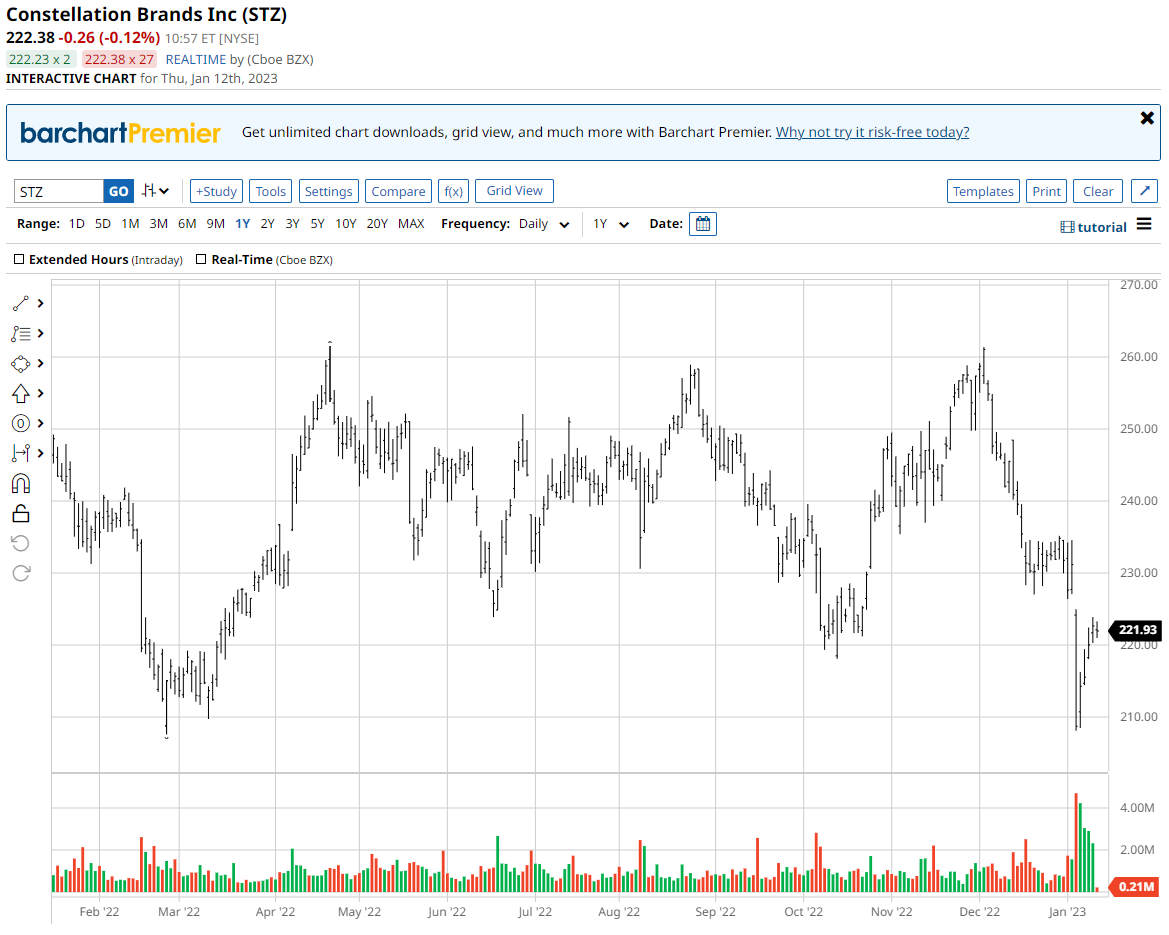

Deceleration in Constellation Brands’ shipment growth and disappointing margin outlook

Constellation Brands, the owner of the Corona and Modelo beer brands and various wine and spirits brands, such as Svedka Vodka, was among the first CPG companies to report earnings in the new year and it proved to be a controversial quarter. Shares declined 10% after it reported last Thursday, which was the biggest one-day decline since March 2020.

It appears that inflation cut into the company’s beer sales, which occupy a premium position relative to most other mass produced brands. Specifically, the company’s volume of cases sold to distributors increased 5.7%, which was a slowing from 8%-9% growth the previous four quarters. In addition, management expects its margins to remain below its targeted levels. The company is now targeting operating income growth this year of 4%-5%, not expected to keep up with its anticipated 8%-9% net revenue growth. Of course, there is still a lot to like in those numbers, considering that the company continues taking share in the overall beer market, is expanding its consumption demographics, and is still growing both its sales and operating income.

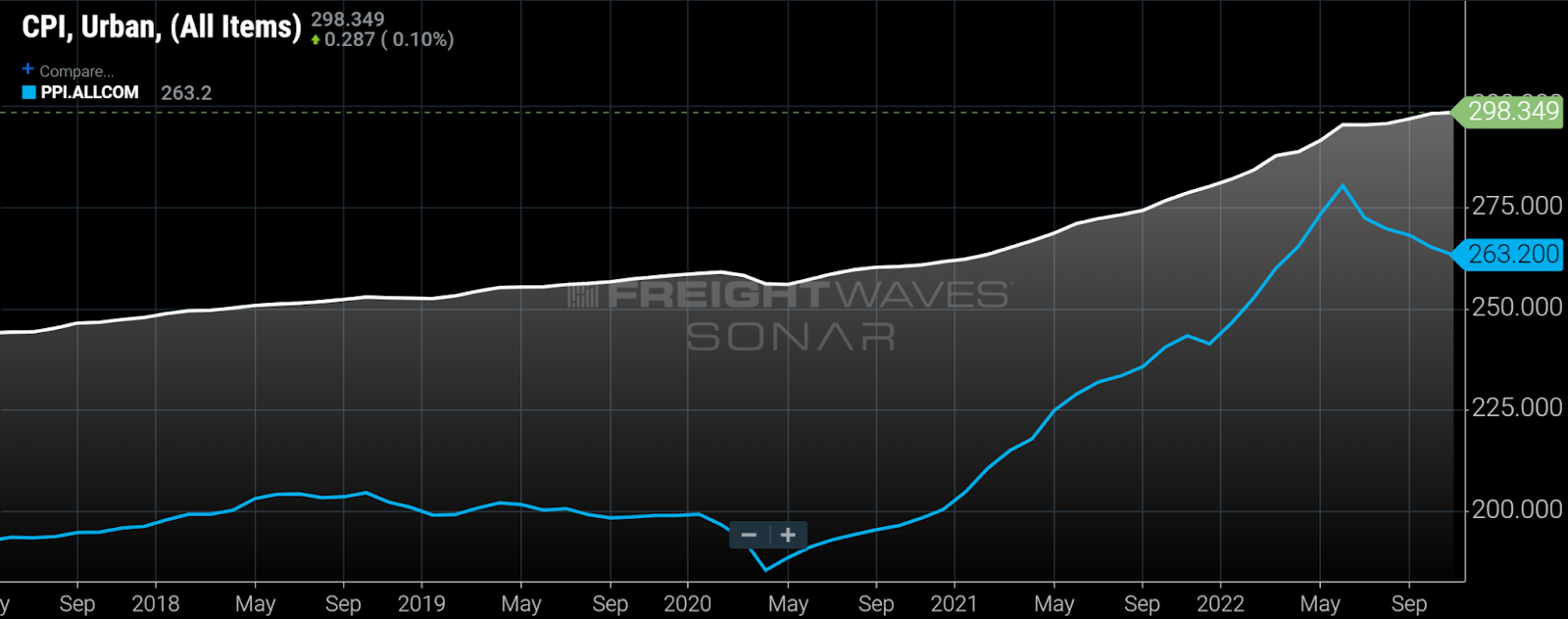

In terms of overall costs, management expects cost pressures to be less severe this year than last — single-digit growth in costs is expected this year rather than last year’s double-digit growth. That deceleration in costs is something that I expect for most CPGs with commodity prices well off their highs as well as looseness in the freight markets. Nevertheless, Constellation’s management cited several sources of continued cost pressure including raw materials, packaging (some commodities like aluminum and glass are down from their highs, but remain above pre-pandemic levels), and logistics. The company is also seeing higher costs in discretionary categories related to brewery expansions and marketing, which are likely in the company’s best interest longer-term.

Management’s comments on pricing suggest that consumers have become more sensitive to rising costs. The company typically raises prices in an effort to match rising operating costs, but has at times, and recently, backed off its initial price increases to some degree if it sees elasticities rise above targeted levels (i.e., if volume falls significantly in response to higher prices). While the company maintains that consumers are still trading up to higher-end brands, it appears that consumers have become more price-sensitive and, as a result, pricing this year is only expected to rise 1%-2%.

Will premium CPG brands disappoint this year?

Constellation Brands’ results were counter to recent trends across the CPG industry. Throughout the pandemic, companies that addressed the premium segments within their categories did the best. At first during the pandemic, the share shift toward premium brands reflected an increase in consumers’ disposable income as well as greater on-shelf availability. More recently, the sales of premium CPG brands have held up well simply because buyers of premium brands have less need to adjust their lifestyles in response to the economy-wide inflation.

Numerous CPG companies have rebalanced their product portfolios to take advantage of the greater resiliency of premium brands. Nestle, the largest packaged food company, is perhaps the best example, in light of its shift to premium products that often include health-related products, while divesting less differentiated segments. Contrary to what we have seen the past two years, this could be the year that relatively well-off consumers decide not to buy unnecessary items.

Another issue that Constellation’s results call into question is whether CPG companies will see meaningful margin improvement this year. For most CPGs, costs rose faster than pricing the past two years leading to significant margin erosion. At this time last year, most expected 2022 was supposed to be a year of margin improvement following the margin contraction that took place in 2021 — that was before the war in Ukraine and the associated surge in commodity prices upended that outlook. Here we are again at the beginning of a year with the potential for this to be a year characterized by margin recovery, but Constellation’s results demonstrate that company-specific items can get in the way of margin improvement, such as Constellation’s hedges in its beer business that have yet to expire.

To subscribe to The Stockout, FreightWaves’ CPG supply chain newsletter, click here.

For more information on SONAR or to request a demo, click here.