Plant-based meat alternatives are to the food industry what electric vehicles are to the transportation industry — a niche with a lot of startups today but maybe not so niche in the future, especially as further quality advancements are made. In today’s edition of The Stockout, a CPG-focused newsletter, I discuss recent developments with Beyond Meat. I also share my thoughts about how the various products look and taste. Beyond Meat shares are sure polarizing, but regardless of your thoughts on investing, the growth of plant-based protein is clearly a mega-trend to watch closely, with implications for animal-based protein providers, manufacturers, retailers, agriculture companies and other ingredient suppliers.

The rapid growth in plant-based proteins should not be ignored.

In 2020, Beyond Meat posted revenue growth at retail locations of 104% y/y and 136% y/y in the U.S. and worldwide, respectively, with similar growth rates posted for the just-released fourth quarter. And those growth rates include share loss to Impossible Foods in the grocery channel; we have less information about Impossible because it’s privately held. Of course, food sales at retail locations increased meaningfully across the board last year, and the company’s retail revenue growth was partially offset by a decline in revenue in out-of-home foodservice locations (which declined 13.7% and 45.1% in 2020 in the U.S. and worldwide, respectively).

Even with those thoughts in mind, it is still striking how quickly plant-based protein is growing in the context of the normally slow-growth food industry. For comparison, most of the largest food companies posted 2020 revenue growth of ~7% in their U.S. grocery channels last year, with declines of ~30%+ in outside-the-home channels. Even for the large, diversified food companies, plant-based products are often among the fastest-growing segments. Last year, Nestle’s plant-based revenue grew double digits organically; it was the company’s fastest-growing segment outside of pet food. Future sources of growth include not only greater consumer product awareness and adoption, but also future product launches. Beyond Meat’s R&D last year was the equivalent of 7.8% of net revenue — very high for food companies, which normally have R&D expenditures in the low single digits, as a percent of net revenue.

For what it’s worth, I think Impossible looks and tastes more like ground beef than the others.

In fact, I did a blind taste test with the three faux-meat burgers below and with a lean beef burger from Costco serving as a control. Impossible was the only one that fooled me — I thought it was real beef and I now understand Impossible’s market share gain. Beyond Meat did taste quite a bit better than the Open Nature plant-based patties, but it still tastes like a garden burger to me. The prices I paid were commensurate with how I thought the products tasted; a two-pack of Impossible, Beyond and Open Nature costs $7, $6.50 and $5.50, respectively. The Impossible price was discounted from its original price, presumably to reflect the 20% cut to its grocery store prices. I recommend paying the extra 50 cents for Impossible. My family said they would pay an extra 50 cents for the Impossible burgers over Beyond Meat (which we still thought tasted good), but not an extra $1.50, so Impossible may have the right idea with its price cut.

The caveat is that these are still early days and none of these companies are standing still. Consumer preferences could easily change as Beyond Meat rolls out version 3.0 of its products, and I am more than willing to give Beyond Meat another shot when it does. Or, maybe the established food companies will be the ones that develop superior products.

Impossible looks and tastes more like ground beef.

Can Beyond answer with new product development?

Beyond Meat is officially McDonald’s “preferred supplier” for the McPlant patty in a newly inked three-year deal.

In addition to the McPlant patty, the companies are also collaborating on plant-based substitutes for chicken, pork and egg. Shares of Beyond Meat often jump when partnerships are announced, such as those with Walmart, Yum! Brands and Pepsi, which, combined with its high short interest of 22.5% (it had been as high as 38%), seems to make it a candidate to become a “meme stock” should the trend continue. But, shares were initially down after the McDonald’s deal was announced because it did not make Beyond the exclusive supplier (the market had been expecting this since it was already known that Beyond was the supplier for a limited test with McDonald’s in Denmark and Sweden). Shares rebounded with the explanation that McDonald’s geographic reach is so large that it does not typically have single suppliers (and only about 20% of Beyond Meat’s net revenue is from outside the U.S.). In fact, McDonald’s does not typically announce who its suppliers are, which is likely why its announcement with Beyond had not come earlier. Beyond Meat expects the financial impact of the deal in 2021 to be “fairly modest” because it will take time for the partnership to phase in. McDonald’s plans to roll out McPlant items more broadly later this year after test phases in the Scandinavian market, where nonmeat burgers are more common.

Beyond Meat also makes bigger inroads with Yum! Brands, owner of KFC, Pizza Hut and Taco Bell.

Beyond Meat also announced an update to its agreement with Yum! Brands. Under the latest agreement, Beyond Meat is making items that are exclusive to KFC, Pizza Hut and Taco Bell during the next several years.

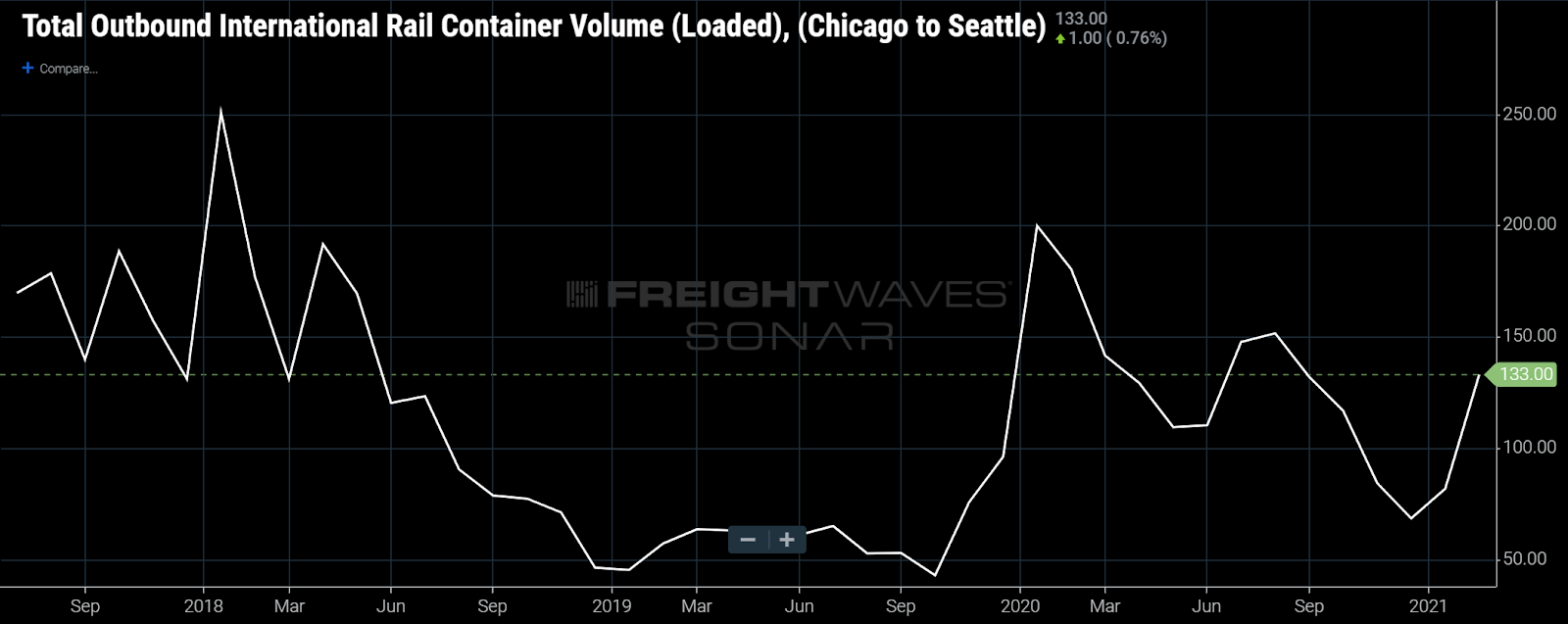

The growth in plant-based proteins will increase domestic demand for various agricultural inputs.

Unlike traditional “bean burgers,” Beyond Meat and Impossible take a different approach with inputs that include pea protein, mung bean, rice, coconut oil and cocoa butter. In addition, Impossible meat patties are made from a blend of soy and potato protein, and sunflower oil, among other ingredients. Tyson Foods is the largest traditional protein company to market its own product line of alternative protein products (after selling its 6.5% ownership position in Beyond Meat in 2019 before its IPO) under its Raised & Rooted brand, which includes chicken nuggets alternatives make from pea protein isolate, egg white, bamboo and flaxseed. So, common ingredients to many of the meat-alternative products include soy and pea protein. If imitation meat alternatives continue to take hold, it could impact soybean trade flows, which are a net export from the U.S.

Soybeans are often exported in international intermodal containers from the U.S. Midwest to the Pacific Northwest. Tariffs disrupted that trade in 2018-2019. Increased domestic consumption could impair future soybean export volumes.

Grow first, improve supply chains later.

At this stage in Beyond Meat’s life, the focus has been on getting new products to market quickly and becoming entrenched with key partners (Walmart, McDonald’s, YUM! Brands, Pepsi, etc.) in order to exploit its early-mover advantage, which has put supply chain optimization secondary. However, it’s clear that supply chain efficiency improvement is going to be one of the main methods for hitting its key objectives, including being able to underprice comparable animal products in at least one category without pressuring gross margins.

Through increased supply chain efficiencies, Beyond and Impossible could increase their reach outside only the environmentally conscious and/or health-conscious buyer who is willing to pay a premium and begin targeting cost-conscious consumers and consumers in countries with a lower standard of living. With those objectives in mind, Beyond Meat is increasing its manufacturing capacity as it rolls out new products such as Beyond Meatballs, Beyond Sausage Links and the to-be-named products that will be served in fast-food restaurants. The company recently acquired a new manufacturing facility in Pennsylvania, has a new facility in China with end-to-end capabilities, and recently enhanced its presence in the Netherlands to gain greater access to European supply chains. In addition, Beyond has avoided ingredients that are particularly high-priced due to added supply chains complexity or other reasons, such as genetic modification.

Do you agree that Impossible’s burger product is impressive? Let me know at [email protected].

If this was forwarded to you and would like to receive this newsletter, please join us here: https://web.freightwaves.com/thestockout

Happy consuming,

Mike