In a letter to rank and file members, the negotiating committee of the International Brotherhood of Teamsters informed members that YRC Worldwide (NASDAQ: YRCW) was given a grace period on health and welfare and pension fund contributions due to volume declines associated with the coronavirus.

The letter states that the grace period extended is for March contributions that were to be paid in April and that the carrier may seek an extension for “perhaps a few additional months going forward.” All of YRC’s less-than-truckload (LTL) operating companies – YRC Freight, Holland, New Penn and Reddaway – were reported to have experienced a “sharp decline in volumes over the past few weeks” due to customer closures and a weakened economy.

Importantly, the letter stated that YRC has not asked for any wage concessions from the union and plans to pay the contractual wage increase agreed upon in the labor deal that was ratified in May 2019.

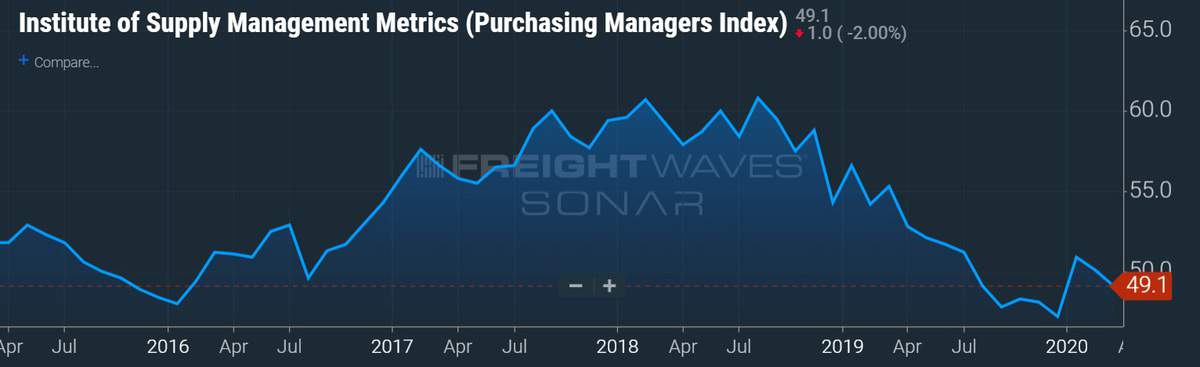

Manufactured goods account for roughly 85% of LTL industry tonnage. Like most LTL carriers, YRC has exposure to an industrial customer base that has been on the decline for a year and a half now. The PMI, a survey of manufacturing supply executives, was under the all-important 50% level in March, implying the U.S. manufacturing sector is contracting.

In March, the company issued an intra-quarter update announcing that tonnage was down 1.5% year-over-year in January, but up 0.3% in February. However, yield, or revenue per hundredweight, was off 4.2% year-over-year for the first two months of the year.

The precursor to another quarter of declining results prompted YRC activist investor, Barna Capital Group, to announce plans to replace three of YRC’s board members. The investment group said YRC’s early-2020 performance highlighted by “softer pricing while volumes fell at the same time,” was not as strong as results reported by other carriers.

In comparison, other LTL carriers have seen mixed results. ArcBest Corporation (NASDAQ: ARCB) reported that its asset-based revenue increased 1.5% year-over-year in the first quarter of 2020 through late February, but competitor Old Dominion Freight Line (NASDAQ: ODFL) reported that revenue per day declined 0.2% in January and 1% in February. Saia, Inc. (NASDAQ: SAIA) reported a 7.7% year-over-year increase in tonnage during January with only a 0.4% increase in February. However, Saia’s favorable year-over-year comparisons from an aggressive Northeast expansion campaign have ended.

The notification to the Teamsters comes two weeks after credit rating service Moody’s Investors Service downgraded the carrier’s debt, liquidity and default probability ratings, citing general market deterioration to the global economy due to the coronavirus.

Specifically related to YRC, Moody’s sees “thin margins, lack of revolver availability and limited covenant headroom” leaving the company “vulnerable.” The report went on to suggest that the carrier could struggle to realize expected cost savings from its new deal with its unionized labor force given “an already weak freight environment” and that its network optimization strategy could be at risk due to a slowdown and disruptions.

YRC recently combined its sales force from four teams to one and is migrating all of its separate operating units onto one technology platform. The company’s goal is for its customers to be able to access all five entities through one network under one point of contact. These moves, along with the previously implemented new labor deal as well as a new financial structure, are expected to lead to improved results.

In September 2019, YRC entered into a new $600 million term loan agreement providing it with additional liquidity, a lower interest rate, less restrictive financial covenants and extended the maturity date to mid-2024. The new leverage covenant requires YRC to maintain adjusted last 12 months’ (LTM) earnings before interest, taxes, depreciation and amortization (EBITDA) of $200 million, a threshold the carrier has not breached on a calendar year basis since 2011.

However, YRC was recently granted a waiver on this covenant from its lenders for the remainder of 2020.

YRC’s 2019 year-end earnings report showed it generated $210.6 million in 2019 adjusted EBITDA, only modestly higher than that required by the lending covenant. The “thin margins” referenced by Moody’s were a full-year operating ratio (OR) of 98.8% in the company’s freight division and a 100.3% result in the regional segment.

OR, operating expenses expressed as a percentage of revenue, is the inverse of operating margin.

2019 was the last year the two divisions will be reported separately.

YRC reported a net loss of $104 million, or $3.13 per share, in 2019 and ended the year with $902.8 million in debt and $80.4 million in liquidity compared to $203.8 million in liquidity at the end of 2018. YRC reported $22 million in cash flow from operations during 2019, down from $225 million in 2018 and $61 million in 2017. Cash from operations less amounts needed to fund capital expenditures (capex), or free cash flow, was $96 million to the negative. The carrier’s high debt load/interest expense and cost structure make it difficult to reduce leverage.

In 2019, YRC’s union employees accounted for 79% of the company’s 29,000 total employees.

Matt

It is an absolute joke. No pension. Soon to be no healthcare. Work the shit out of you and treat you like crap. Close the doors. Put chains on the gates and let me collect my unemployment.

terry

If it doesn’t work for you, then just go somewhere else. Why do you torture yourself?