Ocean carrier Zim outperformed its much larger rivals at the peak of the container shipping boom. It’s still raking in over a billion dollars a quarter, but as the market corrects, it’s falling back to Earth faster than others.

On Wednesday, Zim (NYSE: ZIM) announced a drop in quarterly earnings and cut its full-year guidance. Not only is its spot-rate revenue falling, but it is agreeing to lower contract rates in mid-contract and is handling less volume due to weaker demand and ongoing congestion at East Coast ports.

Zim reported net income of $1.17 billion for Q3 2022, down 20% year on year and down 13% versus the second quarter. Earnings came in at $9.66 per share, below the Bloomberg analyst consensus of $9.81.

The company lowered its full-year guidance for adjusted earnings before interest, taxes, depreciation and amortization to $7.4 billion to $7.7 billion, a 6% reduction from its previous estimate.

The new outlook implies record earnings for 2022, but fourth-quarter EBITDA down 41-57% versus the third quarter.

“Over the past several weeks we’ve seen a steeper decline in freight rates than we had previously assumed,” said Zim CEO Eli Glickman during a call with analysts on Wednesday. He pointed to “a challenging outlook for container shipping, particularly given the scheduled vessel deliveries planned for next year and 2024.”

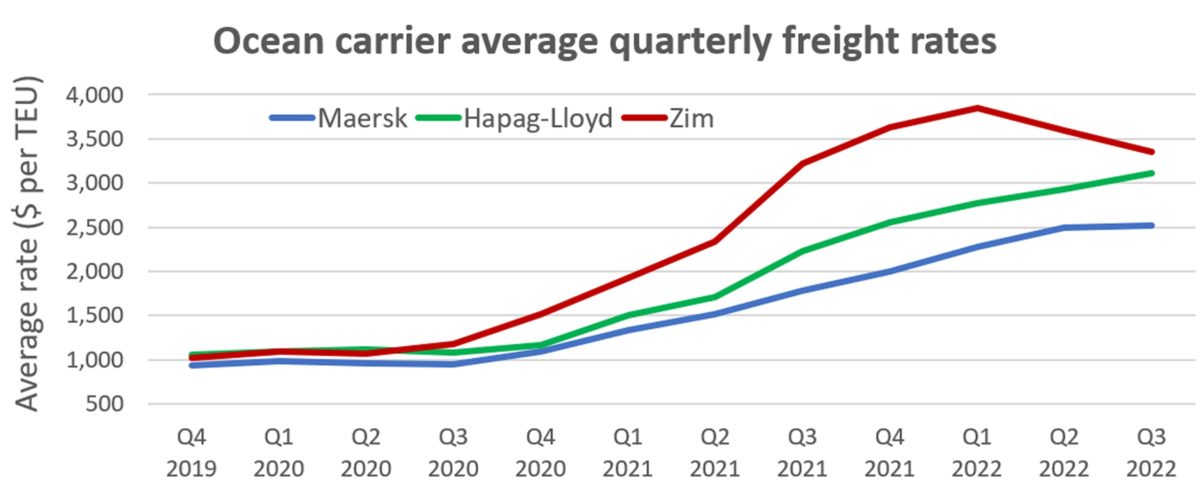

Zim’s average freight rates falling

Rates averaged $3,353 per twenty-foot equivalent unit in Q3 2022. That’s up 4% year on year but down 7% versus to the second quarter.

Zim, the world’s 10th largest ocean carrier, benefited during the boom from elevated exposure to the skyrocketing market. It had capacity concentrated in the high-earning trans-Pacific trade and heavy spot exposure. Now, that high operating leverage is pulling Zim down more so than carriers with much larger fleets such as Maersk and Hapag-Lloyd, which have broader service footprints and very strong contract coverage.

Zim’s average freight rate (including both contract and spot) still tops Maersk’s and Hapag-Lloyd’s. But Zim’s peaked earlier and the gap is narrowing. Since the first quarter, Zim’s average freight rate has fallen 13%. Over the same period, rates of Maersk and Hapag-Lloyd rose 11% and 12%, respectively. All three predict fourth-quarter rates will fall versus the third quarter.

Through the first nine months of this year, 34% of Zim’s volume was in the trans-Pacific trade. Zim CFO Xavier Destriau said spot rates in this market, particularly in the Asia-West Coast lane, have been especially hard hit.

“The trade between Asia and Los Angeles has been the most severely impacted,” he said. Asked whether spot rates are at or below breakeven, he said, “In some trades we are not far from that. [For Asia-West Coast] there is not much more room for a reduction.”

Zim renegotiating contract rates

During the conference calls of Maersk and Hapag-Lloyd, executives said higher contract rates were trumping lower spot rates, allowing average rates to continue rising through the third quarter. They also maintained that they were generally not renegotiating annual contracts.

Maersk CEO Soren Skou said, “I know there’s been a lot of talk about customer contract behavior. But the reality is that the vast majority of our contracts are holding, Our contract portfolio has performed as expected.”

According to Hapag-Lloyd CEO Rolf Habben Jansen, “If you look at Q3, we still had pretty decent contract compliance.”

Zim, in contrast, confirmed it has been renegotiating existing contract prices. It cited this as one reason why average rates are declining. Zim’s main contract exposure is on the trans-Pacific, where 50% of its volumes are under annual contracts that start each May.

Destriau explained: “With the steep decline in the spot market, spot rates went below contract rates and crossed at some point in the quarter. More importantly from our customers’ perspective, demand was not there. So, we have to live with this new reality.

“Most of our customers are not customers for one season. They’re recurring customers with whom we have a long-term relationship. We intend to continue to have those long-term relationships. As the spread between contract rates and spot rates increased, we had to sit down and agree to revisit the pricing with our [contract] customers in order to protect some of the volume. We needed to be pragmatic and make sure we found the middle ground between the interests of our customers and ourselves.”

Stock bulls vs. bears

Share performance of container shipping stocks like Zim’s is being driven by two opposing forces: downward earnings momentum on one hand and perceived low valuation on the other.

As Deutsche Bank analyst Andy Chu wrote in a research note on Hapag-Lloyd last Thursday: “There continues to be a two-way pull on container shipping at the moment, with bulls arguing cheap valuation and bears arguing negative earnings momentum in freight rates and earnings. We side with the latter — that from here it is all about momentum. We worry about the 27% of the current fleet that is on order and how this might be absorbed in a weaker demand environment.”

Trading in Zim’s stock is squarely in the bear camp: It’s down 70% from its 52-week high.

During an interview with American Shipper in October, Jefferies analyst Omar Nokta said that many value investors are looking at container stocks. “Investors don’t want to be involved right now as freight rates are still declining,” he said. “But the moment we start to see some stability in freight rates, I think buyers are going to be flocking into this sector because of the value these stocks hold.”

Zim checks the box for value investors. Not only does it remain highly profitable, it had $4.47 billion in cash at the end of the third quarter, equating to over $35 per share. The stock closed at $26.95 on Wednesday.

Nevertheless, spot rates are still falling, albeit at a slower pace in October and November than in August and September. Rates have yet to reach a floor, thus the stabilization trigger cited by Nokta has yet to fully materialize.

Zim’s new guidance assumes the rate decline isn’t over. “We expect rates to continue to go down,” said Destriau. “Eventually, we think all of the trades will find a new equilibrium,” he said, but he acknowledged that “there is a lot of uncertainty today on when rates will stabilize.”

Click for more articles by Greg Miller

Related articles:

- Los Angeles imports keep sinking as East Coast gains more ground

- Hapag-Lloyd CEO: Container market volatile but not collapsing

- After steep September slide, US imports stabilize in October

- End of an era: Profits finally peak for shipping giant Maersk

- Shifting tides: The fall of container shipping stocks, the rise of tankers

Sonasue

I’m hanging in there with ZIM because shipping rates WILL stabilize and China WILL be relaxing its

Zero Covid policy. In early spring, the shipping industry WILL start bustling again. As I’m approaching

80, I’m learning that everything goes in waves. That’s life.

Spencer

Hi Greg. Thanks for the interesting article. Investing in ZIM has been like trying to catch a falling knife. I have lost quite a few “fingers” this way. Every time I think the floor has been found, it turns out to be the ceiling of the level beneath. I would love to invest in ZIM at these levels (especially with so much cash-on-hand) but as everything seems to be pointing toward recession, with the likelihood of imports falling even further, I think I’ll wait until this falls into the $23-24 range before dipping a toe.

MyrtleLindsey

good