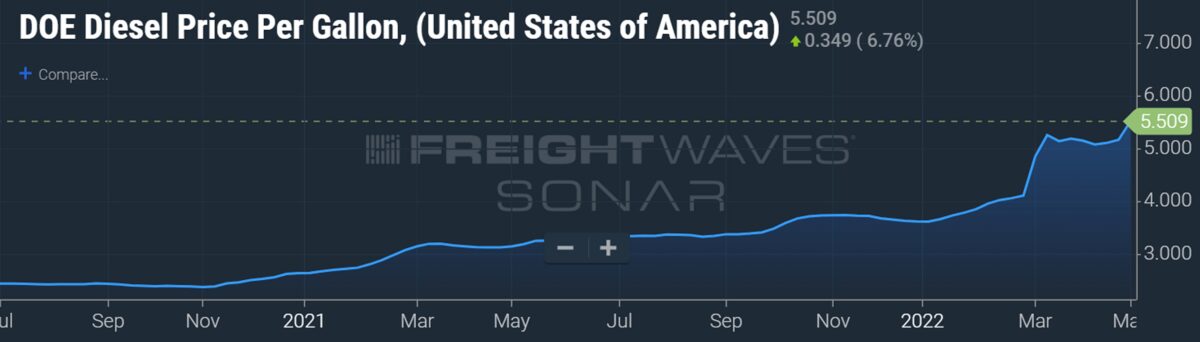

Retail gasoline prices in the U.S. are up 45% year on year. Diesel used by American truckers is up 75% and just hit an all-time high. But this is not just an American problem. Pain at the pump is global. And so-called product tankers — ships designed to transport cargoes such as diesel, gasoline and jet fuel — are in prime position to profit.

Fuel flows globally to where it earns the highest return. Case in point: As U.S. diesel prices have skyrocketed, American exports of diesel have surged, because demand in other countries is higher.

U.S distillate fuel exports hit 1.74 million barrels per day (b/d) in early April, nearing record levels, according to preliminary data from the Energy Information Administration (EIA). Total U.S. exports of all refined products in April rose 28% year on year.

‘Outright panic buying of diesel’

“There has been outright panic-buying of diesel,” said Anthony Gurnee, CEO of product-tanker owner Ardmore Shipping (NYSE: ASC), during a conference call on Wednesday.

Ardmore specializes in MR tankers, a vessel class with capacity ranging from 25,000-54,999 deadweight tons (DWT). Clarksons Platou Securities said that modern-built MRs were earning $49,800 per day in the spot market as of Friday. That’s more than quadruple the average rate for full-year 2021. Clarksons puts the breakeven rate for such vessels at $18,000 per day.

“The world is really crying out for diesel and that’s causing refinery margins to spike,” said Lois Zabrocky, CEO of International Seaways (NYSE: INSW), during a conference call on Wednesday.

INSW’s product tanker fleet primarily consists of MRs and LR1s (55,000-79,999 DWT). Modern LR1s are earning $50,400 per day in the spot market, according to Clarksons, which puts the breakeven rate for such ships at $19,000 per day. Current LR1 rates are almost quadruple their full-year 2021 average.

Larger LR2s (80,000-119,00 DWT) that handle high-volume, long-haul runs are showing even steeper gains. Rates for modern LR2s jumped 21% on Friday to $58,600 per day, said Clarksons.

War exacerbates diesel shortages

The worldwide diesel market is “extremely tight” and the Russia-Ukraine war “has exacerbated the global diesel shortage,” said James Doyle, head of corporate development at Scorpio Tankers (NYSE: STNG), during a conference call on April 28.

Before the invasion, he said, Russia exported about 1 million b/d of diesel to Europe. That volume has plummeted. “But the diesel shortage in Europe is not new,” he added. “And the shortage extends beyond Europe to Latin America and Africa, which have similar diesel deficits.

“For our MRs, the highest rate increases were for our vessels going from the U.S. Gulf to Latin America, which has less to do with Russia and Ukraine and more to do with increasing demand,” Doyle pointed out.

“We expect the market to tighten further with increased competition for distillate molecules as jet fuel demand returns. This is also having an impact on gasoline. With refineries running in max distillate mode, we are not building significant gasoline inventories ahead of peak driving season. As demand grows and inventories remain low, product tankers will need to be the conduit for filling the global supply-demand imbalance.”

Commodity specialist Argus made the same point on gasoline. “The lack of spare capacity is causing alarm heading into the peak summer driving season,” Argus warned on Thursday. “The situation is compounded by even higher middle-distillate margins, which have boosted supply of diesel over gasoline.”

Inventories drawn through COVID era

Usually, rates for tankers that carry crude oil and rates for tankers that carry petroleum products trend roughly in tandem. And if one outperforms the other, it’s usually crude. This year, product tankers are dramatically outperforming crude tankers; larger crude tankers are still below breakeven.

Both crude and product tankers saw rates collapse during the COVID era. Oil production outstripped demand amid lockdowns. The world’s inventories filled with cheap crude and products bought at the trough.

Ever since, those inventories have been drawn down instead of using tankers to import new supply (because new supply is much more expensive than the petroleum still in storage bought at the trough).

Due to this practice, stockpiles were already historically low months before Russia invaded Ukraine. In November 2021, Alphatanker published a report called “Welcome to the great diesel squeeze,” which warned: “It’s now apparent that global gasoil and diesel markets are tightening at an alarming pace with supply shortfalls now hitting key consumer markets worldwide.”

Then Russia invaded Ukraine. “This event immediately laid bare … the risks of severely depleted inventories,” said Evercore ISI analyst Jon Chappell.

Product tankers vs. crude tankers

Asked why this has boosted product tanker rates so much more than crude tanker rates — given that crude inventories are also historically low — Chappell responded, “Usually the two groups are highly correlated, and usually crude leads and outperforms by measure of magnitude. But we are far from normal times.

“Crude tankers are doing really well in regions directly impacted by Russia’s invasion of Ukraine — the Black Sea, Baltic and the Med — owing to the higher insurance costs and risks of entering those markets. But overall, the crude markets have been balancing new longer trade routes with the inability of OPEC to meet quotas, Russia [being] offline, and China lockdowns. The market is better than it probably should be based on those latter factors, but the low inventories and longer ton-miles [voyage distances] are offsetting some of the macro headwinds.

“Product tankers are benefiting from localized diesel shortages, high refinery margins … and massive trading arbs [arbitrages] that allow traders to pay much higher freight costs and still make a ton on the arb. Inventories are far too low globally and prices will likely remain elevated, forcing more trading in unusual trade lanes, tightening capacity and lifting that market well before and well above crude.

“Eventually crude tankers will catch up, I think, if supply of crude can meet higher refinery demand. But right now, it’s a unique product story. And talking with my oil analyst, it’s hard to see how these diesel shortages ease or the strong tanker markets end,” said Chappell.

Earnings recap

Among the universe of listed shipowners, Clarksons Platou Securities said that “product tankers are sailing up as the winning sector year to date.”

Rates are surging on “exploding refining margins,” said Clarksons. It maintained that “the products sector looks primed to gain further.”

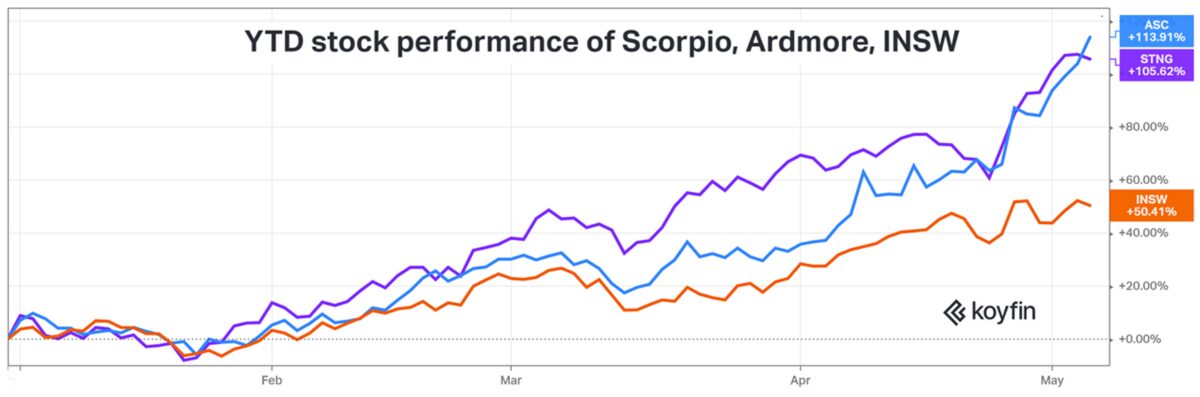

Through Thursday’s close, the stocks of Scorpio Tankers and Ardmore Shipping were up 106% and 114% year to date, respectively. Shares of International Seaways — which owns both crude and product tankers — were up 50% year to date.

Listed product tanker owners have just reported more losses for the first quarter. The rate upswing won’t be fully felt until the current quarter.

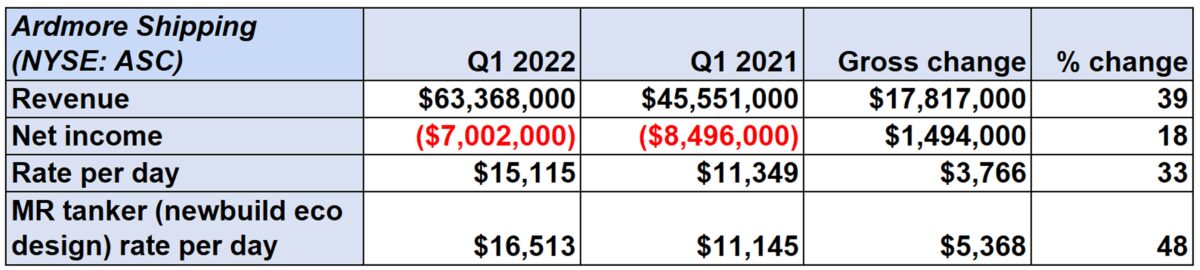

Ardmore Shipping reported a net loss of $7 million for Q1 2022 versus a net loss of $8.5 million in Q1 2021. The adjusted loss of 4 cents per share beat consensus expectations for a loss of 8 cents.

Ardmore has 50% of its Q2 2022 available MR spot days booked at $25,500 per day. That compares to rates of $16,513 per day in Q1 2022.

International Seaways reported a net loss of $13 million for Q1 2022 compared to a net loss of $13.4 million in the same period last year. The adjusted loss of 29 cents per share was slightly better than Wall Street expectations for a loss of 30 cents.

The company has 41% of its available Q2 2022 MR spot days booked at an average of $24,500 per day. That compares to $14,030 per day in the first quarter.

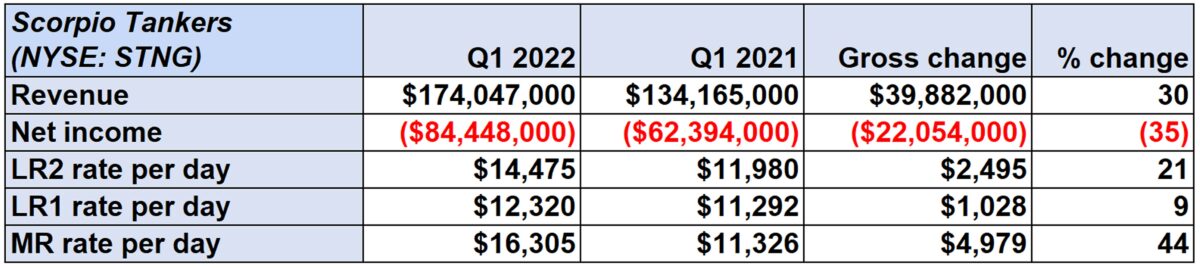

Scorpio Tankers reported a net loss of $84.4 million for Q1 2022 compared to a net loss of $62.4 million in Q1 2021. The adjusted loss per share of 27 cents came in much better than the consensus forecast for a loss of 58 cents.

Scorpio has 42% of its available Q2 2022 spot MR days booked at $30,000 per day. Its MR fleet earned an average of $16,305 per day in the first quarter.

Click for more articles by Greg Miller

Related articles:

- Benchmark diesel price hits all-time record; market signaling it isn’t done

- Why every American should care that diesel prices are surging across the country

- Why diesel prices are soaring beyond crude and gasoline, and are likely to continue that way

- How low can tankers go? Analysts slash rate forecasts (again)

- Why Russia-Ukraine war has not ignited crude tanker rates (yet)

- Shipping on Wall Street: Is it better to be a pure play or jack-of-all-trades?

- ‘Gobbling up’ cargo: How crude tankers cannibalized product tankers