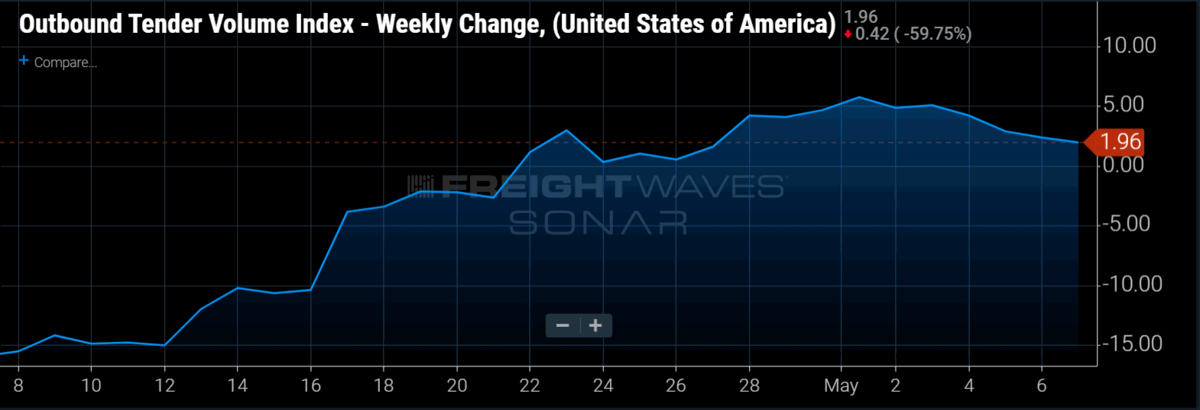

Outbound tender volumes continue to climb slowly. The rate of acceleration has decreased this week compared to last, only up 2.0% week-over-week. National volumes have now bounced nearly 10% off the bottom on April 6th and are 7% lower year-over-year.

Despite warnings from health and disease experts, the majority of U.S. states have moved forward or are moving forward with relaxing some restrictions. Unfortunately for freight volumes, most of the businesses reopening are service-based and do not move much freight. However, there was encouraging news for freight volumes out of Detroit this week when the major auto manufacturers set a soft reopening date for Monday, May 18th.

It is not that the auto industry moves a high percentage of domestic freight. But auto producers are well-positioned to create the blueprint for a wider manufacturing reopening. The strong union presence of the UAW and other unions may be able to secure cleaner and safer work environments, as well as enough protective equipment. Also, the inherent structure of auto plants makes them better suited to work through COVID-19 for a couple reasons. First, the plants are highly automated and workers use heavy machinery, which means they typically are already wearing gloves; secondly, auto plants are much less densely populated than an ecommerce fulfillment warehouse or meat processing plant. It is our belief that auto producers can lead the way towards a manufacturing and industrial reopening. The issue will then be demand, which will be damaged by the economic losses of the next few months.

It may be some time before OTVI reaches pre-crisis levels, but the re-opening of parts of the economy coupled with the ramping up of produce season will increase volumes slowly for the next couple of weeks.

On the positive side, nine of the 15 major freight markets FreightWaves tracks were positive on a week-over-week basis. This ratio is a significant improvement from recent weeks. The markets with the largest gains in OTVI.USA were Savannah, Georgia (17.02%), Houston (6.42%) and Los Angeles (6.04%). The markets with the largest declines were Seattle (-10.65%), Memphis (-9.30%) and Laredo, Texas (-8.73%).

Tender rejections show signs of life

Outbound tender rejections have increased week-over-week for the first time since the OTRI peaked at 19.25% on March 28th. While the index is only up a paltry 11 bps over the past week to 2.84%, it is positive for carriers that OTRI has found the bottom. Unfortunately for carriers, this is still one of the lowest values in the series’ three-year history.

The index has previously found a support level around 4%, getting close to it but rarely falling below. This is the longest time OTRI has been under that support line, and with volumes at national holiday levels, there is not much pointing towards a rebound.

Since peaking at 19.25% on March 28th, OTRI has plummeted more than 80%. OTRI is a measure of carriers’ willingness to accept loads at contracted rates and currently, carriers are moving whatever freight they can find. Contract rates have bounced off the bottom, but tender rejection rates will not trend up across the country until capacity is filled in most markets. Currently, this is not the case. Many trucks have been idled and capacity remains loose around the country. The reopening of some industries and the produce harvests will tighten capacity in pockets, but not on a national level.

In terms of pricing power, it is not constructive for either shippers or carriers when volumes are this low. So, to grasp where the power is in this underperforming environment, we must look to pre-crisis capacity, which was already excessive. Although we believe bankruptcies and company failures will re-accelerate during the second quarter, capacity is still very loose right now. Until volumes pick back up, or a swath of drivers leave the market, that environment will remain.

For more information on the FreightWaves Freight Intel Group, please contact Kevin Hill at khill@www.freightwaves.com, Seth Holm at sholm@www.freightwaves.com or Andrew Cox at acox@www.freightwaves.com.

Check out the newest episode of the Freight Intel Group’s podcast here.