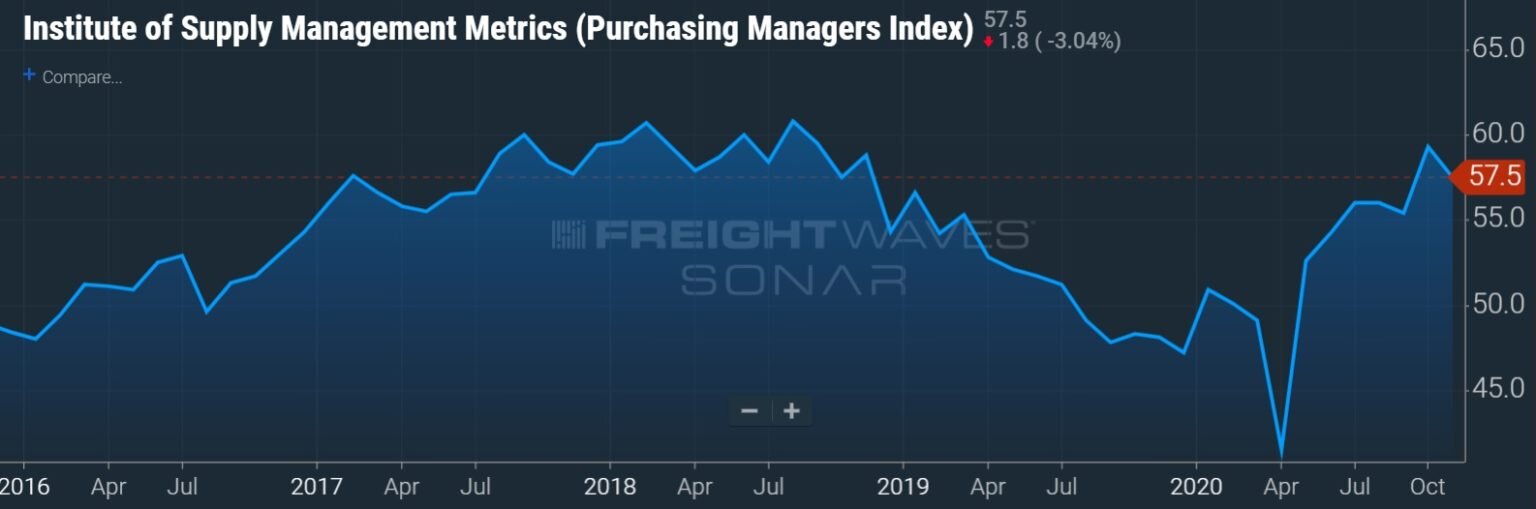

Several analysts have published transportation outlook reports for 2021 that are calling for continued strength in the trucking markets. Some are expecting the favorable truckload fundamentals that were in place in the back half of 2020 to continue unchanged though 2021. However, others believe the TL trade has grown long in the tooth and are pivoting to a more meaningful industrial recovery, which supports an improving freight environment for less-than-truckload carriers and the railroads.

Potential for an industrial uptick benefits LTL

Many analysts believe a wide distribution of a vaccine will reopen more than just the consumer economy. As this occurs, companies that delayed investment in infrastructure, buildings, equipment and technology this year over uncertainty around COVID will need to play catch-up on their capex allocations.

In his annual outlook to clients, Deutsche Bank (NYSE: DB) analyst Amit Mehrotra said his “long-held bullish stance on transportation equities continues unabated in 2021.” His optimistic expectations are based on a positive lift in the industrial economy, strong housing demand, continued inventory restocking and a release of pent-up consumer demand.

Mehrotra is “most optimistic” about the prospects of the U.S. industrial economy expanding quicker than overall GDP. Deutsche Bank’s economics team is forecasting an average year-over-year growth rate of 7.8% in industrial production in the second, third and fourth quarters of 2021, with 4.5% growth in 2022. Mehrotra believes the industrial sector could move positively as soon as the first quarter as demand for gas, diesel and jet fuel improves along with aircraft production. He’s most bullish on the rails and LTLs given their industrial exposure.

In an initiation of coverage report to clients, Evercore ISI (NYSE: EVR) analyst Jon Chappell outlined his trucking thesis, which recommends LTL carriers over TL carriers. He likes the industry’s high barriers to entry and expects service levels to improve through ongoing network optimization and efficiency initiatives. He sees ample room for market share growth in LTL as well.

“Although LTL stocks are trading at all-time-high multiples, a multitude of growth opportunities and the eventual recovery of the U.S. industrial economy provides a much longer cyclical runway for this segment, with a likely multiyear period of double-digit earnings growth,” Chappell said.

TL fundamentals to carry the year again?

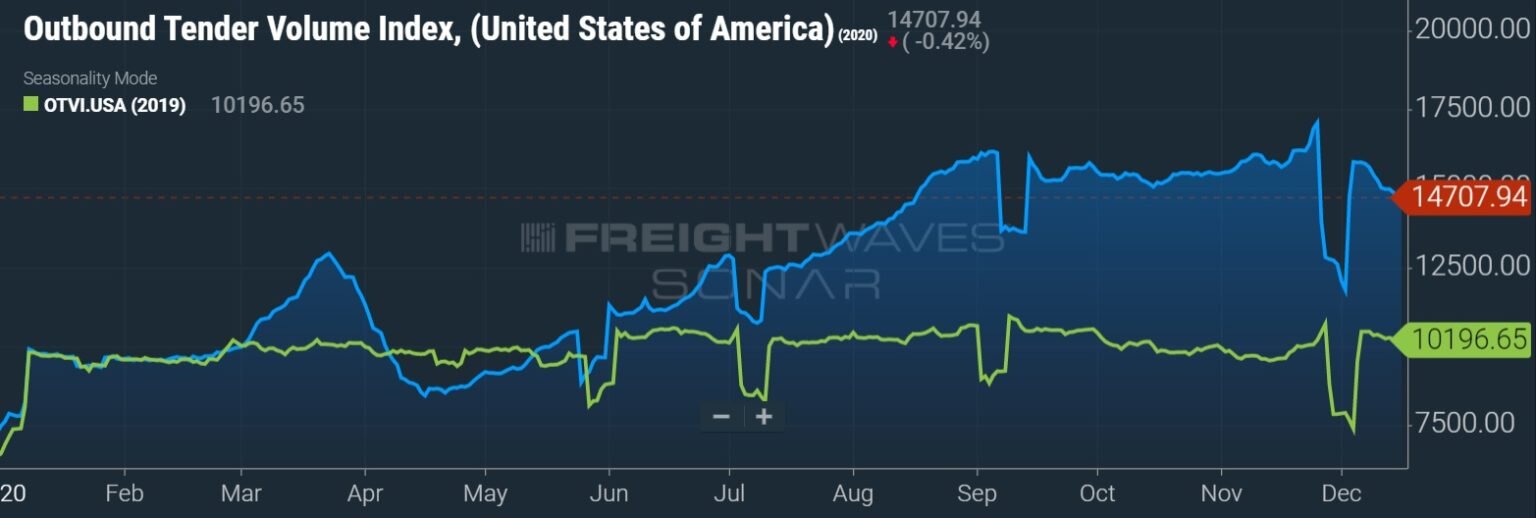

TL carriers dominated the headlines for much of 2020 as those with high exposure to consumer durables, food and grocery, and home improvement goods benefited tremendously from consumers heavily buying online during lockdowns.

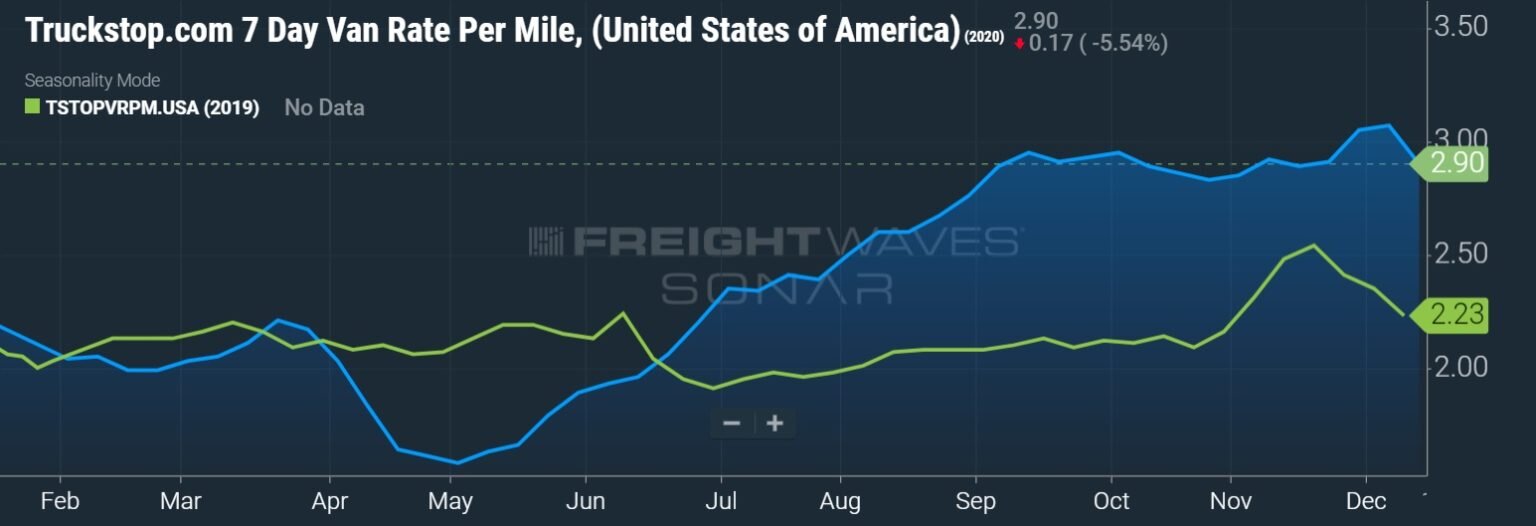

Some analysts think the hole punched in inventories can be cured in the first few months of 2021 and that new truck capacity coming online will dampen current TL fundamentals that have propelled rates to new highs. Other analysts aren’t ready to pull the plug on the TL trade and believe a new peak could be achieved or at least the current peak can linger.

Morgan Stanley’s Ravi Shanker (NYSE: MS) favors the TLs over the LTLs, in part due to low TL valuation multiples, although both sectors are his top picks for 2021.

“We believe it is far too early to call an end to the TL cycle as the demand rebound is still ahead of us and supply side constraints are structural and repeating. TLs are currently trading near trough multiples, which makes them the best value in all of freight transportation,” Shanker said in his outlook piece.

Even though spot rates have reached new highs recently, he sees the current tight-supply-high-demand dynamic remaining intact for a while. He pointed to a proprietary shipper survey in which respondents said the “need to restock” inventories was at the all-time high for the survey’s 15-year history. He believes “at least 55% of the demand cycle is left to run.”

Shanker views this cycle differently given “unprecedented” supply constraints – drivers sidelined by the Drug & Alcohol Clearinghouse, rising insurance costs and diminished driver school enrollment. He said these headwinds “reset and restart on Jan. 1 of every year, making them ongoing and repeated structural constraints of supply.”

“We believe this cycle will end when demand rolls over – either driven by an end to the restocking cycle or an economic recession – neither of which are on the horizon in the near term,” Shanker continued.

Shanker expects the LTLs to benefit from “the rising TL tide,” with the likelihood of record operating ratios in 2021 for carriers as they continue to focus on operational improvements and benefit from higher demand. However, he’s slightly more cautious on the sector given the higher valuation multiples.

Stifel Financial’s (NYSE: SF) David Ross noted many of the same capacity constraints for TL when he published his thoughts on the new year. He believes more of the economy will reopen and the manufacturing recovery will continue as previously delayed capex spending gets back to normal.

He likes TL and intermodal over LTL based on valuation, but noted that LTL volumes are just turning positive for the first time in two years. He sees a constructive capacity setup for the LTL sector as active capacity is down and terminal counts aren’t growing.

Trucking rates accelerate in 2021

Ross believes the “supply constraints are real” and that “pricing [is] going higher” as “lean inventories [will] compel restocking well into 2021.” He’s calling for TL yields to improve 6% to 10% next year with LTL yields increasing 3% to 5%.

Shanker said even if spot rates have already peaked, they aren’t likely to fall anytime soon as contract rates have yet to close the gap. He believes the recent surge in truck orders is largely “catch-up replacement,” not incremental additions of supply. The thought is the current headwinds facing the industry are too cumbersome for most fleets to grow, keeping capacity in check.

Chappell expects contract rate increases to be in the high-single to low-double-digit range next year, but noted “the eventual completion of inventory restocking tailwinds, the end of goods-only consumer spending and the recent acceleration of Class 8 truck orders indicates that the market backdrop is presently as good as it gets.” He said pricing could begin to ease as early as the middle of the year.

Earnings outlook

Mehrotra believes earnings can come in well ahead of expectations. His base case assumes earnings-per-share growth of more than 20% for his entire transportation coverage next year with double-digit EPS growth in 2022. However, he expects TL earnings to peak in 2021, up more than 20% year-over-year, but eroding up to the same amount in 2022.

He sees 30% EPS growth at the nonunion LTL carriers next year, with a 15% increase forecast for 2022. Ample supply and price discipline throughout the industry are the expected drivers. He’s planning for high-single-digit percentage increases in LTL tonnage in 2021 followed by mid-single-digit growth in 2022. Growth expectations and favorable fundamentals “should allow the current high valuation to be sustained,” he said.

Chappell believes EPS increases are largely a 2021 event. The thought is future demand will taper as the traditional seasonal slowdown in the first quarter provides retailers the time to replenish thin inventories and a vaccine steers spending habits from goods requiring transport to services. He sees a ramp in spending on services occurring in the second half of 2021, around the same time inventories will have corrected and new Class 8 production begins to flood the market.

Even though the valuation on TL stocks may appear more attractive, he believes the group’s sell off is making it more evident that 2021 could be the peak for earnings in this cycle. He favors the more expensive LTL stocks given their multiyear earnings potential, which he ties to an improvement in the industrial economy that can account for more than two-thirds of LTL freight compared to less than 25% for the TLs.

Shanker said TL earnings will be “structurally higher” in all parts of the economic cycle on a go-forward basis, pointing to the late-2017 ELD mandate as raising both rates and EPS during the peak and trough since.

On its third-quarter call, Werner Enterprises (NASDAQ: WERN) indicated a similar sentiment, taking its long-term operating margin target for its TL segment up 200 basis points to an average of 13% throughout the cycle.

“We believe the rising tide of restocking/reopening-driven demand and recurring constraints on supply will lift TL earnings by roughly 50% in 2021, and even if the cycle ends in 2022, we will see a softer landing than we have historically seen,” Shanker said.

“Contrary to increasingly popular belief, making a new peak does not automatically mean that the cycle is over,” Shanker continued. “The real debate, in our view, should be whether TLs are worth even more as we raise historical multiples to reflect structurally higher earnings power. Instead, the stocks are already pricing in an imminent sharp decline in spot rates.”

At least in the near term, the outlook for trucking companies looks promising. Recent earnings reports from retailers showed that sales growth outpaced inventory build by more than two times in the recent quarter. The National Retail Federation recently upped its container imports forecast, following a record peak season, which if true means demand will be elevated through at least the first four months of the year.

The supply headwinds appear more structural than cyclical. Concerns over COVID will ease and enrollment at driver schools will improve as a vaccine is distributed. However, with CDL issuances down more than 100,000 in the first half of the year and only 10% of the 46,000 drivers with drug and alcohol violations returning to duty, the headwinds remain real and unlikely to be easily cured.

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now