American agriculture rarely makes front-page freight headlines, yet it quietly underpins a significant portion of trucking demand. Grain, livestock, fertilizer, seed, feed, refrigerated meat, packaged goods, ethanol, farm equipment—entire freight ecosystems depend on a stable farm economy. Recent reporting has highlighted a sharp rise in farm bankruptcies and growing concern from agricultural leaders about systemic financial stress. While these developments are often discussed in rural policy or commodity terms, they carry meaningful implications for freight markets that deserve careful attention.

A Warning From the Fields

Recent industry analysis has indicated a significant increase in farm bankruptcies during 2025, with filings rising sharply compared to the prior year. Agricultural leaders have expressed concern that if underlying pressures—input costs, debt servicing burdens, interest rates, commodity price volatility, and trade uncertainty—are not stabilized, broader structural consequences could follow.

The conversation is not merely about individual farms closing. It is about whether certain segments of American agriculture are operating under financial models that are no longer sustainable in the current economic climate. If consolidation accelerates or production contracts materially, freight does not remain untouched.

Agriculture is not a niche freight sector. It is a foundational one for our economy.

Agriculture’s Hidden Role in Trucking

Many small carriers may not directly haul grain or livestock, yet agricultural output drives multiple layers of freight demand. Consider how agricultural production moves through the economy:

- Bulk grain hauled to elevators and processing facilities

- Feed transported to livestock operations

- Livestock hauled to processors

- Refrigerated protein shipments to distribution centers

- Packaged food products shipped to retail

- Farm equipment distributed to dealers

- Fertilizer, chemicals, and seed delivered seasonally

If agricultural activity slows or consolidates, freight does not simply disappear; it restructures. That restructuring may reduce total volume in some lanes while concentrating it in others.

When production contracts, truck utilization patterns shift.

The Bankruptcy Signal

A 46% year-over-year increase in farm bankruptcies, as recently reported, is not a minor fluctuation. Bankruptcy filings are often lagging indicators, meaning they reflect financial stress that has been building over time. High interest rates amplify debt servicing costs, particularly for operations carrying significant equipment or land loans.

Commodity prices, meanwhile, have shown volatility across grains and livestock markets. When input costs remain elevated—fuel, fertilizer, labor—but output prices soften, margins compress quickly.

For trucking, compressed farm margins can mean:

- Delayed equipment purchases

- Reduced fertilizer and chemical demand

- Fewer livestock placements

- Lower throughput at processing facilities

- Reduced seasonal surge volumes

These shifts are not immediate freight collapses, but they create subtle downward pressure on specific sectors.

The Risk of Consolidation

If smaller farms exit at an accelerated pace, production may shift toward larger, vertically integrated operations. At first glance, consolidation may appear freight-neutral. Production continues; volume moves.

However, consolidation changes logistics behavior. Larger operations often negotiate long-term transportation contracts, rely on integrated supply chain systems, and optimize distribution differently than smaller, independent producers.

For small carriers who rely on regional agricultural freight or spot-based seasonal movement, consolidation could mean fewer independent shipping relationships and greater reliance on contracted capacity pools.

In other words, the structure of demand changes even if the total output does not immediately collapse.

Seasonal Freight Sensitivity

Agricultural freight follows seasonal patterns. Planting season drives fertilizer and seed shipments. Harvest season creates surges in bulk grain hauling. Livestock cycles affect reefer and live haul demand.

When farm financial stress intensifies, seasonal surges may soften. Producers may reduce acreage. They may delay capital investment. They may scale herd sizes cautiously.

For carriers who depend on harvest spikes to stabilize annual revenue, even modest reductions in yield or acreage can affect total freight availability.

Freight markets are sensitive to marginal changes in volume, particularly in already soft conditions.

Trade and Export Exposure

American agriculture is deeply integrated into global trade. Export demand influences grain prices and production planning. Trade disputes, tariff uncertainty, and shifting international demand can amplify domestic financial stress for producers.

If export flows weaken, domestic supply may increase, depressing prices and further tightening margins. Lower margins can lead to acreage reduction or lower input spending the following season.

From a freight perspective, export-sensitive regions—particularly those reliant on bulk grain movements to ports—could experience throughput variability. Trucking demand tied to port drayage, rail transload support, and regional shuttle movements may reflect these changes.

Freight does not operate independently of global agricultural trade dynamics.

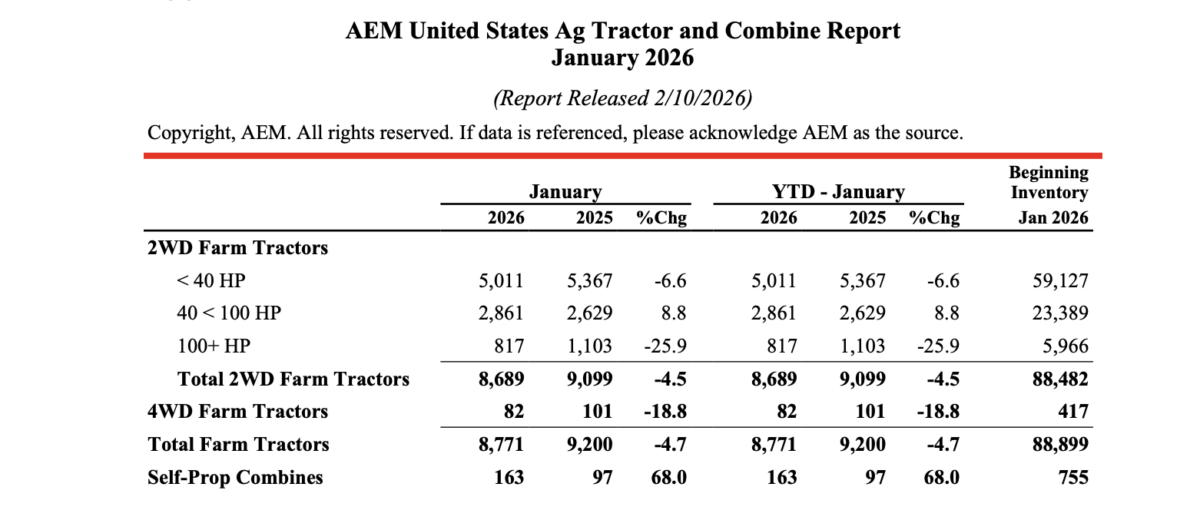

Equipment Demand and Secondary Effects

Agricultural stress affects more than commodity shipments. Farm equipment manufacturers, parts suppliers, and dealers rely on healthy farm balance sheets. If producers delay purchases, equipment freight slows.

Manufacturing facilities that produce tractors, combines, and implements depend on farm-level capital investment. Reduced demand in that sector influences flatbed and specialized hauling segments.

Even rural construction and infrastructure projects may feel secondary effects if agricultural profitability declines in certain regions.

The ripple effect extends beyond the field.

Fuel Demand and Biofuel Markets

Agriculture and energy markets are intertwined. Ethanol production depends heavily on corn supply and pricing. Biodiesel markets depend on soybean oil and other feedstocks.

If agricultural output contracts or price volatility persists, biofuel production margins can fluctuate. Ethanol plants generate consistent inbound and outbound freight. Variability in production levels can alter tank, bulk, and reefer freight activity in affected corridors.

Freight networks tied to agricultural energy markets should monitor these signals carefully.

The Psychological Factor

Markets are not driven solely by data; they are influenced by sentiment. If widespread media coverage amplifies concerns about agricultural collapse, lenders may tighten credit standards further. Producers may adopt more conservative production strategies.

When caution spreads, freight follows.

Reduced risk tolerance can suppress expansion, delay planting decisions, and constrain forward contracting activity. These behaviors may not generate immediate freight reductions but can dampen future growth cycles.

Why This Matters for Small Carriers

Small carriers often operate in regional markets closely tied to agricultural economies. A dry van carrier in the Midwest may indirectly depend on agricultural packaging plants. A flatbed operator may rely on equipment or input hauling. A reefer operator may depend on meat and produce shipments.

Agricultural contraction would not eliminate freight overnight. However, it could:

- Intensify competition for available loads

- Compress spot rates in affected lanes

- Increase volatility during seasonal transitions

- Shift bargaining leverage toward contracted carriers

Carriers who do not monitor agricultural fundamentals risk being surprised by freight softness that originates outside traditional freight metrics.

Watching the Right Indicators

Carriers seeking early warning signs should monitor:

- Farm income projections

- Bankruptcy filing trends by agricultural district

- Commodity price futures for major crops

- Export shipment volumes

- Fertilizer and input sales data

- USDA acreage and yield forecasts

Freight does not move in isolation from these indicators.

If farm income stabilizes and input costs moderate, agricultural freight could remain resilient. If financial stress accelerates, freight-sensitive segments may soften further.

Avoiding Overreaction

It is important not to assume imminent collapse. Agriculture has historically endured cyclical downturns. Producers adapt, restructure debt, and adjust planting strategies. Consolidation has been ongoing for decades without eliminating freight demand.

However, the scale and pace of current financial pressures warrant attention.

The risk lies not in panic but in complacency.

A Freight Market Already Under Strain

Trucking markets have experienced prolonged softness in recent cycles. If agricultural contraction adds incremental pressure in rural corridors, recovery timelines could extend in those regions.

Freight markets are influenced by manufacturing, retail, housing, and energy demand. Agriculture is one of the largest pillars supporting rural freight ecosystems. Weakness in one pillar may not collapse the structure, but it can strain balance.

Strategic Considerations for Carriers

Carriers operating in agriculture-dependent lanes may consider:

- Diversifying freight portfolios beyond seasonal agricultural reliance

- Strengthening direct shipper relationships where possible

- Monitoring regional volume shifts closely

- Adjusting capital expenditures cautiously

- Preserving liquidity during uncertain cycles

Freight cycles reward disciplined operators.

Conclusion

Rising farm bankruptcies and warnings of broader agricultural instability represent more than rural headlines. They may foreshadow structural shifts in freight volume, lane stability, and regional trucking economics.

Agriculture remains one of the most freight-intensive sectors in the American economy. When its financial foundation shows signs of stress, transportation markets should pay attention.

Freight professionals who understand upstream economic signals gain strategic advantage. Watching the farm economy is not optional for carriers operating in agricultural corridors—it is part of reading the freight map accurately.

If the farm belt stabilizes, freight benefits. If structural strain deepens, trucking will feel it even in recovery mode.

The prudent approach is neither alarm nor indifference—but informed awareness.

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now