Trucking executives were on hand on May 19 to discuss freight markets at the 13th Annual Wolfe Research Global Transportation & Industrials Conference. The panel format covered topics like demand, pricing and a potential restart.

Overview of freight trends

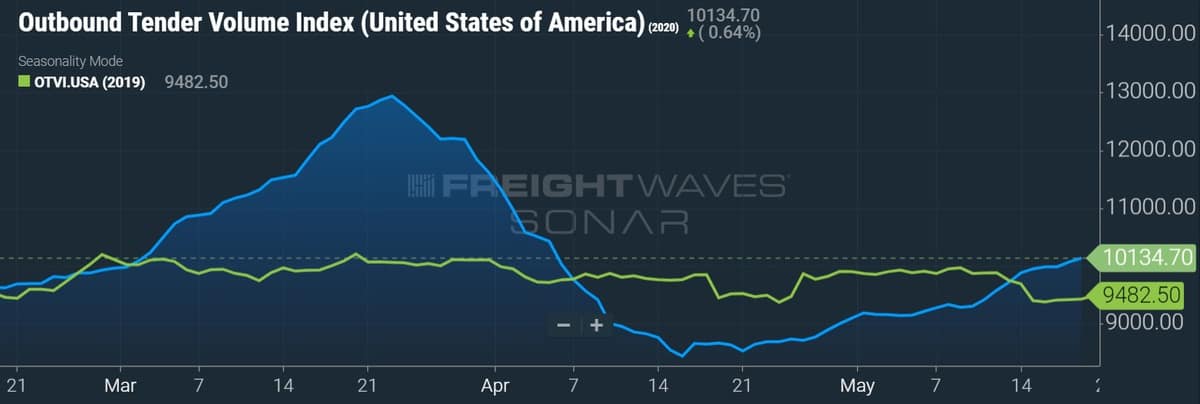

U.S. Xpress’ (NYSE: USX) President and CEO Eric Fuller said the company continues to see consistent volumes as the bulk of the carrier’s freight comes from grocery, discount retail and home improvement stores. In the company’s first quarter 2020 report, the carrier reported only 4% of its revenue was tied to customers that were forced to shut down during the pandemic. Fuller expects the company’s truckload (TL) results to be flat sequentially with the first quarter during the second quarter, noting the company reported its highest revenue week of the year two weeks ago.

Chairman, President & CEO Alain Bedard of Canada’s largest trucking company TFI International (TSX:TFII) said the company’s business has “plateaued” in recent weeks, still down 15% to 20%. Bedard said he was “really proud” of the TL division’s performance during April, a month the unit saw a 20% decline. He said the company’s B2B business has been off 30% to 35%, but an increase in B2C freight has helped fill some of the gaps. Bedard said conditions have stabilized and demand is coming back on line, stating that TFI’s final mile segment was up in April and so far in May compared to 2019.

Privately held TL carrier CRST International has been forced to park some of its fleet during COVID-19. The carrier has a full TL offering – dry van, dedicated, flatbed, specialized and final mile. The company’s President and CEO Hugh Ekberg said it’s “still a tough market,” but he believes it is bouncing off the bottom. CRST International’s flatbed and specialized volumes have been down approximately 30% in April and May, with flatbed rates down approximately 11% over that stretch. Ekberg said dry van volumes are about 15% lower and rates are down 10%. The company’s dedicated unit, approximately 40% of revenue, is “holding up well.”

TL rates and capacity

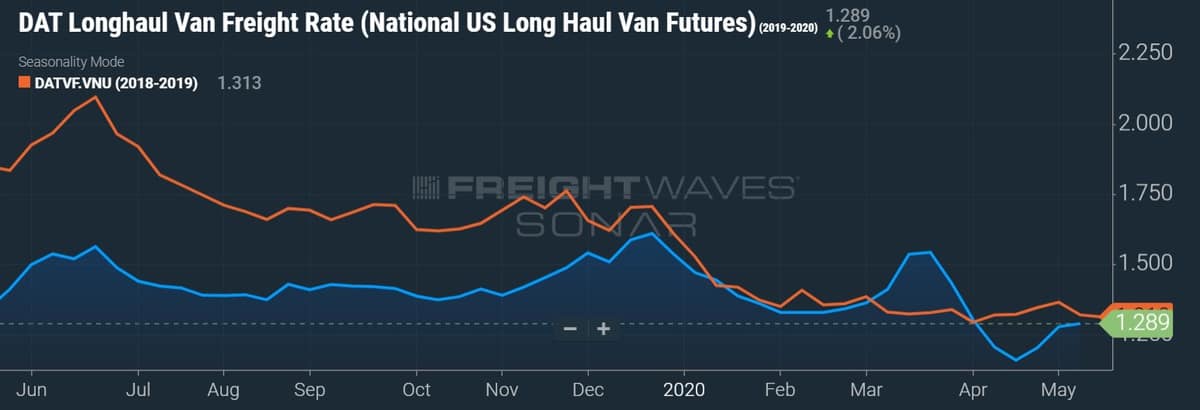

Bedard said contract rates are seeing some pressure, but he doesn’t believe the recently negotiated softer rates will stick in six months’ time as the economy ramps higher. He said TL rates are holding up better in Canada than the U.S., noting gross margins have been protected. The company has little exposure to the spot market.

Fuller said U.S. Xpress is seeing about 12% of its freight come from the spot market currently, a figure he would like to move to 10% or less. He said spot rates are slightly lower than February and March levels. He doesn’t see rates dipping further as they are currently near break-even with variable costs incurred to move the load. Fuller said contract rates are flat to down in the single-digits, but the year-over-year declines are similar to those seen in the first quarter.

Ekberg said spot rates are driving the company’s overall rate per mile lower as the carrier’s spot exposure has increased to 16% to 17% of the freight it carries. He said there has been some “rate give” in recent contractual negotiations in order to maintain or win volume, but the carrier has been successful in procuring the freight needed to maintain miles and equipment utilization. On profitability, he expects the company’s operating ratio to step down sequentially during the second quarter, but expects the company to remain profitable.

Regarding when rate per mile increases, all three participants on the panel see this happening on a sequential basis at the end of the third quarter or early in the fourth. Ekberg said it would take a peak season and capacity leaving the market to happen. On a year-over-year basis, Ekberg doesn’t think rate per mile will move positive until 2021.

Fuller believes rates could move higher year-over-year in the third quarter/fourth quarter time frame, but said “a lot of capacity” has to come out of the market. Fuller sees recent paycheck protection loans as the biggest impediment. “Stimulus has propped up marginal carriers that would have gone out of business otherwise.” He said if there was another round of stimulus, the unfavorable capacity and rate dynamic will be prolonged.

On capacity, Bedard said most small carriers are financed by a bank that “doesn’t want to be a trucker” and will look to keep them open as best they can so they don’t have to take possession of the assets.

Brokerage, dedicated and used truck prices

Everyone acknowledged the competitiveness in truck brokerage currently. Fuller believes the margin squeeze in the market will force the issue with newer industry participants, which have been well-funded and solely focused on capturing market share at the expense of rate. He believes profitability of these companies will come into focus as their capital runs out and expects them to either be acquired or merge with incumbent players with some falling to the wayside.

On dedicated opportunities, Ekberg said there are plenty of good opportunities to capture incremental dedicated freight, although he acknowledged it is tough to tell if shippers are spooked by the expected capacity purge from bankruptcies, cost inflation, increased regulation, etc., or if they are looking to lock in three-year contracts on truck capacity in a weak rate environment.

Fuller and Bedard see favorable tailwinds for dedicated demand, but noted several carriers that aren’t traditional dedicated players are now bidding on the freight, creating a headwind as they haven’t engineered a dedicated network and aren’t pricing the freight correctly.

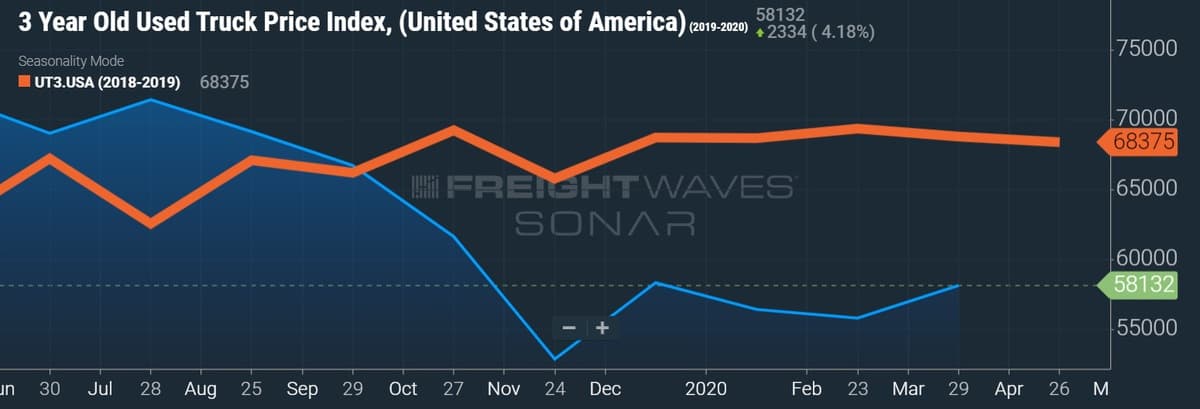

On used truck prices improving, Bedard said the over-buying of tractors during and after the 2018 freight peak is the “stupidity of industry” and will likely take 12 to 18 months to unwind. Fuller believes it could happen in a year as industry orders remain very low. He believes when the turn occurs it will happen quickly as larger carriers will occupy original equipment manufacturers’ (OEMs) order books initially, forcing the smaller carriers to buy used until they can find OEM production slots.

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now