The views expressed here are solely those of the author and do not necessarily represent the views of FreightWaves or its affiliates.

My thesis is that the railcar fleet could be right-sized to just four basic railcar types. There are too many boutique car types – now we must find common ground and agreement among all the parties involved.

In my last commentary, I closed with the following: The rail industry is still generating strong cash flow. …there is a random possibility that a full GDP recession might further exacerbate the car supply dilemma.

A week later, events now suggest more clearly that the railroad freight industry faces a recession. Therefore, I will examine how a recession might spur a strategic opportunity for improvement and a look at overall railcar fleet requirements.

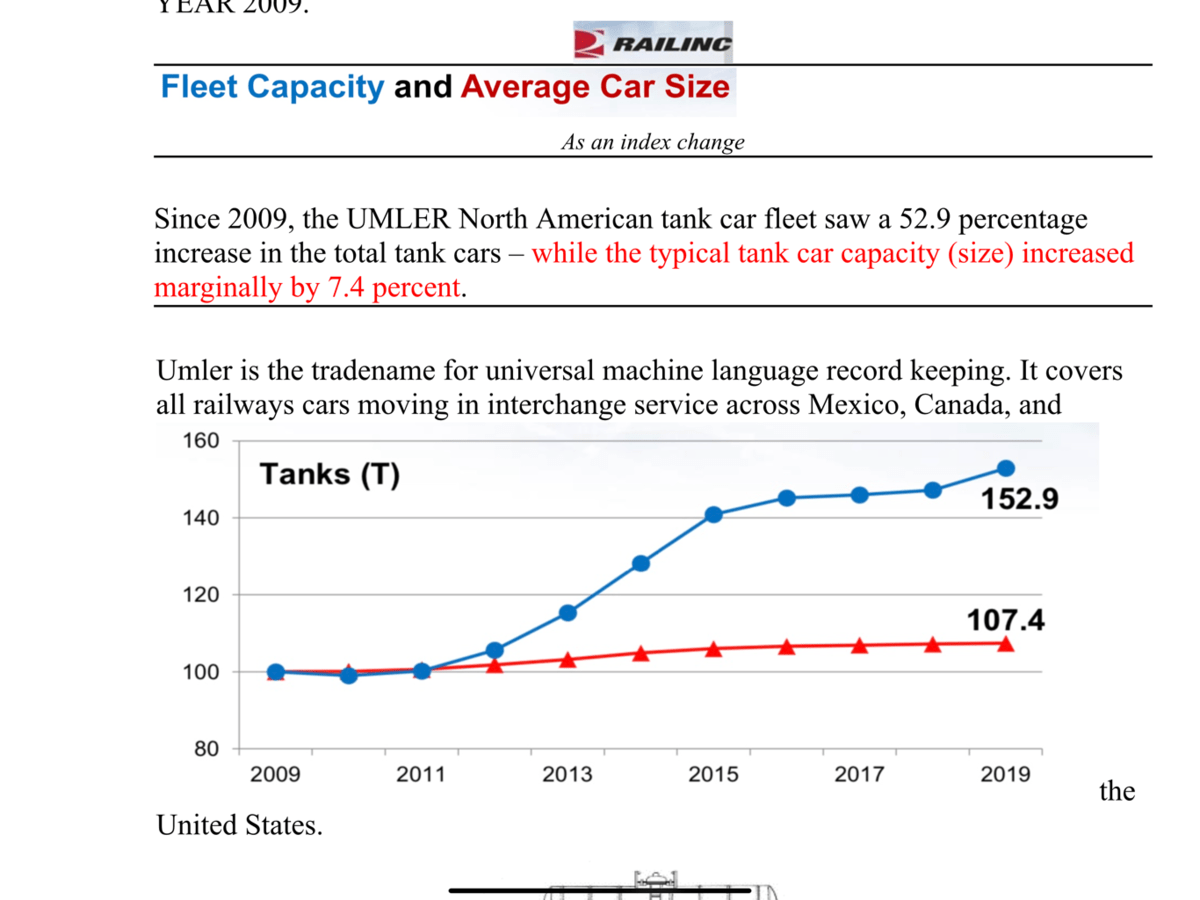

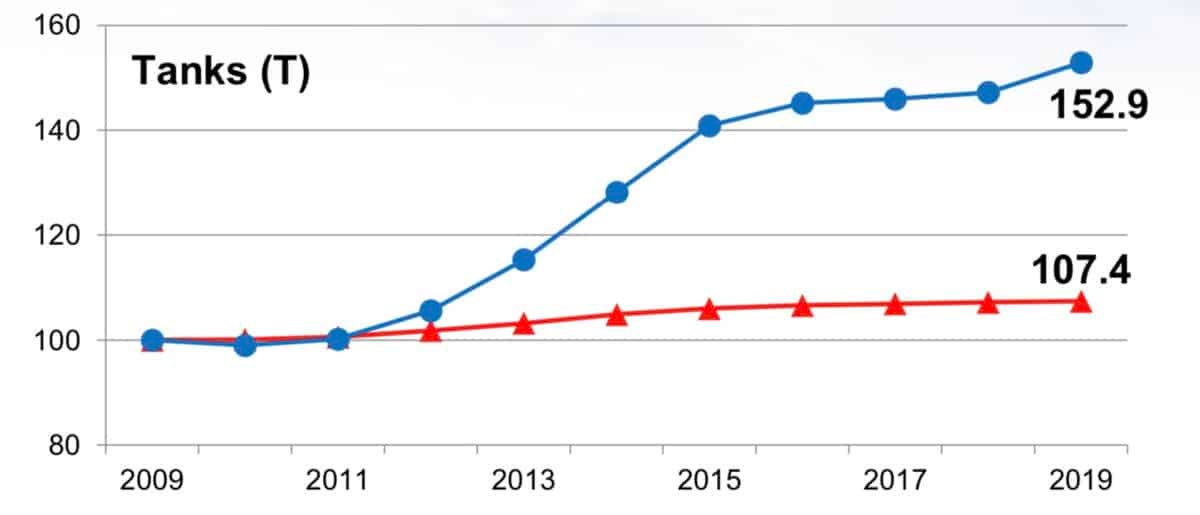

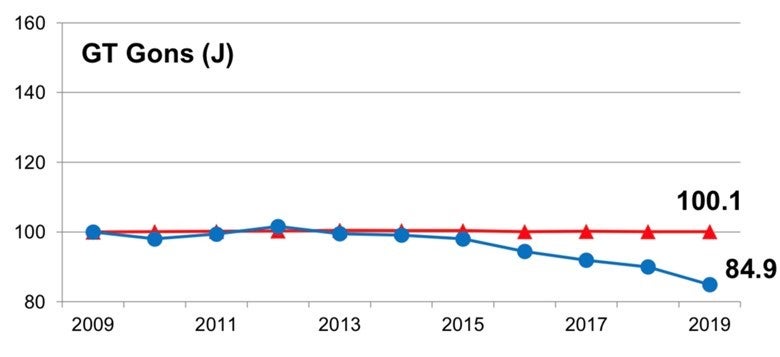

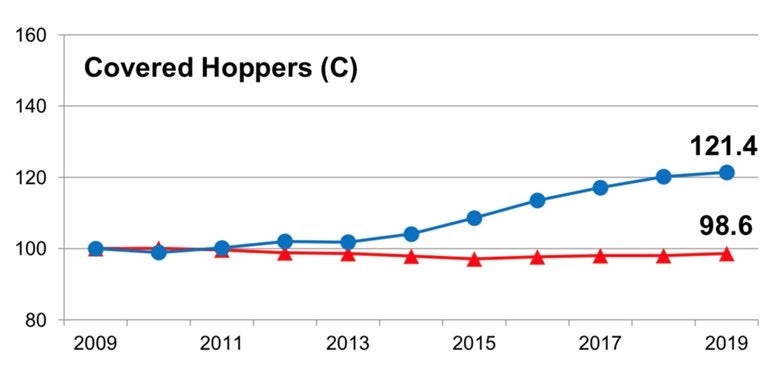

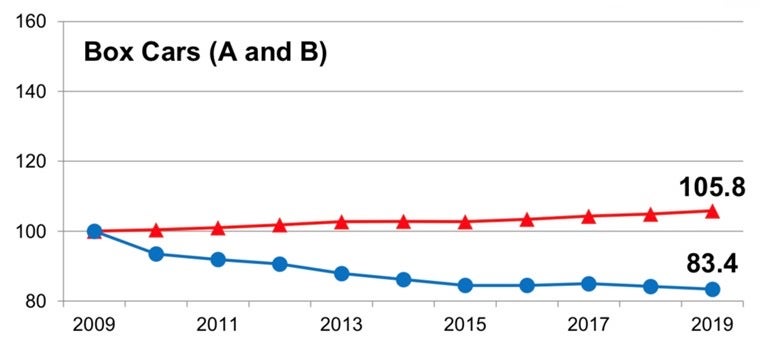

There are four basic commodity railcar types. They are: tank cars; covered hoppers; gondolas; and boxcars. The graphs below suggest the relative size of the fleet that each of these four car types occupies.

The changes in the year-to-year fleet size compared to the changes in fleet capacity for each railcar type shown are indexed to a standard of “100” as of the end of the year 2009.

Since 2009, the UMLER North American tank car fleet saw a 52.9 percentage increase in the total tank cars – while the typical tank car capacity (size) increased marginally by 7.4%.

UMLER is the trade name for universal machine language record keeping. It covers all railcars moving in interchange service across Mexico, Canada and the U.S.

The very large covered hopper car fleet of all cubic sizes and commodity-carrying purposes saw a net 21.4% change in the units with a modest 1.4% decline in the average car size.

The size range varies quite a bit. Small cars are often less than 3,500 cubic feet, while jumbo hoppers are larger than 5,000 cubic feet. The net carrying capacity of cargo varies from a low of 70 tons to as much as 110 tons.

Over the past decade, smaller capacity cars were added to move frac sand to the shale oil fields. Covered hoppers carrying grain and plastic pellets typically move in the larger cubic capacity design. Looking ahead, we can expect the smaller car fleet to shrink; while the larger hoppers increase.

Gondolas come in mixed sizes for different market roles. Many “gons” are used for scrap steel or rolled steel movement. This graph examines only the coal-hauling gondola type.

With coal traffic declining, the average number of gondola coal cars has dropped since 2009 by ~15%.

Since almost all coal cars (open top hopper or gon) in North America are of the heavy axle design (286,000 pounds gross weight), the average car size is steady at really no change (100.1 index).

Many 40-foot boxcars and some 50-foot boxcars were retired over the past decade. The average carrying capacity of the fleet grew by about 6%. The total fleet transformed into larger frame and length sizes. However, railway customers (receivers and shippers) are concerned because the total fleet size has continued to shrink. The total boxcars available are down by about 16%.

Prospects for fleet replacement are not yet clear. There is definite resistance to buying new boxcars.

As a benchmark, here are the overall characteristics of the freight railcars in service as of February 2020:

| Fleet size | 1,627,914 | 100% |

| Heavy axle units @286,000 gross pounds | 1,064,954 | 65% |

| Units at 263k to 270k gross pounds | 505,800 | 31% |

| How many different car types were added in past year? | ~138 | |

| How many car types were subtracted in year past year? | >350 |

Here were the biggest fleet changes to note during full-year 2019:

- Total fleet size up about 0.5%

- Increases included: 15,000 tank cars (+3.4%), 2,000 covered hoppers (+0.4%)

- Fleet Decreases: 11,000 coal sector gondolas/hoppers, 2,000 boxcars

What do railcar investors want?

Since the average price of new freight railcars has increased significantly to now more than $110,000 per unit, the emphasis is on finding ways to reduce the capital cost of replenishing the carload fleet.

One way is to increase the average loads moved per car each year. Often the average number of loads is less than 12 per year – much too low for the investment made. I wrote previously about how loads per year can generate more net cash – and thus a better ROI.

Other issues revolve around the complexity of the railcar fleet itself. There are too many railcar types in the fleet relative to the push for more precision-like railroad operations. The railcar type complexity represents a business model mismatch.

Translation? The large mix of railcar types makes switching, railcar placement, and train make-up operations more complex than the railroads want. It is out of step with the current concept of managing to maximize rail carrier operating ratio goals.

A few of the Class 1 railroads are very direct about this railcar issue. The latest industry documentation comes from Union Pacific as it recently addressed railcar investors and railcar owners.

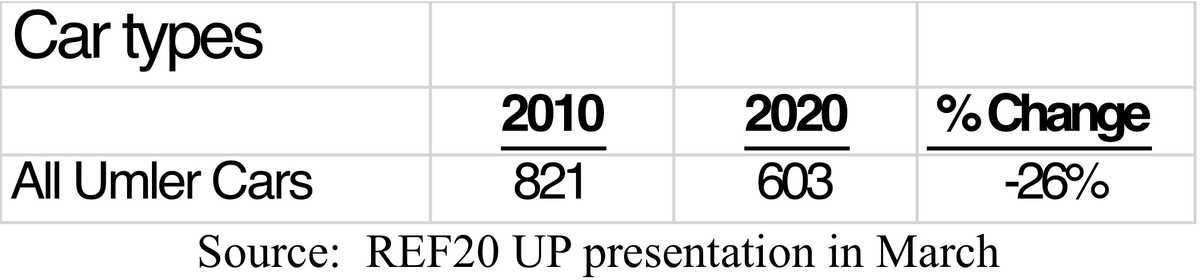

While there has been some improvement in the past decade, over 600 railcar types is still too many.

Note: there is an alternate view by some that the baseline was only 658 car types. That would have been ~8% car type reduction over the decade. The difference is about cars with only two units in each category.

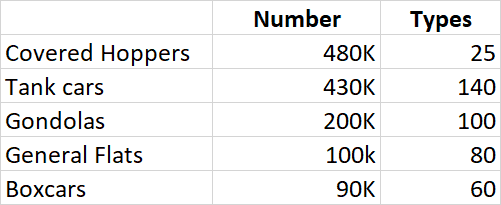

Here is another way to examine the railcar types issue – the approximate size segmentation of the overall fleet for five major car types with the approximate number of different types within each group. This includes the four railcar types mentioned above plus general flats.

Base year 2020. All numbers rounded off. Some railcar types excluded.

Here is the strategic question. What is a best practice method to resolve the North American fleet towards 2025-2030?

How does the industry gather the diverse investors together to reach a resolution?

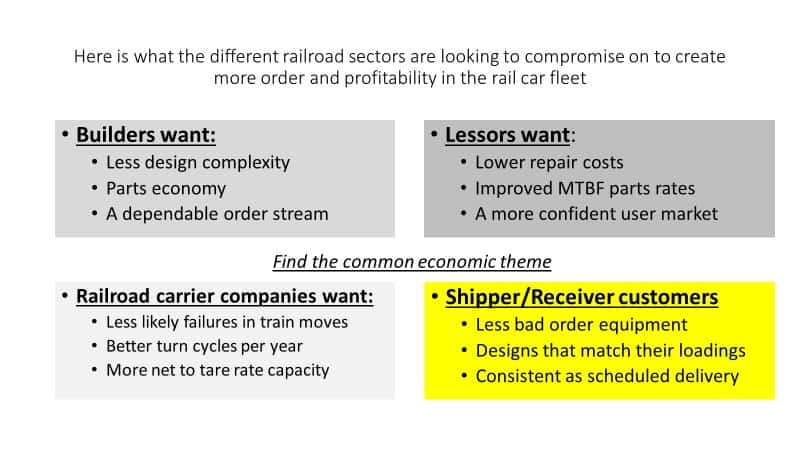

One start is to describe the main goals of each of the invested parties and then negotiate towards a common set of objectives. Here are the framed objectives for four major parties.

Fundamentally – as market share by rail freight has been decreasing, freight railcars have remained much like a boutique market niche.

The business principles of streamlining assets for multiple use and users hasn’t yet sunk in as the rail freight model.

As a strategic comparison, think about Southwest Airlines’ aircraft fleet model – few types that almost any of its pilots can fly – and with simplicity of parts inventory to keep them flight-worthy.

That’s a missed SWOT “opportunity” yet to be captured for rail freight.

Making the investment decisions work out better requires having multiple parties “having skin in the game” – some exposure to capital risk by all parties.

In summary, there is a real opportunity for better fleet utilization and the benefit of much lower capital costs by increasing overall utilization.

One method is to try and shift from using freight railcars as the backup mode and instead rely on the railroads as the shippers’ “base load.” However, that requires customer confidence in the railroads’ on-time delivery promises. Is that precise, truck-like scheduled delivery there yet?

One recent speaker from GATX may have stated the objective well.

A new approach?

Perhaps it’s time to revise the entire railway fleet “carpooling” business model. Car pooling unquestionably improves loads per year.

Added loads per year generates more cash to cover the fleet capital costs while keeping the fleet size down and simultaneously reducing billions in capital costs.

How quickly? If the parties were to negotiate over just two to four of the suggested car types written about in this commentary, could they reach agreement in the next 11 months on some critical improvements tactics?

Who is a leader or a “facilitator? What’s your opinion?

Acknowledgements

The following parties had well-documented ideas. Yet, they might disagree with this observer’s summary. If you want more information/intelligence, check with them please. Always seek a second opinion.

- Adam Simeon, General Director of Equipment Distribution at Union Pacific

- David Humphrey, PhD., Senior Data Scientist at Railinc.

- GATX Corporation

- CSX customer info: https://www.csx.com/index.cfm/customers/resources/equipment/railroad-equipment/

- Jesse Crews, Chief Investment Officer at Trinity

- Ross Corthell, Vice President of Transportation, Packaging Corporation of America

- Patrick O’Neil, Senior Director of Fleet Planning & Optimization, Norfolk Southern

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now