The views expressed here are solely those of the author and do not necessarily represent the views of FreightWaves or its affiliates.

In early September, the U.S. Department of Transportation (DOT) published an updated national freight plan. Was that a big deal or a little deal? Well, if states, towns and private companies want to obtain possible federal grants and/or loans for any transport projects (including rail), yes, it is an important benchmark.

Let us recite what the national “plan” document could enable. First, what’s the document all about: It is a position statement that after about five years since the previous DOT strategy document was released, this update presents a fresh perspective about the market outlook for goods movement and the challenges ahead.

However, it is not actually a concrete and specific plan. It’s mostly an outlook discussion with some data points and metrics about market scope and size.

No. It is not actually a committed funding program to get things built. Consider it instead a statement of possible intent. Perhaps directional changes.

Importantly, it is intended to incite logical and sometimes contrary discussion.

Railway and this revised DOT outlook

What does the report tell us commercially about the railroad industry sector and its future role and possible requirements for improvement?

Well, one interpretation is that the railroad freight role is likely to be somewhat limited over the next several decades.

That is this columnist’s market-strategic interpretation of the report.

Note — this column does not offer a translation that either the government(s) or the industry sector would agree with.

If we examine the report’s statistics and graphs, it is clear that rail freight is not now and may not in the future play the leading “mode” transport role.

If we look back over the previous decades, the rail role has been diminishing as to market share of volume. That’s suggested by Washington government analysts to continue.

Others in Washington might disagree.

But this analyst’s interpretation is that the plan suggests no railway sector rebirth or confirmed market share grab rail freight role ahead.

Yes, rail might take market share from trucking or possibly waterborne commerce in some “corridors,” but nothing in the federal story suggests that this will in fact happen.

There is, however, one important finding by DOT.

The federal analysis confirms that the railroad private track infrastructure (lines of steel rails, bridges and tunnels, and other hard fixed assets) are in better physical shape than are our nation’s locks and dams, and highways.

That is a rail sector business case advantage.

But a good-condition assets base by itself doesn’t guarantee a mode shift from highways or water transport modes back to railroad.

That traffic mode diversion strategy long advertised as coming by railroad executives remains a big challenge.

Not much evidence exists that this has been happening over the past five years. Selectively in intermodal? Yes. However, no overwhelming rail intermodal market share gain from the highways in the recent period. Why not?

A number of the railroads seem much more focused on margin preservation versus growing their share of the market volume (as discussed in previous RR market view FreightWaves columns).

Somewhat ironically, the railroads’ most noticeable strategic strength is its hard-won battle to become the strongest of the modes in financial terms.

They have as a group learned how to earn from their customers the rail industry’s cost of invested capital. As a result, there are strategic and public policy consequences.

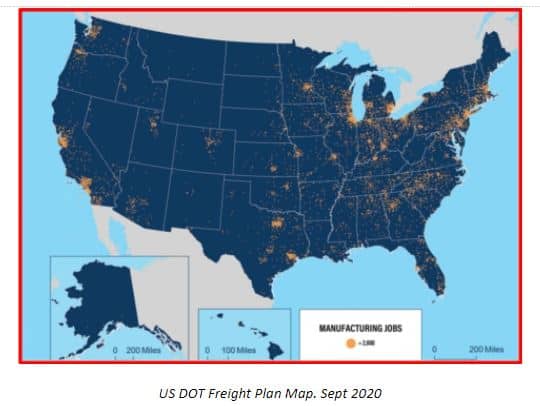

As further geographic market evidence of where the commodity flow demand will be, here is a map showing the concentration of the manufacturing industry.

Figure 3 (below) shows manufacturing activity as signified by the pattern of jobs. How will rail freight grow as a service sector in such subregions?

We can clearly see where the demand corridors will be located. The challenge then becomes to see how this matches up with future rail service.

Can or will the railroads step up with a short-haul solution? Are such selected short-distance markets in their economic tool bag?When will we know?

What are your commercial views as to the railroad capabilities? Are you engaged yet in reconsidering these issues in policy and tactics discussions with Washington technical and policy analysts?

Have you elected yet to reassess the commercial cost and benefits of already conceptualized local state and urban goods movement region plans for railroads?

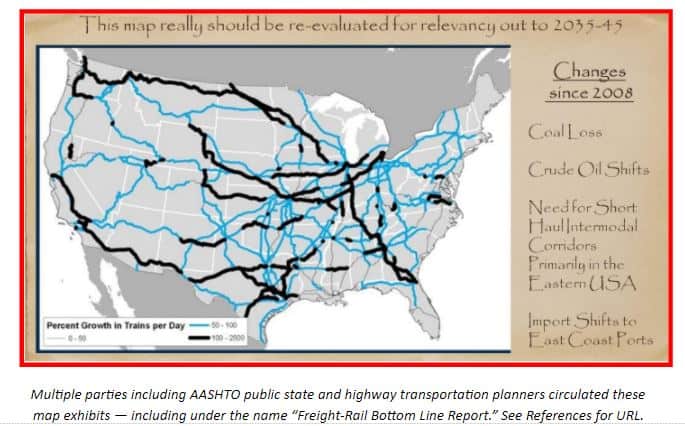

One other argument suggests the need for reevaluation of strategic rail investment needs.

Figure 4, below, identifies where the expected rail capacity growth would be needed when strategic planners huddled back in the 2004 to 2008 period.

Actually, this was a groundbreaking railroad analysis at the time.

However, beginning sometime after 2006 to 2009, the national marketplace for U.S. railroad traffic shifted. Key commodity routes like Powder River Wyoming coal origin traffic flows changed — as did eastern U.S. origin utility coal flows.

More recently, imports of Pacific containers have migrated toward the Gulf Coast and the Atlantic Ocean U.S. ports as shippers diversified their supply chains away in part from the Pacific U.S. ports.

Rail corridors that were to grow heavy future volumes of train per-day traffic now face a new market view.

Therefore, it is now time to reexamine the former strategic market change assumptions.

This fits right into DOT’s 2020 call for discussion.

Here is the major conclusion offered in this week’s rail freight market long-term view. DOT has tendered a document that bears serious reading.

Collectively, we can “officially” re-vet our previous freight logistics data assumptions and the capacity and market demand outlooks. Here for the rail sector. DOT Secretary Elaine Chao asked for our feedback. She did not give us a fixed solution.

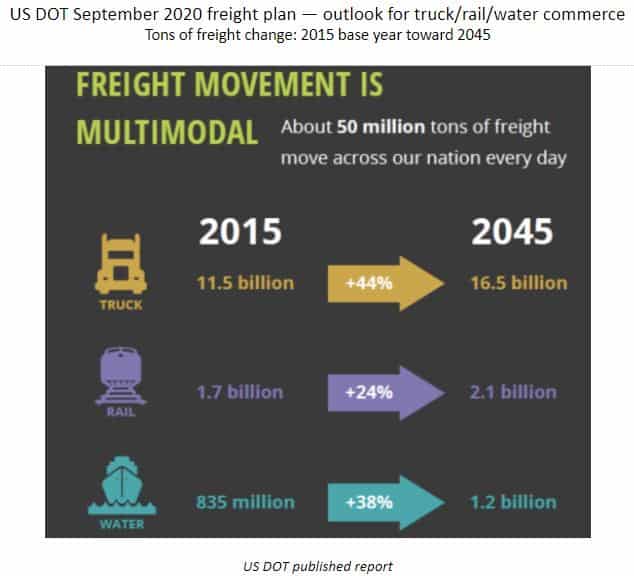

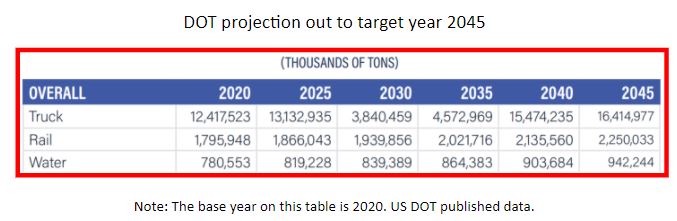

As we close this discussion, here is a summary of the DOT outlook toward year 2045 from their report.

Note: Rail freight looks to grow about 25% when using DOT economic formulas. Trucking is closer to a one-third increase. That will not be a railway market share gain. What is rail industry management’s response to this outlook?

Economic recommendations

DOT has afforded the rail community an opportunity to comment. Who, colleagues, is going to step up and offer contrarian ideas? Not to trash in-place initiatives.

No. Many CAPEX rail initiatives already underway or completed are simply sunk costs. Let’s try to earn a return from them as they were designed.

Instead, let us seriously consider what’s happened or is now occurring in today’s marketplace that could make a difference already in the path ahead.

For the railroad company boards and senior officers, their challenge is to consider how to reallocate cash flow into growth projects that might best be self-funded.

Asking for government assistance might logically for many projects no longer be appropriate.

Public agencies being asked to partially fund PPP rail freight projects not yet under formal negotiated terms and conditions contracts perhaps should retest the projects’ financial feasibility. Use something other than just a do-or-do-not net present value financial model to estimate cash flows. Instead, consider using cost center and pro forma profitability models for a deeper understanding of which PPP party obtains cost versus benefits — and the risk-sharing agreement terms.

If you are interested, give me a call. I’d like to help. After all, I have sat during my rich career at most of the table sides from MPO (CATS) to state DOT (I-DOT) to federal (USRA) to rail carrier (CONRAIL) to engineering consultancy (Zeta Tech) and even on behalf of selective shippers.

I’ll volunteer.

As always, please share your optional opinion and reasons why. That’s how we both learn.

Recommended references:

Readers are encouraged to read the executive summary of the DOT plan point of view: https://www.transportation.gov/sites/dot.gov/files/2020-09/NFSP_execsum_508.pdf

Or they may read the entire report of just over 100 pages here: https://www.transportation.gov/sites/dot.gov/files/2020-09/NFSP_fullplan_508.pdf

Previous documented studies recommended for reading include:

AASHTO and others; Freight-Rail Bottom Line Report: https://www.camsys.com/publications/case-studies/freight-rail-bottom-line-report

Also, check for selected more recent changed strategic assumptions offered by the consultants, working with some of the state DOTs.

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now