On its second-quarter earnings call with analysts on Thursday, August 6, management from the nation’s largest flatbed carrier Daseke Inc. (NASDAQ: DSKE) said the business is holding up well even as revenue has been challenged by the pandemic.

Volumes troughed in April, modestly improving sequentially in May and again in June. Management said July has provided more of a “a sideways movement” as demand began to plateau at the end of June. More specifically, management said flatbed capacity demand for wind energy and lumber has been strong. Demand for building materials has held steady and the defense sector is coming back on line. Softness in the aerospace and metals verticals have provided a partial offset.

While revenue is likely to be flat sequentially from the second quarter to the third quarter, the carrier has several cost catalysts that will allow it to improve its operating ratio (OR) sequentially over the same period.

Daseke’s $45 million restructuring plan remains on track. The carrier achieved the first $30 million in operating income improvement on an annual run rate basis exiting the first quarter. The incremental $15 million annual run rate is expected to be achieved by the end of the year. Management said the longer-term OR potential for the company is sub-90%.

The Addison, Texas-based carrier reported second-quarter adjusted net income of $0.10 per share in a Thursday morning press release ahead of the market open. The result was well ahead of the consensus estimate of a $0.09 per share loss and better than $0.03 per share recorded in the year-ago period. The result was adjusted to exclude the costs associated with restructuring and transforming the business.

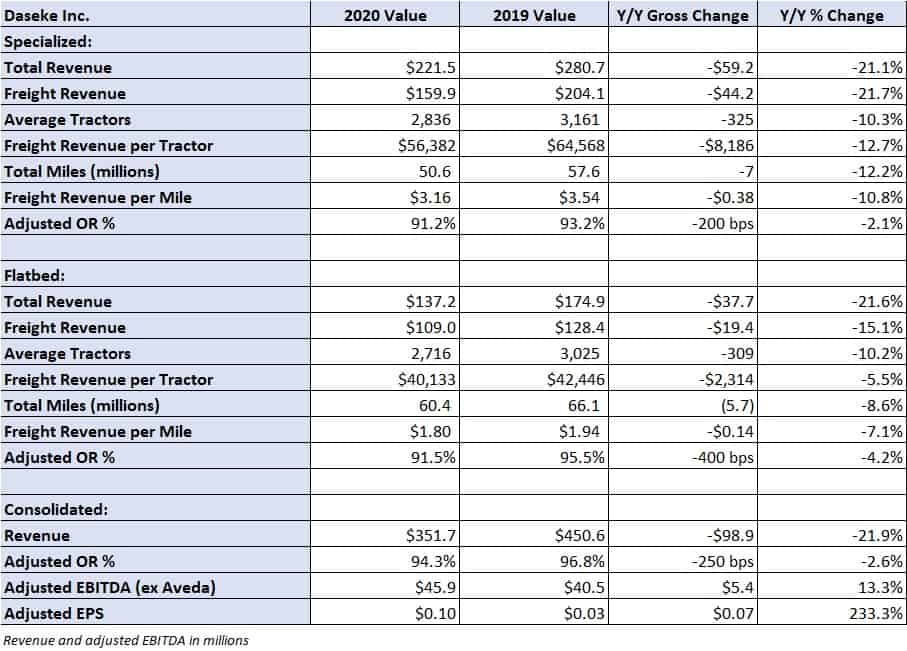

Second-quarter results

Daseke reported a consolidated revenue decline of 22% year-over-year to $352 million, which included a 10% year-over-year reduction in the total tractor fleet. The reduction is part of the carrier’s efforts to improve its capital structure and equipment utilization.

Revenue was down 13% excluding results from its oil rig transportation unit Aveda Transportation and Energy Services, which is in the process of being divested. The revenue decline was offset by strategic long-term cost reductions – tractor, trailer and headcount reductions, and the roll up of previously acquired but separately operated flatbed carriers. These actions led to a record OR of 96.5%, or 94.3% after adjustments and excluding the results from Aveda.

Adjusted earnings before interest, taxes, depreciation and amortization (EBITDA) excluding Aveda increased 13% year-over-year to $46 million.

Daseke recorded $48 million in net proceeds associated with the disposal of property and equipment, and working capital reductions at Aveda. The company expects to use $7 million to $10 million of cash in the third quarter to complete the divestiture. When completed, revenue from the oil and gas markets will account for less than 2%, compared to 13% in 2019.

Specialized freight revenue fell 22% year-over-year with revenue per tractor declining 13%. Total miles declined 12% and rate per mile moved 11% lower. Excluding Aveda, specialized revenue was only off 6% with rate per mile up 5% and revenue per tractor up 1%. The division reported a 91.2% adjusted OR, 200 basis points better year-over-year. The division’s adjusted OR was 89.5% excluding Aveda.

Flatbed freight revenue declined 15% year-over-year with total miles down 9% and rate per mile down 7%. The division reported a 400-basis point improvement in OR at 91.5%.

Daseke ended the quarter with cash of $157 million and $83 million available on its revolver. Total debt was $689 million, $532 million net of cash, with a net debt-to-adjusted EBITDA leverage ratio of 3x, below the company’s 4x leverage covenant and lower than 3.2x at the close of the first quarter. Net debt has been reduced $118 million and liquidity has improved $91 million since the second quarter of 2019.

Daseke lowered the average age of its tractors to 3.4 years in the quarter from 3.8 years at the beginning of the year. Average age includes some specialized and locally used assets that are kept in service much longer than traditional over-the-road tractors. The company’s goal is an average tractor age in the low-three-year range.

Shares of DSKE are up 20% in midday trading compared to the S&P 500, which is flat on the session.

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now