July Economic Roundup

As part of FreightWaves’ overall coverage of freight markets, it publishes a summary of the changes in the economy over the past month, both in terms of the data releases and developments in public policy. The Economic Roundup is designed to synthesize the events of the past month as they relate to freight markets, and provide a guide to trends to keep an eye on in the upcoming month. The Roundup is published on the first business day of each month with the next release scheduled for Wednesday, August 1.

Overview:

Developments over the past month continue to point towards an economy that is losing momentum overall after strength at the start of 2019. Data releases in June (mostly covering May activity) signal that freight economy has stalled since the start of the year. Manufacturing, housing, and trade have all either flatlined or outright declined thus far in 2019, with only retail providing support for freight activity in the economy.

The goods side of the economy continues to operate under the specter of the current trade conflict with China. The protectionist measures enacted over the last year have had the direct effect of hindering trade between the two nations, which by itself has restrained freight activity in recent quarters. In addition, the trade war has introduced considerable uncertainty into the outlook, and businesses have responded by holding off on spending and investment until there is more clarity. The U.S. made some positive strides in June by avoiding tariffs on goods from Mexico and reopening talks with China, but any recovery in the freight economy is likely to be modest until more comprehensive resolutions on trade policy are reached.

GDP

Real GDP growth was finalized at a 3.1 percent annualized pace of growth in the first quarter, unchanged from previous estimates and up from the 2.2 percent pace in the previous quarter. Year-over-year growth remained strong at a near four-year high of 3.2 percent as the economy remained on the accelerating path that began in the middle of 2016.

There were some minor changes in the details of the GDP revision, but the strength in the economy stemmed primarily from inventory building and a reduction in the size of the trade deficit.. Private final goods demand, which has closer ties to freight activity, was essentially flat at the start of 2019, as goods consumption, business investment on equipment and structures, and housing all either sputtered or declined.

Trend to watch: All signs point towards a slowdown in GDP growth when second quarter numbers are released later this month. Inventory building and international trade are not likely to make the same large contributions as they did during the first quarter, which should lead to growth settling in around 2.0 percent. In terms of freight, consumer spending on goods has been growing at a stronger pace during the second quarter, but all other areas remain fairly weak.

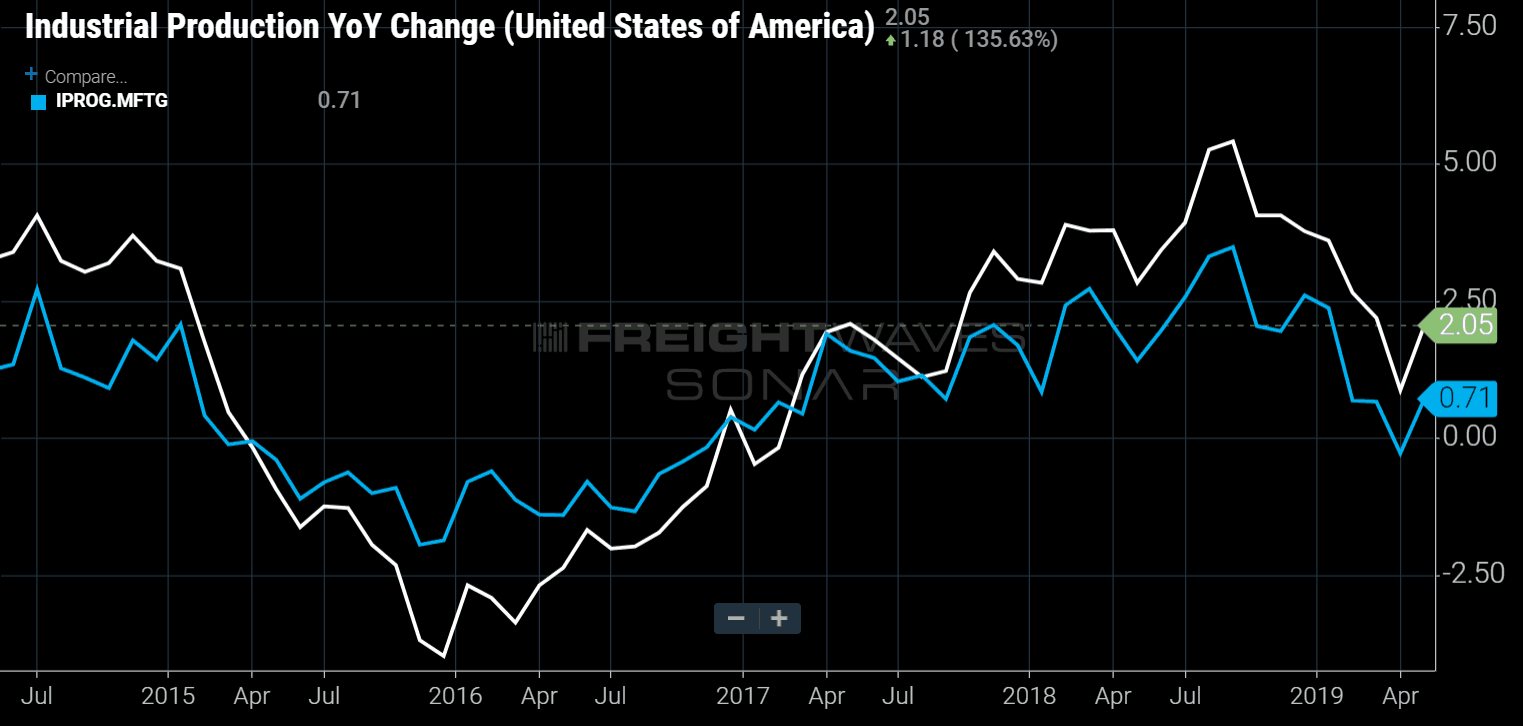

Industrial production and manufacturing

In the industrial sector, total production beat out consensus estimates by growing 0.4 percent in May from April’s levels. This marked the largest gain in production thus far in 2019 and pushed year-over-year growth (SONAR: IPROG.USA) up to 2.1 percent. Manufacturing industrial production, which makes up about three-fourths of the total, posted the first positive gain of 2019, rising 0.2 percent from April’s levels. This was enough to drive yearly growth (SONAR: IPROG.MFTG) back into positive territory at 0.7 percent

Survey data from the Institute of Supply Management’s manufacturing index remained in expansionary territory at 52.1 in May, by continued to trend downward, declining for the second straight month. Both the New Orders and Production components of the index have clearly downshifted in recent months and point to below-average growth in upcoming months.

Trend to watch: The manufacturing sector was set to take a major hit if the threatened tariffs against Mexico came to pass. The U.S. backed away from putting the escalating tariffs into place in June, but manufacturing orders and production numbers for June activity may contain some tariff-related volatility.

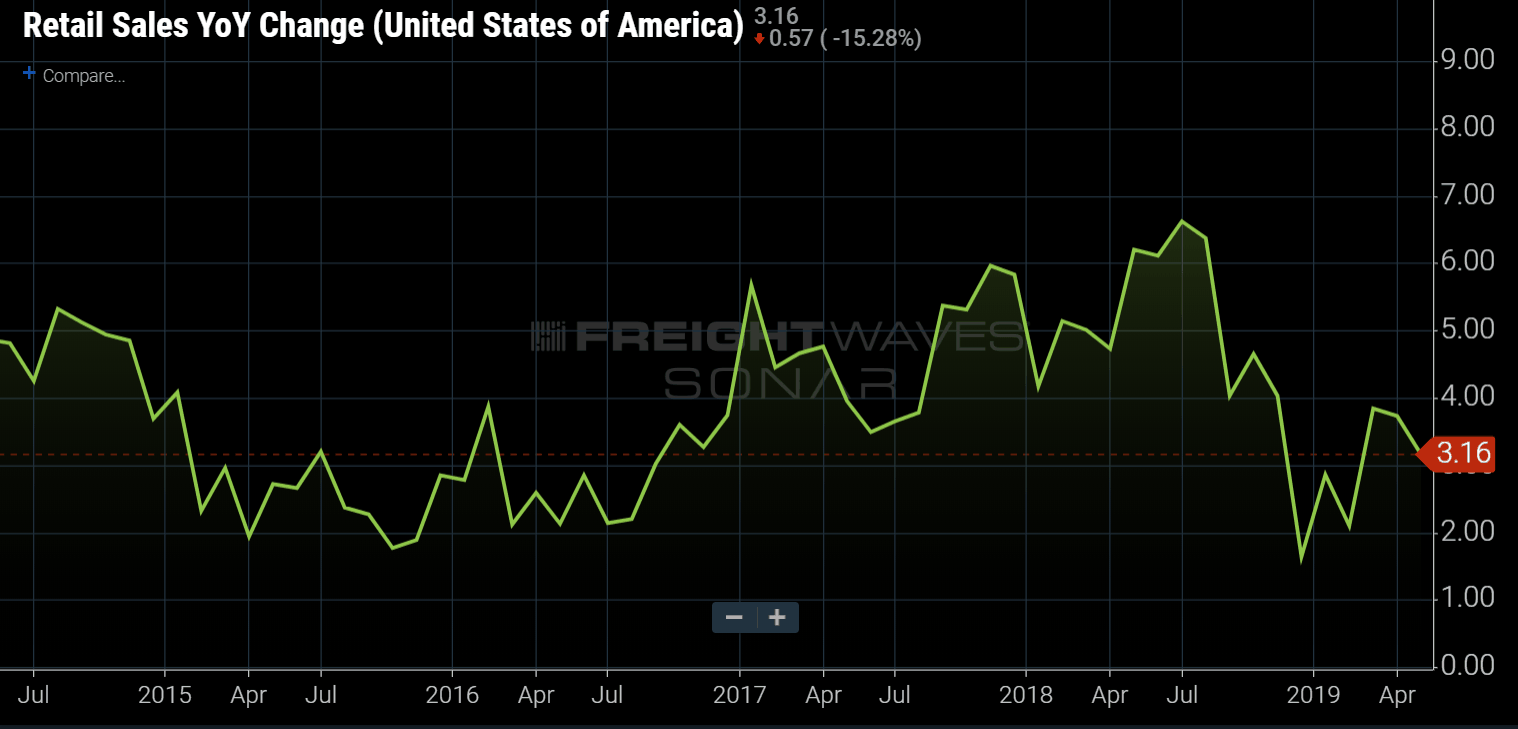

Retail and inventories

Retail sales growth also exceeded forecasts during the month, rising 0.5 percent month-over-month in May. In addition, April’s results were revised up showing a 0.3 percent gain after initial reports of a 0.2 percent decline. Year-over-year growth (SONAR: RESLG.USA) has settled in the 3-3.5 percent range over the past few months, and the broad-based gain in May suggests that consumer spending should be solid going forward.

On the inventory side, the total inventory/sales ratio rose to 1.39 in March, reversing the decline in the previous month. While much of the buildup in inventories in the fourth quarter was driven by tariff-related imports, uncertainty over trade policy has kept inventories high in the economy. Inventory building was a significant contributor to GDP growth in over the past few quarters, and recent data suggests that the inventory cycle has yet to turn

Trend to watch: The retail outlook largely depends on the strength of hiring, wages, and income in the economy. Job growth fell well short of expectations in May, and if the economy strings together a few months of softer employment gains, it could affect expectations for retail in the third and fourth quarter.

Labor markets

Job growth slowed considerably in May, as businesses added just 75,000 workers to payrolls during the month. In addition, results from both April and March were revised down by a combined 75,000 jobs, indicating that trends in hiring have not been quite as strong as previously thought. Despite the weak pace of hiring, the unemployment rate held constant at a near 50-year low of 3.6 percent in May. Wage growth also fell slightly below expectations during the month, as average hourly earnings climbed by just 0.2 percent from April’s levels. As a result, year-over-year growth in wages slipped to 3.1 percent in May, down from 3.2 percent in the previous month

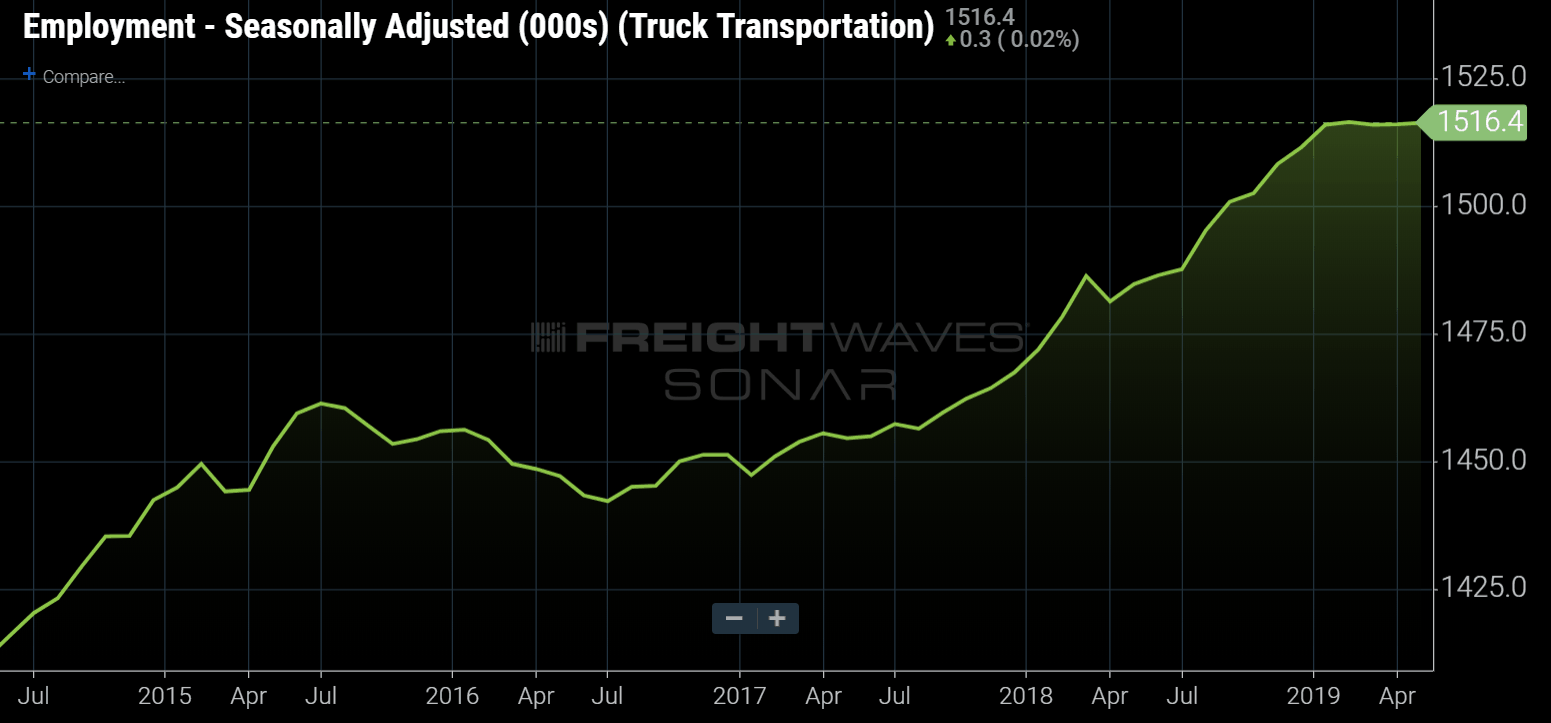

Within the trucking industry, hiring continued to sputter as payrolls rose by just 300 in May. Trucking employment (EMPS.TRUK) has essentially stalled since January of this year, as carriers have found themselves in a softer demand environment. Only 400 total payroll jobs have been added in the for-hire trucking industry over the last four months, after nearly 45,000 jobs were added in 2018.

Trend to watch: Hiring in the trucking industry has clearly flatlined since the start of the year, but has not yet turned south in any meaningful way. Rising rates and surging volume helped contribute to the surge in hiring throughout last year, and it remains to be seen whether the industry will begin to shed capacity now that demand has died down and rates are declining.

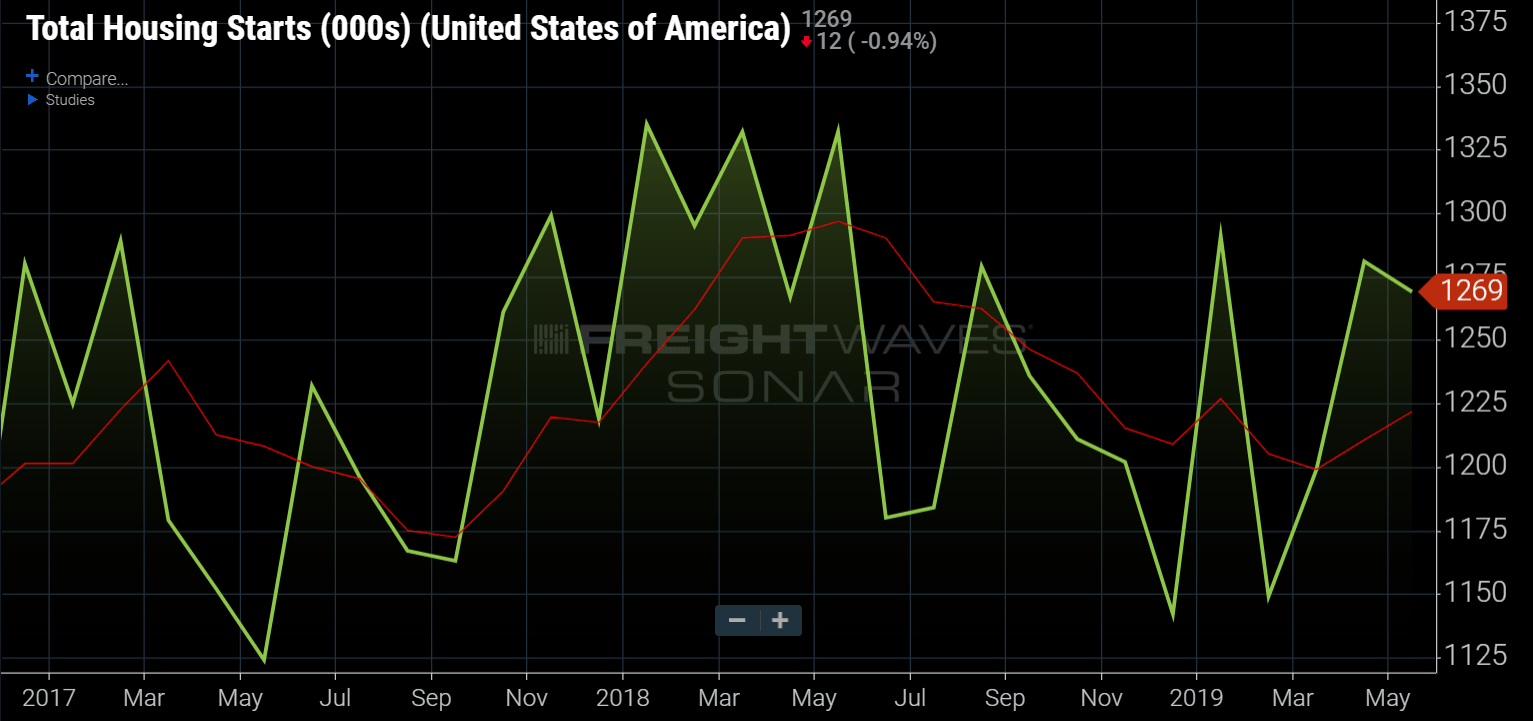

Housing and construction

May’s results were mixed for housing construction, as total housing starts (HOUS.USA) fell 0.9 percent from April’s levels to a 1,269,000 annualized rate. However, May’s weakness was offset by a significant upward revision to April data. New housing construction is still well below the pace seen at this point last year, but with the sizeable upward revision, trends have begun to turn upward in the construction sector.

On the demand side, new home sales fell sharply for the second consecutive month, falling 7.8 percent in May from April’s levels. New home sales are now negative year-over-year despite a significant increase in housing inventory available for sale. Existing home sales, on the other hand, performed much better during the month, rising 2.5 percent from April’s levels.

Trend to watch: Even with May’s declines, trends in both new home sales and housing starts are slowly beginning to trend upward. Solid job and income growth combined with easing mortgages rates should keep demand for home buying fairly solid in upcoming months, so the housing sector should make gradual improvements going forward.

International Trade

Advance reports on international trade show that the goods trade deficit widened for the second straight month in May, to $74.5 billion from $72.1 billion in the previous month. The wideninging trade deficit has negative implications for second quarter GDP growth in the economy, after net exports made the largest single contribution to the 3.1 percent pace of GDP growth during the first quarter.

Unlike last the previous month, data from May was more favorable for freight demand in the economy. Both exports and imports surged during the month, rising 3.1 percent and 3.7 percent, respectively. The strength in trade volume is likely temporary, however, as May’s results were helped by attempts to get goods in and out of the country after the U.S. and China reignited their trade conflict during the month. The fundamentals for trade growth are still fairly poor, and the presence of tariffs and other protectionist measures will only further harm international trade.

Trend to watch: June trade numbers will likely also contain some volatility due to the erratic nature of U.S. trade policy during the second quarter. Month-to-month swings aside, the protectionist trade policies have proven themselves to be bad for global trade volumes, and continued weakening in global growth should keep trade growth slow in upcoming quarters.

Ibrahiim Bayaan is FreightWaves’ Chief Economist. He writes regularly on all aspects of the economy and provides context with original research and analytics on freight market trends. Never miss his commentary by subscribing.

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now