The air cargo market is soaring this year and 2022 is looking even better. The International Air Transport Association on Monday estimated that cargo volume for airlines will grow 7.9% in 2021 compared to 2019 and demand will heat up to 13.2% above pre-pandemic levels next year.

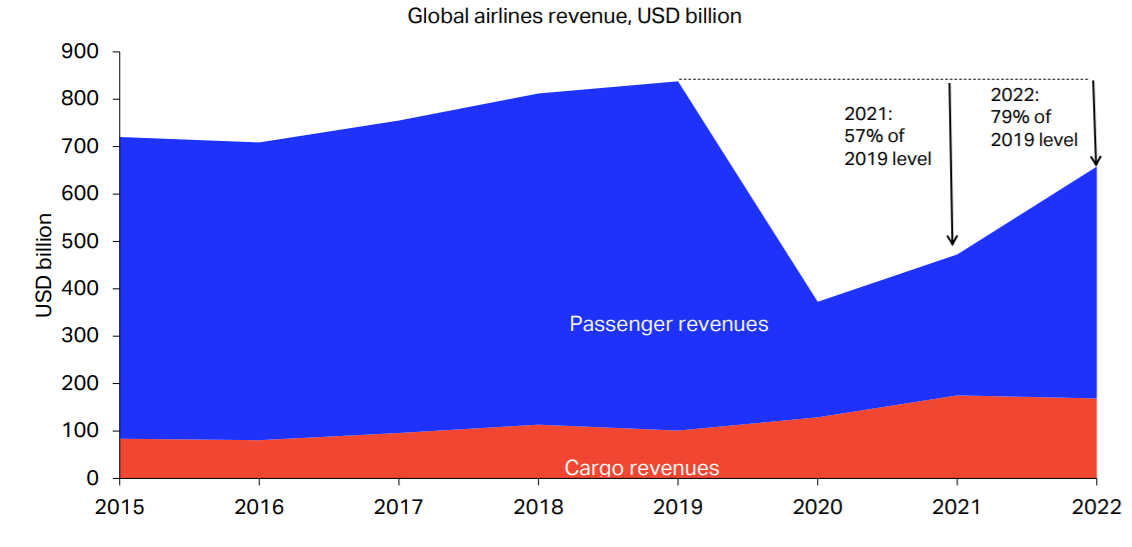

Cargo revenues are expected to reach a record $175 billion in 2021, an upward revision of $23 billion from April, and stay near that level at $169 billion in 2022 as cargo yields soften from 15% to 7% growth. Airlines generated $128 billion in cargo revenue last year, also a historic high.

Positive news on the airfreight side of the business was tempered by the trade association’s estimate that airlines will lose $51.8 billion this year because of reduced passenger travel associated with COVID and border restrictions. But the financial picture is much improved from last year’s $137.7 billion loss.

“We are past the deepest point of the crisis. While serious issues remain, the path to recovery is coming into view,” IATA Director General Willie Walsh said during the organization’s annual general meeting in Boston, according to a copy of his prepared remarks.

Global airfreight demand in 2020 decreased 10.6% year-over-year, the largest decline since IATA began monitoring cargo performance in 1990. The negative growth was primarily from the first half of the year when COVID shut down much of the global economy and crippled passenger travel. During the second half of the year, cargo volume came roaring back as companies tried to quickly restart production and sales.

By January, the air cargo market was in positive territory versus 2019 and has kept growing, driven by economic expansion, low inventories, e-commerce and diversion from overcrowded ocean shipping. The World Trade Organization on Monday revised up its forecast for global merchandise trade to 10.8% growth in 2021, with trade slowing to 4.7% — near the long-term trend — in 2022.

Demand during the first half of 2021 was 8% above the same period in 2019, representing the strongest growth since 2017. It’s possible final performance numbers will come in higher than IATA projections based on extreme market tightness and large shippers spending more on air transport to get goods in time for holiday shopping.

IATA’s metric for cargo volume is cargo ton-kilometers, which factors in the distance goods are carried. And the organization doesn’t track many all-cargo carriers, a sector that is currently thriving compared to passenger-dominated competitors.

But measured simply by weight, air cargo moved by airlines this year will reach 73 million tons, up from 68 million tons in 2019. Next year 76.3 million tons of merchandise, materials, equipment and food products will be shipped by air. More available capacity is the reason rates, and by extension revenue and yields, are expected to taper off despite the growth in volume.

Losing money

Most passenger airlines have survived the pandemic crisis, but they are not out of the financial woods yet. Net industry losses are expected to reach $51.8 billion this year, but shrink further to $11.6 billion next year, IATA projected.

During the three-year period ending in 2022, airlines will have lost a combined total of $201 billion, the airline group said. Carriers were forced to drastically cut costs, furlough workers, borrow heavily and, in many cases, rely on government bailouts worth about $110 billion, to keep operating. Cargo was one of the few revenue streams airlines had and sales reached a record level last year.

The strength in cargo sales isn’t enough to overcome the steep drop in passenger revenue, the core part of airlines’ business. Overall revenues in 2021 are expected to grow by 26.7% compared to last year, reaching $472 billion — on par with industry sales a dozen years ago. Further growth of 39.3% in 2022 will see industry revenues rise to $658 billion — similar to 2011 levels — IATA forecast. But costs will far exceed proceeds.

Airlines reduced overall expenses by 34% this year compared to 2019, but costs will only be 15% lower than pre-crisis levels in 2022 as companies expand operations and face higher jet fuel prices.

Last year, jet kerosene fell to $46.60 per barrel from $77 per barrel in 2019. Jet fuel has increased to an average of $74.50 this year and is expected to reach the 2019 level next year. Nonfuel unit costs rose 19% in 2020, as fixed costs had to be spread over a much smaller fleet. Unit costs will go down to 11% above the pre-crisis level, with added capacity reducing the gap to 2% in 2022, according to IATA.

Airline executives are meeting in Boston Monday and Tuesday to discuss the state of the industry and the road to recovery.

People have not lost their desire to travel but are being held back by “wildly inconsistent” COVID travel restrictions that are stalling the recovery of air transport, Walsh said.

“Travel restrictions bought governments time to respond in the early days of the pandemic. Nearly two years later, that rationale no longer exists. COVID-19 is present in all parts of the world. And there is little evidence to support ongoing blanket border restrictions and the economic havoc they create,” Walsh complained in his remarks.

Director General Willie Walsh addresses the International Air Transport Association general meeting on Monday. (Photo: IATA)

He repeated pleas for governments to reopen borders and simplify public health measures used to manage the risk of international travel.

“COVID-19 measures must not be allowed to become permanent. Measures must remain in place only for as long as they are needed — and not a day longer. As we do with many safety regulations, defined review periods are needed. Otherwise, as we said in the aftermath of 9/11, well-intentioned measures could remain in place long after they are necessary or have become technologically or scientifically obsolete,” said Walsh.

The U.S. reopening of borders in November to vaccinated foreign travelers is expected to increase passenger traffic.

Global passenger demand will only return to 40% of 2019 levels this year, rising to 61% in 2022. Passenger traffic is expected to reach 2.3 billion, growing to 3.4 billion in 2022 — about where demand stood in 2014 and far below the 4.5 billion travelers in 2019, according to IATA.

Domestic passenger markets, especially in the U.S., aren’t subject to as many travel restrictions and are leading the overall recovery. Demand this year and in 2022 will improve to 27% and 7% lower, respectively, than before the pandemic. International demand will continue to lag, down 78% and 56%, respectively, in 2021 and 2022.

The number of travelers dictates how many aircraft carriers will employ, which is important to companies with cargo because more than half of goods moving by air ride in the lower deck of passenger aircraft. The ongoing downturn in the passenger market has crimped overall cargo capacity by more than 12% despite an influx of several hundred freighter aircraft in the past year.

IATA said passenger capacity would increase faster than demand growth, reaching 50% of pre-crisis levels for 2021, with the average passenger load factor expected to be just 67.1% — a level not seen since 1994. In 2022, passenger capacity is expected to outpace demand at 67% of the 2019 benchmark, with average passenger load factors recovering to 75.1% — or where they were in 2005. In 2019, 82.6% of airline seats were filled.

North American carriers are expected to outperform other regions on the back of fast recovery of the U.S. domestic market. The opening of the U.S. market to vaccinated travelers in November will progress the recovery to international markets. The U.S. industry started to turn cash positive in the second quarter of 2021 and will be the only region in positive financial territory in 2022 with an expected $9.9 billion profit.

Airlines are highly leveraged because of public and private borrowing, and the return to profitability that will enable loan repayment will take time. IATA urged governments to provide wage support so the industry can retain critical skills until borders are fully reopened, as well as maintain waivers on meeting thresholds for takeoff/landing slot usage at busy airports.

Click here for more FreightWaves/American Shipper stories by Eric Kulisch.

RECOMMENDED READING:

Airline group says air cargo grew 7.7% in August

Pandemic taught passenger airlines lesson about the value of freight