Yesterday, Federal Reserve officials decided to add some additional stimulus into the economy, settling on a 25 basis point reduction in the federal funds rate at the conclusion of the July 30-31 Federal Open Market Committee (FOMC) meeting. This marks the first reduction in interest rates since 2008 and ends a monetary tightening cycle that began at the end of 2015. The effective federal funds rate will now fall between 2.0-2.25 percent, down from 2.25-2.5 percent.

The rate cut was largely expected headed into the FOMC meeting, as Fed officials have been hinting about a cut in interest rates to stave off a significant slowdown in growth in the economy. However, markets reacted unfavorably after Fed Chairman Jerome Powell’s press conference, in which he downplayed the idea of a prolonged cycle of interest rate decreases. Instead, Powell remarked, “We’re thinking of it as essentially in the nature of a mid-cycle adjustment to policy,” signaling that the Fed may not move interest rates down further unless economic conditions worsen.

How the federal funds rate affects the economy

The federal funds rate is the interest rate at which banks make overnight loans to other banks to maintain the reserve requirements set by the Federal Reserve. The FOMC sets a target range for the federal funds rate at the end of each of its eight meetings throughout the year, then conducts bond purchases or sales to keep the rate within range.

Most businesses and consumers cannot borrow at the federal funds rate, but other interest rates in the economy are based on the federal funds rate. Short-term and adjustable interest rates, such as those found with credit cards, short-term business loans and adjustable mortgages, typically follow the federal funds rate. The Fed then stimulates the economy by lowering the cost of borrowing for consumers and businesses as they respond to the lower federal funds rate.

Longer term rates, such as auto or home loans, generally move in the same direction as the federal funds rate, but are not as closely correlated. Because of the longer duration of loan terms, these rates respond as much to expectations about future rates as they do to movements in the short-term federal funds rate.

In addition, loose monetary policy affects growth by weakening the value of the dollar. As with long-term rates, however, the value of the dollar has as much to do with expectations for future policy as it does with current monetary policy moves. As a result, markets found themselves in the peculiar position of a stronger dollar and narrowing yield curve after the Fed rate cut, caused by Powell signaling that there may not need to be any more future cuts.

Why a rate decrease?

Generally speaking, the Federal Reserve conducts monetary policy to fulfill its dual mandate to maintain full employment in the economy and keep inflation moderate. It uses the target federal funds rate to help smooth out fluctuations in the economy, lowering the rate when the economy is weak and raising it to keep it from overheating and prevent inflation.

As the economy began gaining momentum at the end of 2017 through much of 2018, the Fed got more aggressive by tightening monetary policy, raising interest rates four times over the course of last year. In fact, throughout much of 2018, the Fed signaled that there would be additional rate increases in 2019.

Many analysts at the time of the final increase in December questioned whether the economy was growing at a fast enough pace to warrant another interest rate hike, especially given the generally subdued pace of inflation in the economy. This concern seems even more valid in hindsight given the recent annual revision of the gross domestic product (GDP), which showed the economy was not growing as fast as previously thought during the fourth quarter of 2018.

As disappointing data began to appear in early 2019, both in the U.S. and across much of the rest of the world, Fed officials began gradually backing away from their tightening stance. Slumping business investment, sluggish inflation and declining manufacturing activity served as signs that perhaps the Fed had already tightened too much. By the end of the first quarter, the Federal Reserve clearly signaled there would be no further rate increases in 2019, and after the FOMC’s June meeting, a rate decrease was all but assured.

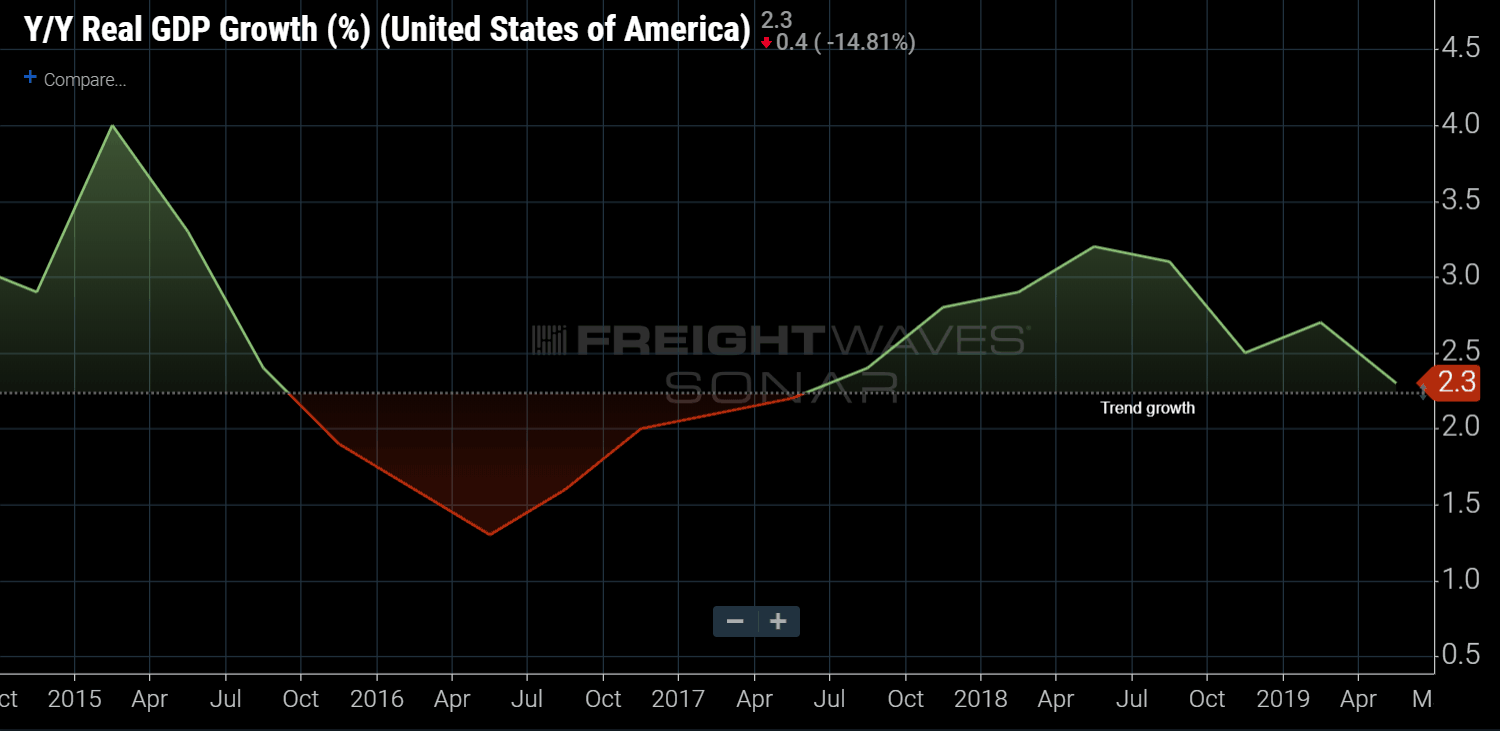

Fed officials have been very careful to mention that they are not necessarily concerned about the current state of the economy, however. For all of the difficulties in the economy at the start of the year, GDP still grew 2.3 percent year-over-year in the second quarter. That is quite a bit slower than the 3.2 percent pace in the middle of last year, but still right around trend growth in the economy. In addition, positive surprises for job growth, the retail sector and manufacturing over the past month suggest that the economy may have been turning around already before any Fed action.

The minutes from the June FOMC meeting made it clear that the prevailing feeling among members was that global growth and lingering low inflation were the chief concerns facing the U.S. economy. As such, the decrease in rates is less about jumpstarting the economy than it is about trying to provide some additional cushion against future risks to growth.

What does this mean for freight markets and carriers?

Freight markets are affected by a rate cut in a few different ways. First, freight activity is derived demand; the amount of transportation services that shippers demand is directly affected by the demand for the goods that shippers sell. The rate decrease provides a boost to consumer and business spending. This, in turn, should help drive additional manufacturing, construction and import activity.

Carriers of course will begin to notice modestly lower interest rates throughout the economy. Financing terms on truck and equipment purchases should come down slightly in response to the interest rate cut. In addition, looser monetary policy generally makes it easier for smaller, less credit-worthy carriers to receive loans from banks.

Because the central bank signaled that this rate cut is likely just a minor adjustment and not part of a longer, rate-cutting cycle, the impact to overall activity will probably be minimal. A quarter-point rate decrease provides some boost to the economy at the margins, but any pronounced reacceleration in growth is going to have to come from somewhere else in the economy.

Ibrahiim Bayaan is FreightWaves’ Chief Economist. He writes regularly on all aspects of the economy and provides context with original research and analytics on freight market trends. Never miss his commentary by subscribing.