Trailer-as-a-service partnership

Trailer pool services are gaining adoption. Wabash, a major manufacturer of equipment, recently announced a partnership with Phoenix-based freight brokerage FreightVana to supply the company with its trailer-as-a-service (TaaS) platform. The platform will provide FreightVana customers with trailer pool services as part of the power-only offering known as FreightVana X.

This comes as more shippers seek trailer pools to provide greater flexibility for shipping loads and reduce the number of scheduled live loads from their facilities. Traditionally, only the largest fleets could afford the equipment to position trailers at shipper locations, which caused smaller carriers the added headache of dealing with live loading or unloading appointments that can last hours and reduce precious driving time.

This partnership by Wabash comes as the trailer business model is changing. FreightWaves’ Alan Adler writes, “Long known for boom-and-bust periods, trailer manufacturing is experiencing less cyclicality. One change is the growth of trailer pools to address resilient e-commerce demand. Even as consumer spending pulls back, commercial vehicle miles are replacing passenger vehicle miles because of same- and next-day delivery.”

FreightVana is unique in that it’s one of the few brokerages that offer a power-only option that gives access to trailer pools for smaller carriers. Regarding the partnership and benefits for FreightVana, Fleet Owner noted, “FreightVana’s trailer pools enable small trucking companies, who would otherwise be incapable of supporting many large shippers’ trailer requirements, an opportunity to build networks of consistent freight, typically dominated by only the largest for-hire carriers in the country.”

This will be an interesting development to watch, as access to trailer pools and greater preloaded freight will allow smaller carriers greater savings due to less lost revenue from excessive dwell time. Reducing dwell time and speeding up trailer velocity should benefit both shippers who seek to turn idle trailers and carriers that are willing to haul rather than wait for a live load.

Large carrier Q2 earnings boon

Buoyed by high contract rates and less spot market exposure, large carriers are reporting an earnings boon. Contracted rates are normally negotiated in a byzantine RFP process and can take anywhere from weeks to months to conclude, often lasting around a year. The duration of these contracted rates provides large carriers not only predictable freight volumes but also a buffer on rates during freight market downturns. This is in part due to the lag time between the decline in spot market rates and shippers requesting contract rate renegotiations.

Now that earnings season has begun, there will be increased scrutiny on trucking and logistics C-suite comments outlining the outlook for the rest of the year. Below are a few highlights so far from the earnings season.

Heartland CEO Mike Gerdin noted in the company’s earnings report, “While the current levels are down compared against the unprecedented levels experienced in the later months of 2021, we continue to have significantly more opportunities to haul freight than we are able to cover with our existing fleet and available drivers.”

J.B. Hunt CCO Shelley Simpson noted in the company’s earnings report that, “We’re having a seasonally normal July. We do think that there will be a peak [season], to what extent we’re still not sure. We feel confident in the different areas of our businesses and how we’re having conversations with our customers.”

Adam Miller, CFO at Knight-Swift Transportation, noted in the company’s earnings call, “Freight demand followed normal seasonal trends but was generally strong throughout the quarter. As we make more commitments, we are seeing higher tender acceptance levels and fewer noncontract opportunities. As spot rates have declined, we have increased commitment levels with our customers and have reduced our exposure to the spot market. We are seeing strong demand from our customers to secure trailer pool capacity through our truckload and logistics segments.”

FreightWaves’ Todd Maiden noted that on Knight-Swift’s earnings call, Dave Jackson, president and CEO. stated this downturn is unique, writing, “He said the supply side is different this cycle because in past downturns small carriers had the benefit of low fuel prices, and falling used equipment prices allowed them to inexpensively jump into a newer truck and avoid the maintenance expenses associated with running older equipment. Further, prior to the electronic logging device mandate, carriers could run extra miles to make up for revenue shortfalls.”

Jackson added on the call, “One thing we do know, that has been consistent from one cycle to the next, is when credit dries up, that brings religion to small carriers in terms of what they do to grow or refresh. And that process is well underway already.”

Whether or not small carriers can remain in the market profitably will be the theme to watch over the next six months, as inflation, fuel prices and consumer trends continue to have a major impact on the freight market and trucking business environment.

Market update: Recession or not a recession, that is the question

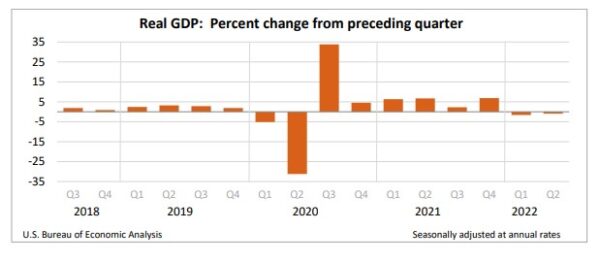

On Thursday the Commerce Department released its Q2 GDP data, reporting that the economy contracted at a seasonally adjusted annual rate of 0.9%. This follows a decline of 1.6% from Q1 data from the first three months of 2022.

If you Google “recession definition,” the Oxford Languages dictionary notes, “a period of temporary economic decline during which trade and industrial activity are reduced, generally identified by a fall in GDP in two successive quarters.”

The part that has some economists debating this release stems from economic decline and a fall in GDP for two quarters. While we are in a technical recession by definition, Harriet Torry with The Wall Street Journal wrote, “The official arbiter of recessions in the U.S. is the National Bureau of Economic Research, which defines one as a significant decline in economic activity, spread across the economy for more than a few months. Its Business Cycle Dating Committee considers factors including employment, output, retail sales and household income — and it usually doesn’t make a recession determination until long after the fact.”

Sal Guatiere, senior economist at BMO Capital markets, told The Associated Press, “The back-to-back contraction of GDP will feed the debate about whether the U.S. is in, or soon headed for, a recession,” adding, “The fact that the economy created 2.7 million payrolls in the first half of the year would seem to argue against an official recession call for now.” However, Guatiere notes that rising borrowing costs, tightening financial conditions and four-decade-high inflation are creating major headwinds for the economy.

Unfortunately, economic analysis is tediously slow, and by the time the dust settles we may know if it was in fact a recession months after the fact. In the meantime, buckle up and get some popcorn out.

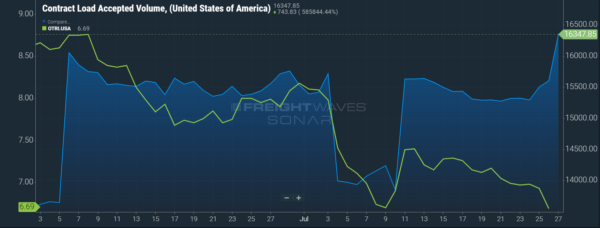

FreightWaves’ SONAR spotlight: Contract freight is king as rejections continue to fall.

Summary: The amount of contracted freight compared to the Outbound Tender Reject Index gives a clear idea where freight is headed. CLAV has continued rising while OTRI has trended downward — that indicates that carriers are pushing capacity back to the contracted side. That information aligns with what we already know — contracted rates are on par with or higher than spot rates in some markets. When the market gets good for spot rates, watch for contracted volumes to drop or stagnate and outbound tender rejections to increase, something unlikely to be seen for the next few weeks.

The Routing Guide: Links from around the web

ATRI launches survey on driver-facing cameras (Fleet Owner)

C.H. Robinson surpasses profitability expectations (FreightWaves)

Carriers unable to pay drivers, buy fuel after CoreFund Capital closes (FreightWaves)

We might be having the completely wrong conversation about truck parking (FreightWaves)

Subscribe to the Loaded and Rolling newsletter here

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now