Crude and product tankers have garnered all the headlines in 2020, and rightfully so, but liquefied petroleum gas (LPG) shipping could offer a clearer-cut and more binary bet on the coronavirus recovery.

Higher oil production and refining would create more propane and butane as byproducts, filling more LPG carrier cargo holds. Unlike crude and product tankers, LPG carriers face no near-term headwinds due to the unwinding of floating storage.

LPG shipping companies boast high spot-market exposure and volatility. Rates for very large gas carriers (VLGCs; LPG carriers with a capacity of 84,000 cubic meters) are much more volatile than rates for product carriers.

According to data from Clarksons Platou Securities, VLGC day rates rose from around $10,000 in February 2019 to $66,000 in June, then fell to $40,000 by August, rose back to $62,000 in November 2019, and sank back down to $20,800 as of Wednesday.

The stock of the largest U.S.-listed VLGC owner, Dorian LPG (NYSE: LPG) has seen similarly big swings. Between January and December 2019, its share price tripled. Since that peak, it has fallen 40%. On Wednesday, after it released its latest quarterly earnings, its stock jumped 14%.

Coronavirus curbs export cargoes

Connecticut-based Dorian LPG reported net income of $29.4 million for the quarter of its fiscal year ending March 31, 2020, compared to $16 million during the same period last year. Adjusted earnings of 81 cents per share came in well above the consensus forecast for 63 cents per share.

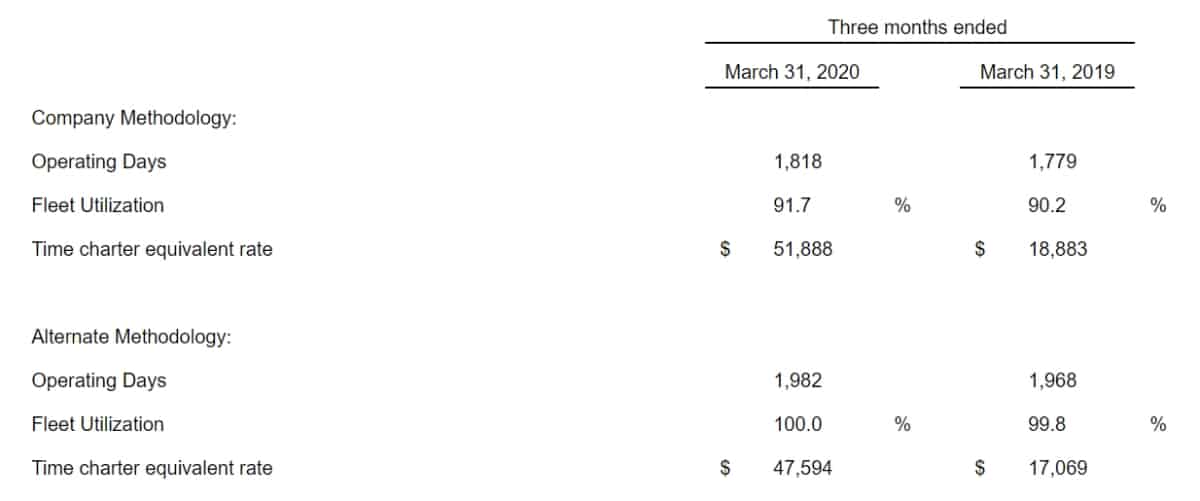

Rates averaged $51,888 per day in the latest quarter, up 175% year-on-year. For the quarter that will end on June 30, Dorian has 75% of its days booked at nearly $50,000 per day, more than double current spot rates.

During the conference call with analysts, Dorian LPG (USA) CEO John Lycouris pointed out that volumes have been strong until this month. First-quarter global volumes of seaborne LPG were up 3.6% year-on-year. Over 50 VLGCs were loaded per month in the U.S. in March and April, and there were 70 loadings in the Middle East Gulf in April, the highest monthly tally since June 2019. Middle East Gulf loadings in May dropped to 54 from 60 in May 2019.

The coronavirus crisis affects VLGC seaborne volumes from both the cargo supply and demand side. On the supply side, OPEC cuts and the shut-ins of U.S. production due to low pricing translate into less LPG available for export, although LPG drawn from stockpiles should temporarily offset production fallout.

According to Dorian LPG Chief Commercial Officer Tim Hansen, “Of course we’re seeing these [crude production] cuts eating into LPG volumes out of the U.S., although it’s too early to say how much and we have not seen an [export cargo] cancellation yet.” Lycouris confirmed that production cuts were also reducing loadings in the Middle East.

Demand-side fallout

On the demand side, about half of LPG is consumed by residential customers for heating and cooking, the other half by industrial propane dehydrogenation (PDH) plants, largely in Asia, that produce propylene for plastics manufacturing. PDH plants use either propane carried by VLGCs or naphtha carried by product tankers as a feedstock, depending on price.

Residential demand for LPG, which falls in the “essentials” category, is likely to remain resilient. However, on the industrial side of the equation, lower crude pricing due to the coronavirus has equated to lower naphtha pricing, making naphtha more attractive to PDH plants than LPG.

During the conference call on Monday of Oslo-listed BW LPG, that company’s executive vice president of commercial operations, Neils Rigault, commented that “obviously, with naphtha prices as low as they are, [Asian buyers] will probably switch back to naphtha.”

In a coronavirus recovery scenario, the price of oil, and thus naphtha, would snap back up — a plus for LPG industrial demand. To some extent, this has already begun. According to Lycouris, “With crude oil prices recovering, we find the propane-to-naphtha spread starting to turn in favor of LPG.”

Uncertain outlook

A number of public shipping company executives have maintained on conference calls that the second half looks better because the worst of the coronavirus has probably passed.

Dorian LPG founder and CEO John Hadjipateras was more circumspect, openly acknowledging the inherent uncertainty.

“We have read many forecasts [on LPG shipping] ranging from a little to very pessimistic. They’re predominantly based on assumptions about a decline in U.S. shale production available for export,” he said. “But will economic activity bounce or crawl back? Will there be permanent demand destruction?”

His answer: “I do not pretend to know which forecast to believe — much less to make them.” Click for more FreightWaves/American Shipper articles by Greg Miller

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now