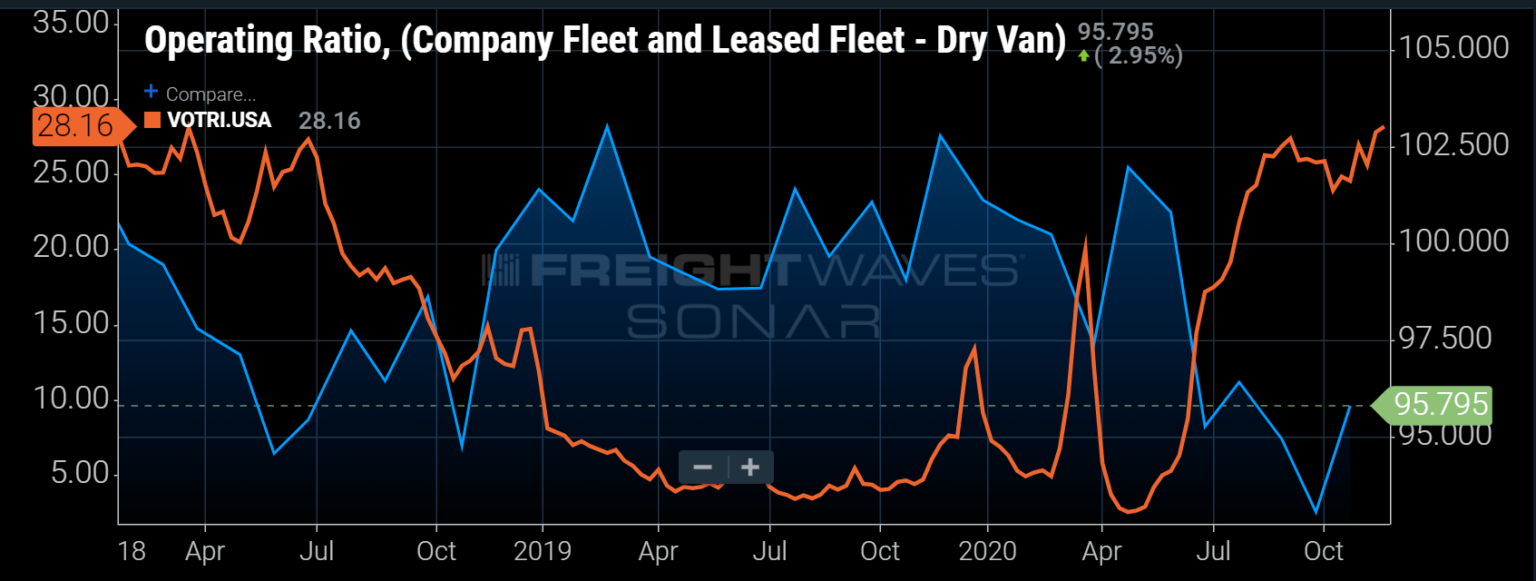

The average dry van carrier operating ratio (OR) for Truckload Carriers Association (TCA) members dipped to a multiyear low in September, falling below 94% for the first time since late 2015. Operating ratio is the ratio of operating expense to operating revenue — lower values indicate a more profitable operation. The boundary was crossed as tender rejection rates — the rate at which carriers turn down requests for capacity from their customers — for van loads were near record highs as carriers were only able to cover about three in every four loads.

From 2015 to 2019, the average OR for van carriers in the TCA program was 97.7%, meaning for every $100 in sales, they spent $97.70 moving the freight. Through the first half of 2020, carrier ORs averaged 99.4%. From July through October, that figure dropped to 95%.

The trucking business relies heavily on efficient operations and consistent volumes to ensure profitability — the latter being difficult to attain most of the time. High amounts of competition thanks in part to low barriers to entry ensure that carriers cannot expand pricing to create much of a cushion when demand wanes.

The COVID-19 pandemic arrived on the heels of a stable and oversupplied freight market, which was reflected in the relatively low tender rejection rates for dry van loads. Van tender rejection rates averaged 5-6% during the seasonally slow period from January through February. Dry van carrier ORs had been above 100 since November.

Once the pandemic hit the U.S. in early March, volumes rose suddenly and somewhat unexpectedly thanks to panic-induced purchases of food and beverage and household items, creating numerous network imbalances and pushing tender rejection rates above 19% for the first time since 2018. This was short lived as the economy shuttered for a month.

The short-term boost helped carriers achieve the highest level of operational profitability in nearly 18 months, dropping ORs to 97%. This figure jumped back over 100 in April and May but has been below 97% since June as demand for goods has replaced many services with people staying at home.

While this all may seem like good news for carriers, it is concerning that one of the most historically tight freight markets only produces 5% to 7% operating margins. Demand appears to look strong for the near future and rate increases are all but inevitable for 2021, but will carriers see a repeat of a 2019-style year if freight volumes recede to more manageable levels as they typically do?

A few things may help carriers retain some of the gains from 2020 — the first is driver recruitment. While it was easy enough in 2018 to place an order for Class 8 trucks and convince new drivers to enter the space, 2020 has seen driver schools close or only produce half-full classes over the past several months. This will keep capacity growth at bay well into next year. The offset of this may be increased driver cost, however, as carriers struggle to retain their current driver base.

Rate volatility may be the biggest factor that will enable carriers to keep some of momentum into next year. Shippers have now experienced extreme capacity shifts in three out of the past four years. A soft 2016 led to depressed rates and trucking exits as demand ramped through the second half of 2017 into 2018. Capacity flooded the market in 2019 just in time for demand to fall and push rates back down leading into 2020.

The rate pendulum has not swung this wildly in some time and shippers need consistency from their carriers now more than ever as supply chains are being redesigned. Having reliable sourcing and transportation solutions are higher priorities as companies have learned nothing is given, even in a nearly purely competitive trucking market.