After racking up numerous quarters of record financial performances, truckload carriers are acknowledging the historic strength of the recent freight cycle has finally petered out. Sentiment from some of the nation’s largest fleets has turned considerably more tepid around freight demand and the outlook for 2023.

Carriers were largely optimistic heading into peak season, calling for a normal stretch of stocking up ahead of the holidays, albeit not as robust as the last two years. However, as September progressed demand cooled and capacity continued to loosen. Morgan Stanley (NYSE: MS) analyst Ravi Shanker summed up the about-face best in a note to clients discussing Knight-Swift Transportation’s (NYSE: KNX) third-quarter results.

“Barely a month since the Laguna conference where KNX and virtually all their Transportation peers sent the collective message of ‘sequential slowing but things are fine,’ the KNX cuts + JBHT’s commentary … are a meaningful step down in fundamentals. This should serve as a warning to any other cohorts in Transports that are still not pricing in a downturn.”

Knight-Swift missed consensus expectations and lowered its outlook for the fourth quarter.

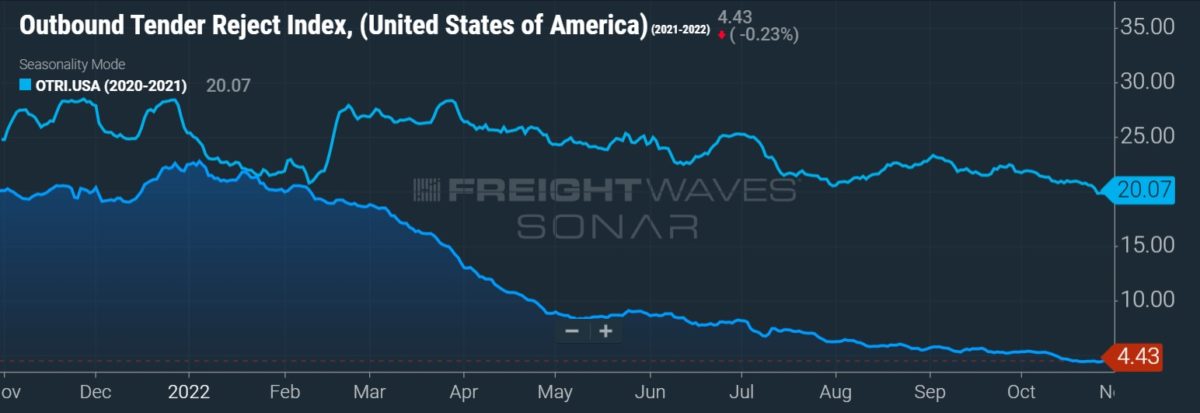

The last 2 weeks of September unraveled

A deceleration in fundamentals during late September was notable in responses to a monthly supply chain survey.

The Logistics Managers’ Index showed respondents said transportation capacity loosened and pricing fell at an accelerated pace during the last 15 days of the month. The diffusion index, wherein a reading above 50 indicates expansion while one below 50 indicates contraction, showed the view on capacity was 9.2 percentage points higher at 76.9 with pricing down 14 points to 36.8 in the back half of the month.

“It’s rare that you go into a fourth quarter and not see some type of seasonal uplift and projects and spot opportunities,” said Knight-Swift CFO Adam Miller on a call with analysts discussing the third quarter. “Especially with companies of our scale, we typically get some of these large, kind of difficult projects to handle and they typically pay a premium; … none of that stuff materialized.”

Freight broker Landstar System (NASDAQ: LSTR) saw loads hauled by truck decline as the third quarter progressed. Total truck loads were up 5% year over year (y/y) in July, flat in August and down 1% in September. October loads were down y/y by a mid-single-digit percentage as of the Oct. 20 update.

“Everybody’s [indicating a] flat to a soft, muted peak season,” Landstar President and CEO Jim Gattoni said on a conference call discussing quarterly results and fourth-quarter expectations. “Since our July call, I would say things have clearly softened up compared to the anticipation of a better peak season.”

The company reported third-quarter results that were in line with analysts’ expectations and its fourth-quarter guidance came in better than expected.

Schneider National (NYSE: SNDR) said contractual volumes were steady but tenders of recently awarded freight were light of plan on its Q3 call. Freight allocations from shippers that concluded in the second quarter have seen fulfillment of those orders below historical averages.

Management chalked it up to the reality of being on the downside of a record demand cycle. It also said several shippers are dealing with elevated inventories and that many had pulled forward delivery of merchandise to avoid the delays seen during last year’s peak season.

“So far in October, we are experiencing sequential volume improvement but muted seasonal peak demand and below historical average of special project programs,” said CEO and President Mark Rourke.

Schneider’s TL segment recorded 300 basis points of y/y margin deterioration, posting an 85.4% operating ratio for the quarter. However, lower gains on sale compared to the year-ago period accounted for all of the decline and then some.

Knight-Swift misses, lowers expectations as costs outpace yields

Knight-Swift’s adjusted TL OR deteriorated 400 bps y/y to 81.8% in the third quarter. Higher costs associated with drivers, equipment maintenance and insurance were cited as the reasons. Revenue per tractor was up slightly as revenue per loaded mile (excluding fuel) increased 8% and loaded miles per tractor declined 6%.

“This was the first quarter in quite a while where the rate [per loaded mile] was only up single digits and clearly our costs are up more than single digits on a y/y basis,” President and CEO Dave Jackson said.

A lack of specialty and project freight suppressed the yield metric in the quarter compared to costs per loaded mile, which were 13% higher y/y on an adjusted basis. The margin step-down occurred even though contractual rates didn’t move lower y/y in the period.

Management’s guidance for the fourth quarter calls for rates to turn negative y/y given fewer noncontractual opportunities. “That is the reality that we are facing as truckload carriers going into the bid season,” Jackson added.

Cost cutting already in progress

As carriers find themselves on the wrong side of the cycle, commentary has become a bit more defensive. Large carriers will continue to pursue growth initiatives both organically and through M&A but with a more measured approach to cost management.

“Further evidence has presented itself over the course of the quarter that requires an increased level of caution and awareness on broader demand trends and economic activity,” said J.B. Hunt Transport Services (NASDAQ: JBHT) CEO John Roberts on its quarterly call.

The company beat analysts’ expectations in the third quarter, with the biggest operating income gains coming from its intermodal and dedicated segments. However, a sobering, post-pandemic backdrop for demand in the near term has it pursuing cost reductions in all five of its segments. Brokerage and final mile, which have seen significant investment in recent years, were mentioned as areas of focus.

“Our capital allocation process will continue to follow the exact same way that we have done over the last five years,” President Shelley Simpson said. “We’ve been very offensive over the last year or two, making sure that we are prepared and ready for our customers. This is going to give us a chance to take a little bit more of a breath and be a little more structured, disciplined, staying in tune and in line with what the market is doing.”

Knight-Swift has been tempering costs as demand has faded as well.

“Our goal is to reduce our empty mile percentage to allow us to really run more miles with our seated trucks to help offset any of the rate pressure we may feel,” Miller said. “And then certainly, I think you know our culture, we’ll become very cost disciplined. We already are, but we’ll dig deeper into our organization and most likely make progress where we can from a cost standpoint.”

Landstar bracing for H1 comps

Landstar’s independent contractor, or business capacity owner (BCO), network tends to withstand market swings better than the broader spot market. BCO loads are often specialized in nature and usually have trailers attached to the transaction, which make the operations a little more contract-like.

“They tend to not kick you out as fast if you’re providing trailers, and so you kind of can lock in a little longer on those rates and hold them a little more steady,” Gattoni said.

Landstar’s BCO yield metrics have been less volatile, down only 17% since the February peak compared to general spot rate declines of more than 40% (excluding fluctuations in fuel) over the same time. BCO revenue per mile (excluding fuel) for dry van loads was up 2% y/y in July, flat in August but down 4% y/y in September.

While BCOs have seen firmer conditions, Gattoni said it won’t hold. “You’ll get pressure there. There’s no question. It just takes a little while longer.”

Landstar is forecasting loads to decline between 2% and 4% y/y in the fourth quarter, which has one extra operating week compared to 2021, with truck revenue per load forecast to drop between 5% and 7% y/y.

The falloff gets more severe in 2023. The first quarter of 2022 was Landstar’s best ever. Revenue per load is off 15% to 20% since then and normal seasonality implies another 5% to 6% sequential decline from the fourth quarter.

“I think it’s going to be an extremely tough first half next year, just on the comparisons and the direction of the economy,” Gattoni said.

More FreightWaves articles by Todd Maiden

- Saia says demand lost momentum as Q3 advanced

- XPO closes a chapter, Q3 beat with mixed Q4 guide

- Ruan acquires Michigan-based dedicated carrier NTB

Carrier Update

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now