(Updated with brief comments from CEO on earnings call)

The stronger freight and trucking market can be clearly seen in the fourth-quarter earnings of Canadian-based bank BMO, the former Bank of Montreal, which is a significant lender to that sector.

Given the size and significance to the trucking community, the quarterly data of BMO is an indication of the health of the industry. Stronger markets result in fewer write-offs and impairments; weaker markets do the opposite.

BMO is the only known key lender to the trucking industry to disclose such specific data. By that standard, the BMO data for the fourth quarter that ended Oct. 31 clearly showed that borrowers are staying more current with their payments than at any time this year.

On the company’s earnings call with analysts, CEO Darryl White made one brief reference to the results in the transportation division. “Within our U.S. commercial segment, we also saw a decline in provisions for transportation finance as the tighter truck capacity and improved spot rates resulted in improvements across all delinquency categories,” he said.

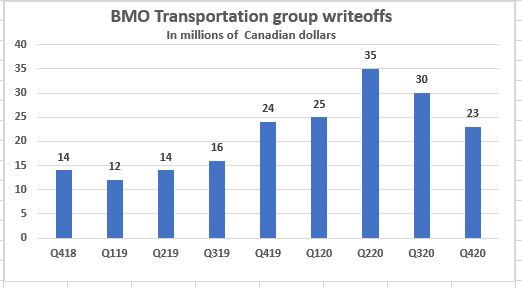

Among the key data points:

— Write-offs in the transportation sector were down. A bank takes a write-off when it has concluded there is no reasonable chance for recovering its loans. In the fourth quarter, write-offs were CA$23 million — or U.S. $17.7 million at a conversion rate of 1 Canadian dollar equivalent to U.S. 77 cents. That write-off figure is down from the CA$30 million in the third quarter and CA$35 million in the second quarter. A year ago, write-offs were CA$24 million.

— Gross impaired loans were down significantly, to CA$144 million. That shows a sharp decline from the CA$189 million posted in the second and third quarters and is less than the CA$149 million posted in the fourth quarter of 2019. Net impaired loans are calculated by taking gross impaired loans and subtracting allowances for credit losses. Allowance for credit losses is defined as “an estimate of the debt that a company is unlikely to recover.” That figure also is down for BMO, dropping to CA$32 million in the quarter. That is down from CA$36 million in the third quarter but was at CA$30 million last year.

— The bank’s book of transportation business, defined as gross loans and acceptances, was essentially flat at CA$12.95 billion. But it is smaller than the second-quarter figure of CA$13.38 billion, a number that was inflated by clients pulling down their lines of credit as a safety net at the start of the pandemic. The reduction might be seen as a sign that some of the borrowers who took that money earlier in the year have been paying it back given the healthier market. But at CA$12.95 billion, it is still bigger than the CA$12.42 billion of the fourth quarter of last year.

— Provisions for credit losses in BMO’s transportation sector for the quarter fell to CA$18 million in the quarter. That is down sharply from the CA$31 million in the third quarter and CA$38 million in the second quarter, a period that included the disastrous freight market of April. In the fourth quarter of 2019, provisions for credit losses were CA$23 million. The category of provisions for credit losses is defined by Investopedia as covering “expected losses from delinquent and bad debt or other credit that is likely to default or become unrecoverable.”

More articles by John Kingston

BMO’s Q3 suggests transportation sector’s finances stabilized

BMO, big trucking industry lender, eyes steps to help borrowers

BMO bank takes significant charges in truck lending transportation