Instead of discussing the current CPG news and freight data per my usual, for today’s newsletter I highlight the CPG industry trends I expect to see in 2022.

Trend No. 1: Consumer behavior will change in response to rising prices, at least among lower-income consumers. The topic of the hour is inflation, which hit a 39-year high in November, up 6.8% year-over-year. As tight as the labor market has been, wages are rising less than inflation, up just under 5%. So workers are losing ground to inflation and, of course, it’s a worse situation for retirees and people on a fixed income. While most recent sales data shows that consumers are still spending freely, consumer sentiment surveys reveal meaningful concern over rising price levels, which could prove to be a leading indicator for upcoming consumer retrenchment. Barring any unforeseen changes, consumer behavior is likely to become even more bifurcated between those focused on the stock market and those focused on grocery prices.

Trend No. 2: Sorry, shoppers — CPG companies will get even more aggressive with price increases in 2022. Most CPG companies experienced pressure on their gross margins in the past year due to increases in ingredient costs, packaging costs, labor costs and freight costs. In most cases, those costs rose more quickly than CPG companies could pass along price increases through their retail channels. In some cases, the margin pressure was a couple hundred basis points, and in other cases, it was several hundred basis points. Whatever the magnitude, CPG companies are looking to make their margins whole next year.

Trend No. 3: Private-label brands should regain market share from national brands. That would be a reversal of a pandemic-era trend, but I believe a logical one considering that many consumers will be forced to trade down to less expensive items as prices rise. On that topic, TreeHouse Foods makes a compelling case showing that states that rolled back enhanced unemployment benefits relatively early experienced an earlier uptick in sales of private-label brands. I believe that could be a harbinger of 2022 as household savings related to pandemic-era stimulus packages are depleted.

Trend No. 4: The Biden administration will point to the CPG industry to deflect blame for rising prices. The problem with calling inflation “transitory” is that it’s harder to continue using the term the longer it persists. So far, we have seen the Biden administration issue an executive order to promote competition, accuse the meat processing industry of profiteering and the Federal Trade Commission ordered nine companies to turn over supply chain data (some of which were CPGs or their retail partners). I expect 2022 to be a long year of finger-pointing ahead of the midterm elections.

Trend No. 5: CPG companies will find innovative ways to address labor shortages. The big takeaway from Thursday’s Tyson investor conference is that the company is investing heavily in automation to reduce the need for workers in difficult-to-fill positions. That implies that the meat processing giant expects the labor shortage to be long-lived. In the interim, Tyson has worked with employees on attendance sticking points, such as arranging transportation and child care.

Trend No. 6: CPG companies will continue to diversify into higher-growth and higher-margin segments. The preferred segments include health and pet food, due to favorable demographics, growth rates and compatibility with direct-to-consumer e-commerce.

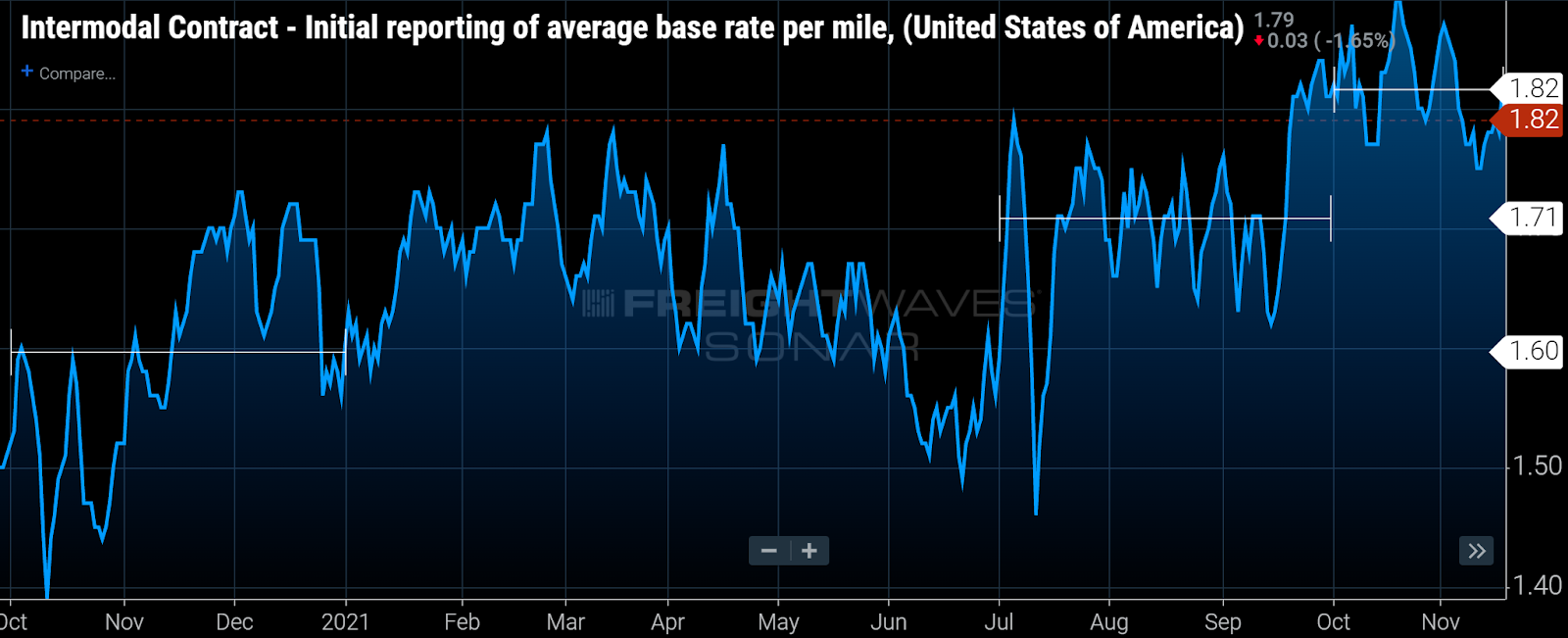

Trend No. 7: Freight costs will continue to rise, at least in the first half of 2022. Contract freight rates rose steadily throughout 2021 with contract freight rates higher in each quarter than they were in the prior quarter. As a result, shippers that are moving freight under contracts last repriced in early 2021 will be in for a sharp increase when those contracts are repriced early next year.

Trend No. 8: Capital will continue to flow into alternative food companies. I don’t expect the recent disappointing results posted by Beyond Meat to dampen investors’ appetite for alternative foods given the interest in ESG investing and the potential for nascent technologies to disrupt the food industry. In addition to plant-based meat alternatives, the most promising technologies include vertical farming (which Whole Foods called its top food trend) and cell-based meat production.

Trend No. 9: Food companies will build more optionality into their supply chains for sourcing ingredients. Food supply chains have been disrupted in the past year by severe weather events, such as droughts in the Western states and frost in Brazil. Food companies may broaden their supplier base to mitigate the impact of similar events in the future.

Trend No. 10: CPG companies will launch creative initiatives to enhance e-commerce sales. Lately, CPG companies have been making a bigger push into direct-to-consumer channels. I expect to see more CPG companies launch subscription boxes across a range of brands, perhaps bundling disparate products that have a common corporate owner, like Nestle. In addition, consumer products companies are becoming more efficient in working with grocers’ e-commerce platforms to target specific customers. For instance, consumers who regularly buy Purina pet food online from Walmart should expect to receive coupons and promotions for competing pet food brands.

To sign up for The Stockout, a free newsletter focused on CPG supply chains, please click here.