As you read this market view, the planning for year 2020 railroad capital work is well underway.

It is that time of the year when staff members in different major departments within each Class 1 railroad company lay out their expectations for next year’s budgets.

The strategic question might be, “What’s the outlook in a period of traffic uncertainty?”

My hypothesis suggests lower capital expenditures (cap ex) for 2020 than in 2019.

Unlike truckers, railroad managers face multi-faceted budget hurdles. Rail executives have a complex infrastructure to both maintain as well as improve.

As previously discussed, railways are vast real estate organizations. They don’t pay into a trust fund to keep their “ways” in shape as with highways.

Regional engineers have calculated their “wish list” of projects based upon this year’s out-in-the-field operating experience.

Those localized track, structure, signals and bridge “needs estimates” will then be sorted at headquarters against other system-wide data.

The data sets include evaluations of ultrasonic inspection tapes of steel rails as well as assessments of geometry and surface defects that at some point require engineered correction.

All these hard data engineering assessments must be prioritized against the other overall business needs that marketing staff as well as locomotive and freight car mechanical departments are compiling.

Into October and November there will be a vetting of these competing cap ex needs lists.

Not every project is going to be funded.

Most capital projects require a calculated cost/benefit calculation that allows these senior officers to rank projects by expected rate of return. Those return on investment estimates are reviewed by the finance department according to approved templates.

Three right-of-way sectors require constant maintenance – plus periodic heavy-duty maintenance. They are:

- Track structure

- Bridges, culverts and tunnels

- Signal and communications systems

Beyond that are movable assets like locomotives and freight cars.

And there are general and administrative capital assets such as computers.

When most people think about the railroad track structure, they probably think first of the railroad tracks. In doing so, they might overlook the actual physical design of the railway routes that dissipates vertical forces from train passages down through the different layers of the structure. That vertical track structure is illustrated in the following graphic.

This route structure part of the railroad capital assets (along with tunnels) has the longest economic life measured often in 50- to 100-plus years. But this structure also requires a good deal of steady state maintenance to do such things as keep ballast clean and the geometry level. That kind of continuing maintenance consumes most of a railroad company’s capital dollars each year.

Table 1 identifies the broad categories over which capital dollars are spent each year on a major Class 1 railroad that likely spends between $3 and $4 billion as its announced capital budget.

A review of multiple railroads’ investor reports and SEC filings shows that the typical allocation of capital expenditure program by type of project includes:

- Track/roadbed – 48%

- Locomotives – 22%

- Capacity added – 6%

- Signals/communications – 6%

- Freight cars – 4%

- Safety – 2%

Remember that these percentages represent long-term patterns. In any given year or series of years, a category can have a significantly higher or lower percentage share of the budget. Track and roadbed share might drop to 38 percent or lower in some years.

Capital investment in Positive Train Control (PTC), for example, has been taking a rather large share of all major railroad capital dollars over the past half-decade or more.

During the early phases of a railroad adopting so-called Precision Scheduled Railroading (PSR) as a business model, some of these categories will see both a lower annual dollar allocation as well as a percentage of the cap ex annual budget pie. As one possible example, the financial targets under the roll-out of PSR heavily emphasize a reduction in locomotives and excess freight cars. That is the pattern revealed when we examine the changing railroad investment presentation slides.

In previous decades, when a railroad’s returns on capital assets was often in the 4 to 7 % range, many railroads tried to limit their annual capital expenditure to a target maximum. One target range would be that capital expenditures would not exceed 75% to 80% of operating income.

During the high annual traffic growth years between 2002 and 2006, and again in 2010 to 2013 – the cap ex of most of the Class 1 railroads like BNSF and Norfolk Southern often was elevated and could represent about 20% to 25% of freight revenues.

However, many of the railroad companies will see their total capital expenditures budget drop to a 14% to 18% share of freight revenues.

One notable exception is at Canadian National, where exceptionally high traffic growth across the provinces of Alberta and British Columbia has resulted in CN having to invest significant capital to add trains per day and track capacity. That’s regarded as a positive investment shift.

That change results in the 2018-19 capital expenditure budget at Canadian National increasing up to the higher 20%-plus share of freight revenues.

That’s the background.

After prioritization, the capital budget moves to the Board of Directors for discussion and a final decision. This typically occurs during late November or early December.

Board approval then starts the process of bids and procurement. That allows materials to be ordered, then received. All of this takes time.

Railroads’ cap ex projects are normally released to the industry press in January.

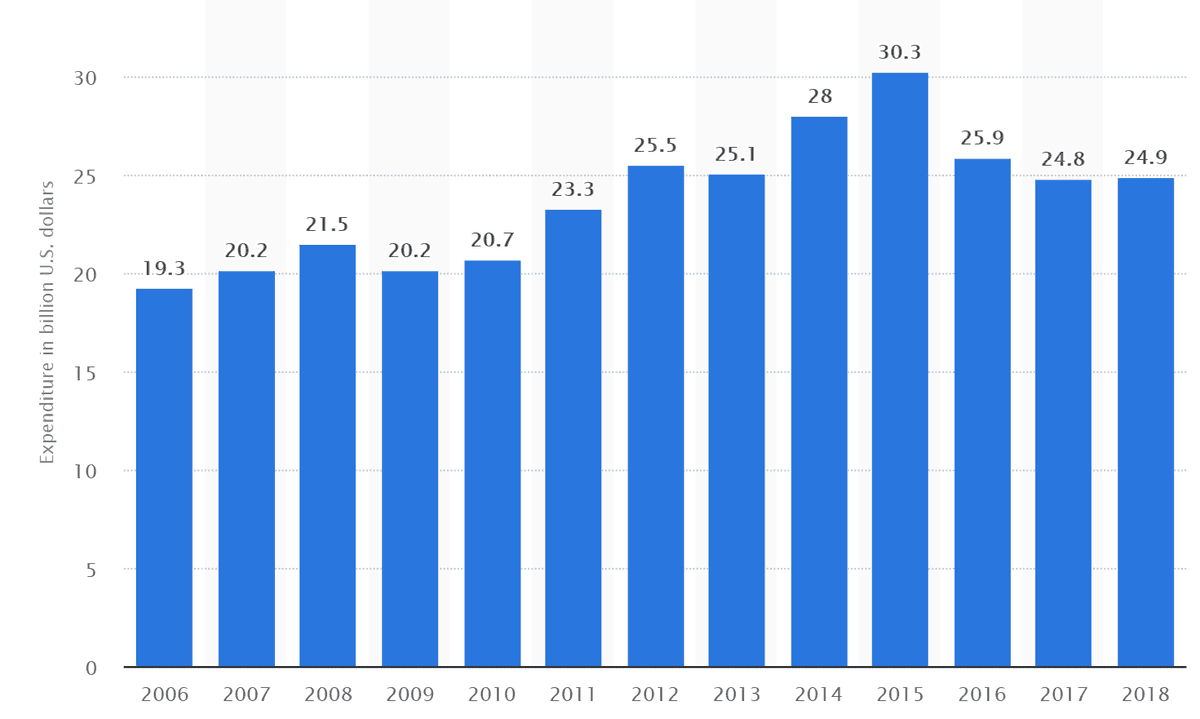

Figure 2 illustrates the recent pattern of U.S. railroad capital spending.

Source: A blend of AAR data and a Statista 2019 report

What is the outlook for 2020?

That’s tricky to estimate given uncertainty of the U.S. economy and trade headwinds.

Here is my estimated outlook based upon the current market view.

The capital expenditures for PTC projects over the past decade was estimated by various industry sources at a $12 billion initial design and install expense. Most of the ongoing component system is now in place. Therefore, incremental dispatching and communications PTC expenses are likely to fall during 2020.

Exceptions might occur if certain PTC parts fail to perform as expected.

There is very little all new railroad freight line construction underway in the U.S.

There are no large carload railroad yard projects being built, for Union Pacific’s delayed Brazos classification yard in Texas.

A logical outlook into year 2020 suggests that fewer than 500 locomotives will be ordered. In contrast, in a good year about 900 new locomotives would be ordered.

New railroad freight car orders will drop to around 40,000 – which is about a calculated steady state fleet size replacement rate. In contrast, a good year might see 60,000 to 70,000 units ordered.

A year ago, the railroad boards of directors collectively approved healthy 2019 capital expenditures’ budgets. At the time, that expressed optimism about the year 2019 business volume for non-coal carload traffic and both domestic intermodal and international intermodal traffic growth.

That business unit volume growth hasn’t occurred. The signals are that the 2019 traffic volumes have turned out as much as 6% to near 10% lower than expected for the year.

Railroad board members often tend to be conservative, especially as they consider the flawed traffic volume outlook for 2019 that is still fresh in their minds.

The result? It is possible that the U.S. railways’ may lower their 2020 capital budgets by as much as 4 to 6% below the amount authorized for 2019.

What is your outlook?

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now