Newly released fiscal-year (FY) statistics from the Panama Canal Authority (ACP) and the latest shipping price data from Freightos both shine a positive light on U.S. East Coast box imports. To the extent cargo flows favor the Atlantic over the Pacific ports, it’s good for trucking demand and bad for intermodal rail demand.

The ACP’s fiscal year runs from Oct. 1-Sept. 30. FY19, which just concluded, was impacted by low water levels due to a regional drought, as well as global trade tensions. Total cargo came in at 252.4 million long tons (1 long ton equals 2,240 pounds), down 1% versus FY18.

Volumes of liquefied natural gas (LNG) and liquefied petroleum gas rose, as did roll-on/roll-off cargo, but drops were logged for containers, dry bulk, tankers and general cargo. Container cargo volumes totaled 56.37 million long tons, down 1.4% from FY18.

Asked by FreightWaves about the apparent softness of the FY19 numbers, ACP responded that long tons “are not necessarily an indicator of the Panama Canal’s performance” because they measure weight and FY19 long tons were lowered by “a fall in iron and steel manufactures, as well as in minerals and heavy products, which have been largely replaced by the increase in LNG, a product that does not weigh much.”

The ACP instead emphasized its own internal measure, PC/UMS tonnage, which gauges cargo capacity, and which hit a record 469 million in FY19, up 6.1% from FY18. The ACP now predicts the waterway will reach 493.4 million PC/UMS in FY20 (driven by LNG), up 5.2% from FY19.

Breaking down the container stats further, box long tons going from the Pacific to Atlantic (largely Asia to U.S. East Coast) rose 1% and flows from the Atlantic to Pacific fell 5%. In other words, the Asian cargo to East Coast ports is still increasing; it’s U.S. imports to Asia – most likely to China – that are paring the results measured in long-tons (whether due to lower volume or weight).

One of America’s biggest exports is waste paper. According to the ACP’s commodity-level data, paper and paper product cargoes transiting the canal from the Atlantic to the Pacific fell to 95,000 long tons in FY19, down 63% from FY18.

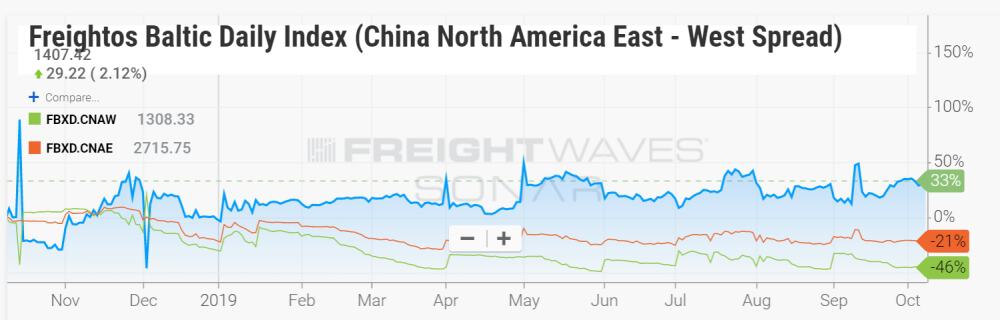

Meanwhile, the latest index data from Freightos – which tracks the cost to ship a 40-foot-equivalent unit (FEU) container along various trade routes – offers more positive perspective on U.S. East Coast imports.

In general, box-rate performance in the second half of this year has been terrible, which bodes ill for container lines such as Maersk, MSC and CMA CGM. When there is not a significant driver (positive or negative) in terms of deployed vessel capacity, rate levels can be seen as a reasonable proxy for demand.

The Freightos Baltic Daily Index covering the trans-Pacific route from China to the North American West Coast (SONAR: FBXD.CNAW) is currently at $1,308 per FEU, the lowest it has been since late August and down 46% year-on-year. U.S. imports at this time last year were unusually elevated because U.S. buyers were front-loading cargoes from China to beat tariff deadlines.

The current cost to ship boxes from China to the East Coast (SONAR: FBXD.CNAW) is $2,715 per FEU, down 21% year-on-year.

It should cost more to ship to the East Coast, because the voyage distance from Asia is considerably longer and Panama Canal tolls are not cheap. But the spread between the two rates – the “Panama spread” (SONAR: FBXD.PANA) – varies. To the extent it widens, it can be viewed as a positive reflection on demand into U.S. East Coast ports.

That spread has indeed performed well, because the pricing to the East Coast is doing less poorly than to the West Coast. The spread is now at $1,407 per FEU – up 33% year-on-year. More FreightWaves/American Shipper articles by Greg Miller

Editor’s note: Freightos has a business agreement with FreightWaves that includes editorial coverage.

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now