The 2011 movie Moneyball tells the story of Billy Beane, a former baseball player who became the general manager of the Oakland A’s. Beane worked with Harvard-educated statistician Paul DePodesta to develop a method to judge a player’s value in a baseball lineup by using statistics and models called sabermetrics to make incremental improvements that increase the team’s odds of winning. Beane and DePodesta met resistance when they challenged long-standing methods to evaluate baseball players. But great news, their method worked!

With tons of data emerging in transportation and freight resulting from new technology, there is a renaissance on how to navigate the freight market in an up or down cycle and there are lessons to be learned from Billy Beane and his sabermetrics.

FreightWaves’ SONAR was created from the idea that the highly fragmented trucking industry could benefit from additional data that provided more transparency into what was occurring in the general market. Those involved in the freight market have access to multiple internal data points to judge how well they are performing. The problem with this approach is whether you are a carrier, broker or shipper, you have a large bias towards your specific activity. This leaves each with multiple blind spots.

Moneyball explained

All data has biases. The more specialized the information, the more biased it becomes. For instance, in baseball, the batting average was used as a primary way of measuring a player’s value on offense. In Moneyball the idea that a player’s ability to get on base was actually more valuable to scoring runs, so a higher value was placed on the On Base Percentage (OBP) statistic than batting average in the Beane/DePodesta model. OBP measures the rate at which a player gets on base safely per total plate appearances, walks, hits, and reaching base due to errors.

Batting average was too focused on measuring a player’s ability to hit the ball, which does not always translate to scoring runs. Players with higher OBP tend to be faster and more patient at the plate. The player with a higher batting average may be more focused on hitting the ball to increase average but striking out more often instead of taking a walk. When players are more focused on getting on base, the odds of them scoring increases according to the studies they performed in statistical models. This process also allowed teams to identify players with more value, as the higher priced players had the higher batting averages, not OBPs.

This is an article about freight, though. So now that you have the basic concept of Moneyball, let’s dive into how this concept applies to maneuvering the volatile freight market. The statistical modeling that was used in baseball was not overly complicated. A lot of the data was readily available. The freight market does not have near the amount of aggregated statistics available that baseball has, but there are several internal metrics as well as SONAR data points that can help carriers operate more efficiently.

Revenue: the batting average of freight

The base principle of using statistical modeling to improve effectiveness is to find the measurement(s) that matter most to improve performance or in the case of an asset-based carrier improve return or profit margins. The profit margin calculation is very simple – revenue less expenses.

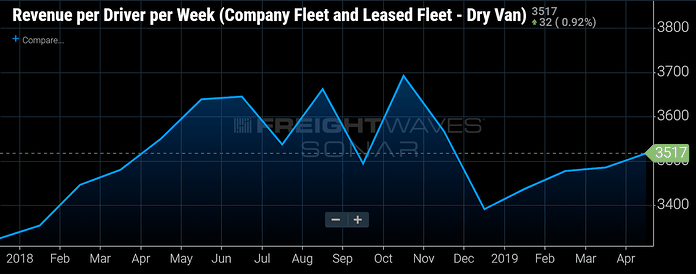

SONAR chart of TCA dry van carriers’ average revenue per driver per week each month

Most carriers measure average revenue per truck per week so they can easily calculate profit, since most have a running idea of how much it costs to operate a truck. This is a good start, but it is a sales-focused number. There is not always a load available, and in a soft market like the one we are seeing currently it does not provide an operational target. In other words, this is largely a sales-focused metric, not an operational metric. This number is useful in measuring how profitable a carrier is but lacks operational direction.

Many carriers choose to shut down during periods of oversupply in the market. Instead of taking a low-paying load, they will just not work. This is a flawed logic; as many larger carriers know, they need to keep utilization as high as possible. Utilization in trucking means trucks are being used in a revenue-producing manner regardless of profit or loss. To understand why this is important, a basic understanding of fixed versus variable costs is needed.

Fixed costs are there regardless of driving

Fixed costs are the costs a company assumes regardless of activity. The fixed cost of a truck is easy to calculate—simply the cost of owning or leasing the truck divided over a period of time. If leasing the truck, it is the cost of the monthly lease payment. If the truck is purchased, then it is the monthly payment or depreciation. Carriers do not stop paying on a truck if it does not move. Larger carriers with back office staff and brick-and-mortar facilities also have these items to consider.

The variable cost is a little more complicated but still relatively straight-forward. Variable costs include maintenance, driver pay, fuel, tires, truck wash, licensing and insurance. There are multiple ways of allocating these costs across the fleet, but it is much simpler when there are fewer trucks because it is easier to calculate the specific cost for each unit.

SONAR chart of average monthly maintenance expense per mile for TCA reefer carriers

Variable costs only occur when the truck is moving, fixed costs occur regardless of truck operation. So, when carriers decide to not drive, they are still losing money. Of course, they do not want to drive for next to nothing, but most of the time the market price will cover all the fixed costs and most of the variable costs leading to less of a loss than they would incur by idling the truck.

Sometimes getting more revenue is not an option, so making sure the operation is as efficient as possible will lead to better chances for profitability or at least allows the carrier to lose less and survive long enough to make it through the down cycle. In the less-than-truckload sector, this concept is known as contribution.

Elevated revenue is the easiest and most understood target for carriers to set as a goal, but the reality is the trucking industry is extremely competitive and cyclical and down cycles when revenues are suppressed are a given. Being able to increase the odds of utilization will lead to more success. In other words, revenue is the batting average of freight.

How can carriers increase the odds of utilization?

As mentioned, the freight market is very competitive and cyclical. To increase the odds of finding freight, carriers need to know where the freight demand exceeds the supply of trucks. SONAR users have two main indices at their disposal to alert them to markets where they will have better chances of finding available freight – the Outbound Tender Rejection Index (OTRI) and Headhaul Index (HAUL).

SONAR heat map of Headhaul Index values – blue indicates a positive valued “headhaul” market and red indicates a negative valued “backhaul” market

OTRI is a near-time measurement that shows where carriers are likely to honor their contracted freight load requests. When they are rejecting more of their contracted loads—OTRI increases— that means there will be better chances of other carriers seeing that load, either by request or on a load board. When tender rejections decline there are fewer opportunities for carriers available. Positioning trucks where markets have increasing or elevated outbound tender rejection rates in relation to the rest of the country will give a carrier better odds for finding additional loads, potentially with elevated margins.

HAUL is the difference of outbound load volumes and inbound load volumes. It is the Outbound Tender Volume Index (OTVI) less the Inbound Tender Volume Index (ITVI) for any individual market. As many carriers know, heavy consumption markets like Miami and Phoenix are difficult to find loads out of, which is why they attempt to charge more to haul freight into these markets. These “backhaul” markets can become less so at different times of the year, meaning carriers can attempt to accept more freight into these areas during more favorable times.

A better use of HAUL is to find when markets that do not have a clear identity shift between headhaul (more out than in) and backhaul conditions. The nation’s second-largest market, Atlanta, shifts between these two regularly. Carriers may be able to utilize their equipment better in other lanes by accepting freight into a market with increasing OTRI or positive HAUL values.

Most carriers have consistent shipper accounts that keep them moving in regular lanes. This keeps them biased to their shippers without real visibility to the rest of the market. The aforementioned indices and the Outbound Tender Market Share (OTMS) index can help carriers identify markets and lanes that are more favorable to bid on by giving them an idea of where freight volumes are in general. OTMS measures how large a market is in relation to the rest of the 135 U.S. markets. They all add up to 100 percent. Ontario, California and Atlanta tend to occupy the top two spots, moving between 4 percent and 5 percent of the total.

SONAR Ticker: OTMS.ATL, OTMS.ONT

Combining this data with the carrier’s existing data will allow it to increase the odds for making the best margin possible for the given market conditions. Revenue covers up a lot of sins, but the best operators with the highest utilization survive the longest in this highly fragmented and competitive industry. Knowing where to look is as important as knowing what to do. Chasing rates is not a sustainable practice.

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now