According to “IMO 2020: A new higher normal for diesel prices?,” a new report from the FreightWaves Freight Intel Group, when IMO 2020 goes into effect on January 1, 2020 the domestic U.S. logistics industry, including the shippers it serves, will be grossly unprepared for volatility in the diesel markets.

This report, which builds on extensive IMO 2020 reporting by FreightWaves over the past several months, surveys the U.S. logistics industry and shippers to get a sense of their awareness of IMO 2020. This includes how the new rules mandating the use of very low sulfur fuel oil (VLSFO) will increase competition for diesel fuels.

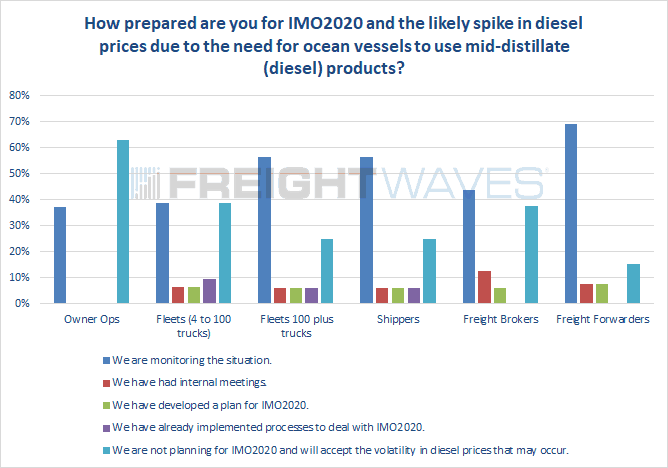

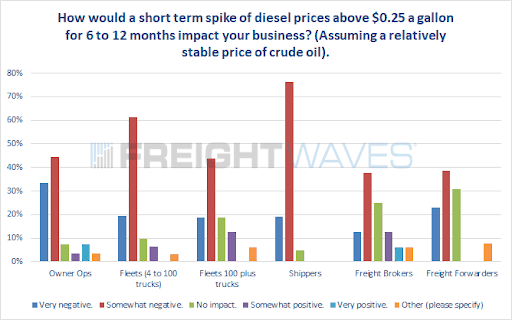

A key finding is that owner-operators (one to three trucks) and small fleets (four to 100 trucks) – the groups most at-risk to higher diesel prices – have decided to not prepare at all. Three of five owner-operators (60 percent) and two of five small fleets (40 percent) indicated they will not develop any plans or strategies for possible increases in diesel prices in the coming months.

The survey also found that domestic trucking and transportation professionals were five times more likely to be merely ‘monitoring the situation’ rather than planning or taking action.

The logistics sector plans (or lack thereof) for IMO 2020

U.S. shippers are also behind in plans for how to handle rising fuel surcharges from carriers. Of shipper respondents, 70 percent assume the first course of action will be to try passing any diesel price increases along to customers. This will likely wind up hitting the wallets of end consumers, much like tariffs.

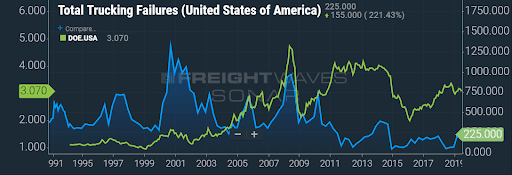

Any sustained spikes in diesel prices are highly dangerous to trucking companies. Based on analysis by FreightWaves and Michigan State University using two decades of historical trucking company failure rates, most non-recession trucking company failures occur when diesel prices are rising and spot rates are depressed. These two conditions are becoming more and more likely for 2020.

Trucking company failure rates and diesel price correlation

Note: Trucking company failures include fleets with five or more trucks.

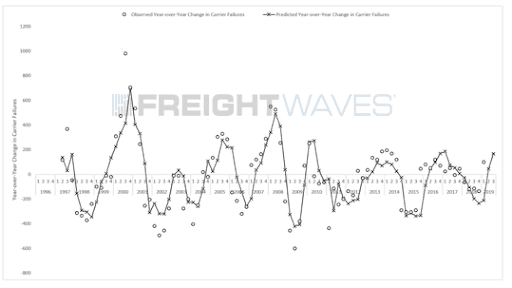

Forecast of trucking failures in 2019

The FreightWaves Intel Group also analyzed other industries at risk of higher diesel or jet fuel prices. This includes airlines, cruise lines, railroads and refineries. All spend a significant percentage of revenues on fuel. Railroads have historically had the most pricing power of these industries, and this trend should hold. Airlines most likely will fare the worst passing on costs to customers as there are plenty of alternatives to flying.

Refineries should be the clear winners of IMO 2020. The increased competition for diesel distalites will likely widen the crack spread (the difference between the cost to buy oil and the revenue of selling refined products), which will increase refineries profit margins.

Ship owners will feel the pain of IMO 2020 the most. The bad news is VLSFO is a new and untested blend of fuel that currently has no market price. There is an established and traded low sulfur bunker fuel on the market – it is a class of fuel also made from diesel distillates called Marine Gasoil (MGO). The bad news is MGO trades at roughly a 60 percent premium to high sulfur fuel oil (HSFO), which most ships currently use for fuel.

In the end, IMO 2020 could be the next electronic logging device (ELD) scare in the logistics market. It may be an event with drama leading up to it, short-term chaos, followed by a steady return to a new manageable status quo. Or, it could create not only a short-term spike in diesel prices, but a new long-term higher normal that will be painful for carriers, shippers and ultimately consumers to absorb.

Key highlights of how IMO 2020 will affect the U.S. trucking and logistics sectors

Imagine if one million for-hire interstate trucks suddenly converted from diesel to gasoline on January 1, 2020. It would be pure chaos as trucks competed with cars for gasoline. This is what IMO 2020 will do to the diesel market as ocean vessels switch from HSFO made from a category of oil product known by a variety of names – fuel oil, marine fuels, bunkers fuels. They will switch to either MGO, which is an existing diesel product designed for marine applications, or VLSFO, a new product made for IMO 2020 that is produced in part by blending feedstocks that now make over-the-road diesel.

There are other ways to meet the rules – ships can install scrubbers that allow the burning of HSFO, but it’s expensive, especially for a smaller fleet. Liquified natural gas can be used, but that’s a major retrofit. Or the rules can just be ignored, but estimates of non-compliance have been dropping.

The bottom line – there’s likely to be another 1.5 to 2 million barrels per day (b/d) of diesel demand as a result of the rule. In a tightly balanced market, that is a significant number.

Although the implementation date for IMO 2020 is January 1, 2020, the reality is that it could begin impacting markets by September. That’s because ships are expected to begin cleaning out their tanks that contain non-compliant HSFO and filling them with compliant fuels.

So far, there are few signs of any of the market beginning to react to the impending switch. The futures market for ultra low sulfur diesel (ULSD) has not reacted yet though futures markets, despite their name, are a notably poor predictor of prices in the future; they are designed to hedge future supply or demand. The forward curve in a futures market is a complex brew of the current price, interest rates and inventories; it doesn’t predict the future.

Separately, the prices for the new VLSFO blends that are being created are trading at a premium to HSFO but certainly not at any sort of level that would spur fear in the hearts of diesel buyers. The question is when it happens, and if it happens, what will be the first signs? Besides the VLSFO-HSFO spread, other signals may be the price of physical diesel compared to the ULSD price on the CME and also the price of diesel to the Brent crude oil benchmark.

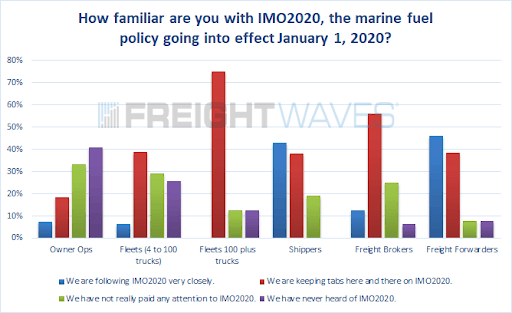

Shippers and the U.S. trucking and logistics sector are not ready for IMO 2020. According to the FreightWaves IMO 2020 survey, 40 percent of the logistics sector and shippers have either never heard of IMO 2020 or have not paid it any attention. When asked about their plan of action, eight of 10 are either monitoring the situation (doing nothing) or have decided to skip the planning and ride out the volatility.

Owner-operators (one to three trucks) and small fleets (four to 100 trucks) are most at risk and are doing the least to prepare for a rise in diesel prices. Sixty-three percent of owner-operators and 39 percent of small fleets indicate they are not going to prepare for the effects of IMO 2020 on diesel prices.

Based on historical data there will be a wave of trucking failures if diesel prices spike. Fleet failures are highly correlated to rising diesel prices and falling spot rates. If diesel increases by 10 percent over one quarter with stagnant spot rates, trucking company failures will increase significantly.

With new competition for diesel fuel, the battle for those barrels could become intense. Refiners have added some new capabilities to produce those fuels. But ultimately, the market will respond to economics. Markets are resilient and that may be the ultimate savior. For example, if the price of MGO and VLSFO soars relative to the price of HSFO, the economics of installing a scrubber start to look more attractive. Every scrubber decreases MGO or VLSFO demand. Ships may turn to slow steaming; that softens demand. To take advantage of profitable refining opportunities created by IMO 2020, refiners may push larger-than-usual quantities of crude oil through their plants. That may mean too much supply of other products like gasoline, but it may ease any squeeze on diesel.

The key thing to remember is markets always find a way. But they don’t always find a way immediately. The transition could take months to as much as a year.

There’s another possibility – a global slowdown or recession should stop diesel prices from moving higher in late 2019 or early 2020. With trade wars, real wars, Brexit and Italian debt creating headlines, the global economy could falter by the time IMO 2020 goes into effect. There is precedent for that. In 2008, when the price of crude oil hit its all-time high of more than $140/barrel, diesel actually rose more in terms of percentage. It had just undergone a change in specification in 2006-2007 when allowable sulfur content was reduced in the U.S. and Europe. But when markets began to fall because of the Great Recession, oil plunged and diesel did as well.

IMO 2020 will ultimately be a tax on consumers. Seventy-seven percent of the logistics sector and shippers expect each will try to pass along fuel surcharge hikes to their customers. This will act like any tax or tariff – it will eventually hit the end-consumer and most likely put a dent into final demand of goods.

FreightWaves will continue to monitor and report the actions that the logistics sector, trucking companies, shippers and ship owners take to prepare for IMO 2020.

Freight Intel research is live in FreightWaves SONAR under the light bulb icon at the top of the dashboard alongside all of the Daily Watch and Deep Dive notes from FreightWaves’ Market Experts.

For more information on the FreightWaves Freight Intel Group, please contact Kevin Hill at khill@www.freightwaves.com or Seth Holm at sholm@www.freightwaves.com.

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now