This Week’s DHL Supply Chain/FreightWaves Pricing Power Index: 25 (Shippers)

Last Week’s DHL Supply Chain/FreightWaves Pricing Power Index: 30 (Shippers)

Three-Month DHL Supply Chain/FreightWaves Pricing Power Index Outlook: 50 (Balanced)

The trucking industry operates in a market based on real-time demand and supply. When demand is higher than capacity, carriers gain negotiating power for rates. When supply is higher than demand, shippers gain negotiating power for rates.

The DHL Supply Chain/FreightWaves Pricing Power Index uses the analytics and data contained in FreightWaves SONAR to analyze the market and estimate the negotiating power for rates between shippers and carriers.

The Pricing Power Index is based on the following indicators:

Load Volumes: Momentum and Trend Neutral.

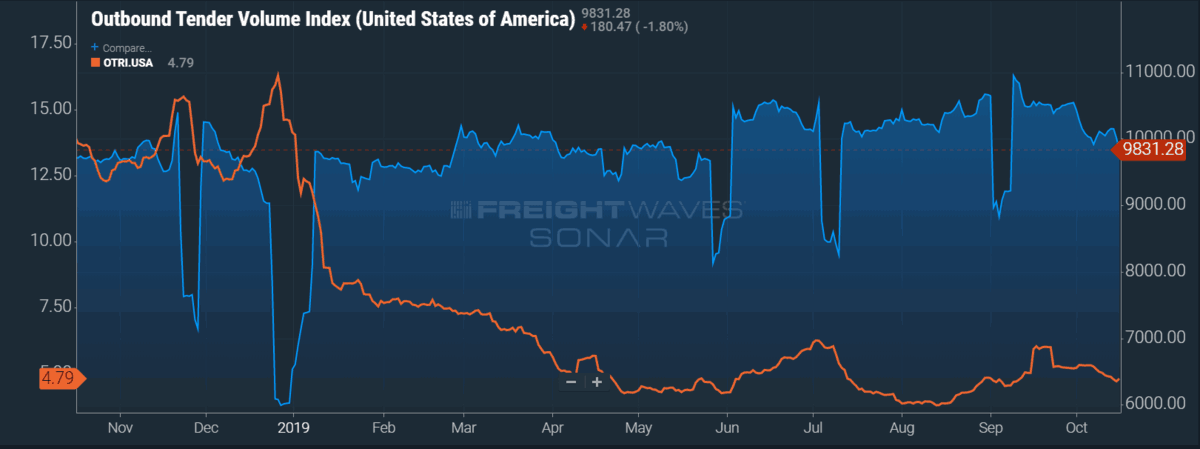

The Outbound Tender Volume Index (OTVI.USA) is currently at 9,831.38. While load volumes have remained above 2018 levels since mid-July, over the past week the year-over-year change has weakened significantly from 7% to 1.22%. Week-over-week load volumes are down 2.78%. While it is too early to call a trend, deteriorating economic indicators combined with weakness in OTVI.USA is worrisome.

SONAR: OTVI.USA

Tender Rejections: Trend and Absolute Levels Positive for Shippers, Long-Term Trend Positive for Carriers.

Outbound Tender Rejections (OTRI.USA) declined 23 basis points (bps) this week from 5.02% to 4.79%. Capacity continues to be loose without any clear indicators to build a narrative for capacity to tighten or line-haul rates to bounce.

The end of the United Auto Workers (UAW) strike could bring a short-term bounce in OTRI to certain markets affected by the strike (more on the UAW strike below). If the tentative deal is ratified by its members, then markets like Detroit where OTVI.DTW is down 37%, and OTRI.DTW struggles to remain above 3%, should pop for a few weeks before returning to normal levels.

SONAR: OTRI.USA

Spot Rates: Absolute Level and Momentum Positive for Shippers

Spot rates continue to slide as we head into October. The DAT dry van national average slid 156 bps this week to $1.40 per mile. We still think this range is the trough for spot market rates as it is reflective of normal per mile operating costs for carriers. With this said, it can still remain at this lower band for the coming months based on capacity metrics from OTRI.USA and weakening demand indicators from the economy.

Clawing Back “Paper” Rates: Momentum and Trend Positive for Shippers

One carrier called out a very competitive and aggressive environment on its earnings call in terms of an early read on the upcoming bid season for contract freight. We believe this will be a common theme moving forward, suggesting shippers will be aggressively clawing back 2018 increases in paper rates during this bid season. It also calls into question some of the more aggressive estimates we have seen looking for low-single-digit positive paper rates for the overall truckload industry in 2020.

September ACT Class 8 Truck Data: Absolute level and momentum positive for Carriers

ACT released its September Class 8 truck metrics this week. On balance, these supply-side indicators are bullish for the medium- to long-term outlook for carriers.

For example, Class 8 Orders fell 70% year-over-year to 12,700 units (compared to our estimate of replacement demand of approximately 23,000). Orders have been sharply negative on a year-over-year basis going all the way back to November 2018.

The industry produced 28,000 trucks in September, which was down 3% year-over-year and negative for the first time since April 2017. Additionally, inventories are on the downswing, with the Class 8 inventory-to-sales ratio falling to 2.5 times in September from 3.1 times in August.

It will take time (likely measured in quarters) for capacity to right-size, but the ACT data continues to be directionally encouraging for carriers.

Critical Events: Positive Short-Term Momentum for Carriers.

UAW Auto Strike

A tentative deal was reached this week between General Motors (GM) and 48,000 UAW members to end the 32 days and counting strike. The terms of the settlement still need to be voted on by leadership before a full vote can be rolled out for a ratification vote by all members. This could take up to two more weeks if all goes smoothly, though workers could return to work before the ratification vote if the initial vote is in favor of the deal.

According to Bloomberg, the UAW strike is costing GM $100 million per day in lost profit as production facilities remain idle. If and when a deal is ratified and workers return to the assembly lines, this backlog in inbound and outbound freight will likely be a boost for volumes in the Midwest along with GM vendors located around the country as raw materials and finished parts are expedited to restart production.

East Coast Nor’easter

High winds late this week due to a Nor’easter on the East Coast from Delaware to Maine will likely disrupt freight markets over the second half of this week. While this storm should not have any lasting effects on the freight markets in the Northeast, it will likely increase spot rates over the next few days.

Economic Stats: Positive Momentum for Shippers.

Last week we noted that one point of emphasis that is key for the freight markets moving forward is that the U.S. consumer needs to stay strong in order for this economic cycle and the nascent freight market recovery to continue. While we still believe this to be the case, there are several signs emerging that the strength may be weakening – at least on the margin – which is a potential headwind for outbound tender volumes in 2020.

Retail sales for September disappointed this week, fueling the fire that contagion in manufacturing weakness may be starting to spread. The numbers were not bad in an absolute sense – at 4.1% percent year-over-year growth. However, similar to most of the indicators we watch, the trend is deteriorating. On a month-over-month basis, retail sales fell 0.3%, the first decline in seven months going back to February 2019. Further, the 4.1% year-over-year growth rate was down from 4.4% last month and is well off the cycle peak of 6.5% back in July 2018.

Lastly, we got more of the same in terms of industrial and manufacturing malaise this week. Overall U.S. industrial production fell 0.4% in September according to the Federal Reserve’s data, the second decline in the last three months. It appears the recessionary backdrop for this segment of the economy continues to weaken.

Third Quarter Transportation Earnings Highlights: Absolute levels positive for Shippers, momentum positive for Carriers

The market is sanguine on the transportation sector, even in the face of disappointing earnings as demonstrated by the fact that our proprietary FreightWaves Truckload Index was up 8% this week.

Both Knight-Swift (KNX) and J.B. Hunt (JBHT) missed Wall Street consensus estimates for earnings and issued tepid outlooks. However, their stocks rose 8.2% and 9.2% this week, respectively, suggesting a willingness among market participants to look through any near-term weakness due to the potential for earnings to trough in 2020.

For more information on the FreightWaves Freight Intel Group, please contact Kevin Hill at khill@www.freightwaves.com, Seth Holm at sholm@www.freightwaves.com, or Andrew Cox at acox@www.freightwaves.com.

Supply Chain AI Symposium

Past the hype. Join operators, founders, and enterprise leaders figuring out how to deploy AI in supply chain.

Future of Rail Symposium

Reshoring is rewriting freight demand. Join shippers, rail executives, and government officials to shape the next decade.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

Past the hype. Join operators, founders, and enterprise leaders figuring out how to deploy AI in supply chain.

The Old Post • Chicago, IL Register NowReshoring is rewriting freight demand. Join shippers, rail executives, and government officials to shape the next decade.

The Signal at Chattanooga Choo Choo • Chattanooga TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now